The 1099 form is the family of IRS information returns a US payer files at year-end to report payments made to people who were not employees, the most common of which is the 1099-NEC for nonemployee compensation of $600 or more to a contractor, freelancer, or vendor. The 1099 family is not one form. It is a stack of related variants (NEC, MISC, K, DIV, INT, R, and a long tail of others) that each report a specific type of payment, and the federal calendar gives the payer until January 31 to issue every one of them to the recipient and to the IRS. The 1099 is the payer-side output that pairs with the W-9 intake the contractor signs at the start of the relationship: W-9 in, 1099 out, with the year of payments and the backup-withholding accounting in between.

This guide is the payer-side walkthrough of Form 1099 for a US small business in 2026: the family map (NEC vs MISC vs K vs DIV vs INT vs R and where each one fits), the $600 threshold and the corporate-entity exemption with the legal-services exception, the line-by-line for the most common variant (1099-NEC), the January 31 dual-deadline rule, the 10-return e-filing threshold the IRS lowered in 2023, the three-prong IRS test that decides whether the worker is a 1099 contractor or a W-2 employee, Form 1096 for the shrinking population of paper filers, the 35-state copy mandate with the CFSF program, and the two-step corrections process. The audience is the same small finance and HR teams the rest of the federal-form pillar is written for: the office manager running payroll and AP from one browser tab, the founder who just sent the first $4,500 invoice payment to an outside designer and is wondering whether the company owes the IRS something, the operations lead in mid-January who has thirty contractors and no idea where to start. If you want a January-prep workflow that captures the payer block, the recipient block from the W-9, Box 1 compensation totals, and the backup-withholding amount in one structured intake, clone the Good Form 1099-NEC payer prep template.

The short version:

- The 1099 is a family of IRS information returns. The 1099-NEC reports nonemployee compensation of $600 or more to a contractor. The 1099-MISC reports rent, royalties, prizes, and legal fees. The 1099-K, DIV, INT, and R cover payment-card, dividend, interest, and retirement income respectively.

- The $600 threshold for 1099-NEC is aggregate across the calendar year, not per invoice. One $250 invoice and one $400 invoice to the same contractor trigger the 1099. So does any single payment of $600 or more.

- C and S corporations are exempt from 1099 reporting on most service payments. Exceptions: legal services (always reportable on 1099-NEC, even to corporate law firms), medical and health-care services, fish purchases, and a short list of other categories.

- The 2026 deadline calendar: 1099-NEC to recipient and to the IRS by January 31. 1099-MISC to recipient by January 31, to the IRS by February 28 paper or March 31 electronic. Form 8809 extends the IRS deadline by 30 days, never the recipient deadline.

- The IRS lowered the e-filing threshold from 250 to 10 aggregate information returns starting tax year 2023 (filed January 2024+). The 10 includes every 1099, W-2, 1095, and 1098 the payer files in the same year. Almost every US business is now required to e-file.

- The 1099 vs W-2 decision turns on three IRS categories: behavioural control (who decides how the work is done), financial control (who carries the financial risk), and the relationship of the parties (ongoing employment vs project-based engagement). If a prong is mixed, default to W-2.

- Misclassification penalties under Section 3509 fall on the payer, not the worker. The Section 530 safe-harbor is narrow and requires a documented reasonable basis, consistent treatment, and full information-return filing for all years.

- Backup withholding shows in Box 4 of the 1099-NEC and triggers a Form 945 obligation for the payer. The withholding rate is 24% of the gross payment.

- Corrections to a filed 1099 use the two-step VOID + corrected process for Type 2 errors (wrong payee, wrong TIN, wrong form type) and a single corrected return for Type 1 errors (wrong amount, wrong code, wrong checkbox).

The 1099 Family Map: NEC, MISC, K, DIV, INT, R

The 1099 is one of the longest-running IRS information returns and the family map matters because picking the wrong variant is a Type 2 correction (the worst kind) and a recipient-confusion problem at year-end. The six variants that account for the bulk of 1099 filings for a small US business in 2026:

- 1099-NEC (Nonemployee Compensation). The contractor-payment form. Reports $600 or more in services paid to a non-employee during the calendar year. Reintroduced by the IRS for tax year 2020 after a 38-year retirement, specifically because the MISC's bundled use was breaking the deadline calendar (NEC payments needed a January 31 IRS deadline; MISC's other categories could wait until March 31). NEC is the variant a small business that pays contractors will file the most of.

- 1099-MISC (Miscellaneous Information). The catch-all for non-NEC payments: rent of $600 or more (Box 1), royalties of $10 or more (Box 2), prizes and awards (Box 3), gross proceeds paid to attorneys (Box 10), fishing-boat proceeds (Box 5), crop insurance proceeds, and a long tail of other categories. The MISC is the form a small business uses for landlord rent payments and for legal-fee gross proceeds where the payment is not for nonemployee services.

- 1099-K (Payment Card and Third-Party Network Transactions). Filed by payment-processing platforms (Stripe, PayPal, Etsy, Venmo for business accounts) when a recipient receives payments above the threshold. The threshold has been moving: $20,000 and 200 transactions historically, then $600 (delayed twice), with $5,000 set for tax year 2024 as the IRS phased in the lower threshold under ARPA. Most small businesses receive 1099-Ks rather than file them; the form is the third-party network's reporting obligation.

- 1099-DIV (Dividends and Distributions). Filed by corporations, mutual funds, and brokerages for $10 or more in dividends, plus capital-gain distributions and liquidating distributions. Small operating businesses rarely file 1099-DIVs; they receive them.

- 1099-INT (Interest Income). Filed by banks, brokerages, and other interest payers for $10 or more in interest. Same pattern as DIV: small operating businesses receive these rather than file them.

- 1099-R (Distributions from Pensions, Retirement Plans, etc.). Filed by retirement-plan administrators for distributions of $10 or more. Even a small business with a SEP-IRA or solo 401(k) at a custodian will not file 1099-Rs directly; the custodian files them.

The variant map above shows the six in their year-end relationship, with NEC drawn as the core for the typical small-business payer.

Who Gets a 1099-NEC: the $600 Threshold and the Corporate Exemption

The 1099-NEC threshold is $600 aggregate during the calendar year, paid to a single recipient, for services performed in the course of the payer's trade or business. The threshold includes the labour portion of any mixed-bill invoice (parts and labour combined are reportable if billed together) but does not include reimbursed expenses billed separately on the contractor's invoice. Personal payments do not count: a contractor hired to fix the office plumbing crosses the threshold; a contractor hired to fix the home owner's residential plumbing does not.

The corporate-entity exemption is the second filter. Most payments to C corporations and S corporations are not 1099-reportable, even if the payment crosses the threshold. The exceptions, where the corporate exemption does not apply:

- Legal services. Always reportable on 1099-NEC if the payment is for services, regardless of the law firm's corporate status. This is the single most-missed 1099 rule among small payers. The corporate exemption was specifically removed for attorney services because the IRS wanted full reporting on legal-fee income.

- Medical and health-care services. Reportable on 1099-NEC regardless of corporate status. Includes payments to a physician, hospital, or other health-care provider for the trade-or-business medical services.

- Fish purchases. Cash payments of $600 or more to a fisherman for fish or other aquatic life caught for resale, regardless of the payee's corporate status. The reporting goes on 1099-NEC Box 1.

- Substitute payments and broker fees. Specific securities-industry categories, reportable regardless of corporate status.

- Attorney gross proceeds. Different from legal-services payments. A payment of gross proceeds to an attorney (e.g., a settlement payment that the attorney holds in escrow for a client) goes in 1099-MISC Box 10, again regardless of the law firm's corporate status.

The W-9 the payer collected at the start of the relationship is what tells the payer whether the recipient is incorporated. Line 3a of the W-9 form carries the federal tax classification (Individual, C corp, S corp, Partnership, LLC, Trust); Line 3b adds the LLC sub-classification (C, S, or P) when applicable. The clean way to handle the exemption is to record the Line 3a result against every vendor on intake and let the AP system auto-flag the year-end 1099 batch with the corporate-exempt rows pre-filtered.

The $600 threshold does not exempt the payer from collecting the W-9. The W-9 should be collected from every non-employee recipient regardless of whether the relationship is expected to cross the threshold, because a one-off $250 invoice can become an $850 relationship two months later and the year-end 1099 is then easier to file from existing data than from a January W-9 request.

Form 1099-NEC Line by Line

The 1099-NEC is a short form that produces a long downstream effect when filled correctly. The lines and boxes:

- Payer's name, address, and telephone. The reporting entity. Must match the entity name on the EIN registration and the federal tax return exactly.

- Payer's TIN. The EIN of the payer entity. Same EIN on every 1099 in the batch.

- Recipient's TIN. The taxpayer identification number from W-9 Part I. SSN for sole proprietors and disregarded-entity single-member LLCs (XXX-XX-XXXX). EIN for corporations, partnerships, multi-member LLCs, and trusts (XX-XXXXXXX).

- Recipient's name. The Line 1 name from the W-9 (the legal name, exactly as filed on the recipient's income tax return). A mismatch between the 1099 name and the IRS records for the recipient's TIN is the single most common reason the IRS issues a CP2100 or CP2100A B-Notice.

- Street address, city, state, ZIP. The recipient's mailing address from W-9 Lines 5 and 6. This is where the recipient copy is mailed in January.

- Account number. Optional, used when a payer files more than one 1099 for the same recipient or wants an internal vendor identifier on the form.

- Box 1: Nonemployee compensation. The gross dollar amount of services paid to the recipient during the calendar year. This is the only required money box on the NEC. Includes the full payment for services, not netted against any expenses the recipient billed separately.

- Box 2: Payer-made direct sales of $5,000 or more. A check-the-box field for consumer-product direct sales, rarely used by typical small businesses.

- Box 3: Reserved (intentionally blank in the current edition).

- Box 4: Federal income tax withheld. The dollar amount of backup withholding, if any. Triggers a Form 945 obligation: the payer must deposit the withheld amount with the IRS on the payer's regular payroll-tax deposit schedule and report the total annually on Form 945.

- Boxes 5-7: State income tax withheld, State / Payer's state no., State income. Used when state copies are filed and the state has income tax withheld or different amounts than the federal Box 1.

The payer fills everything. The recipient receives a copy and uses it to file their own return; the recipient does not return the 1099 to the payer.

The 2026 Deadline Calendar

The 2026 calendar for the 1099 family compresses everything into the first quarter:

- 1099-NEC. January 31, 2027 (for tax year 2026 payments) to both the recipient and the IRS. There is no separate later deadline for IRS submission; the NEC has the same date for both copies. This was the entire reason the IRS revived the NEC in 2020.

- 1099-MISC. January 31, 2027 to the recipient. IRS deadline is February 28, 2027 if paper-filed, March 31, 2027 if e-filed.

- 1099-K, 1099-DIV, 1099-INT. Recipient copy by January 31, IRS copy by February 28 paper or March 31 electronic, same pattern as MISC.

- 1099-R. Recipient copy by January 31, IRS copy by February 28 paper or March 31 electronic.

- Form 1096 (paper transmittal). Same deadline as the IRS copy of the 1099 type it transmits.

The 30-day extension is available through Form 8809 (Application for Extension of Time to File Information Returns), but with a hard caveat: Form 8809 extends only the IRS deadline. The January 31 recipient deadline is not extendable. A payer who files Form 8809 buys time to fix data, not time to delay the contractor copy. The recipient copy is also not extendable on appeal; the IRS treats the late recipient copy as a separate failure with separate penalties.

Penalties for late or missing 1099s scale by how late and how many. Under IRC Section 6721, the per-form penalty in 2026 is approximately $60 if filed within 30 days, $130 if filed by August 1, $330 thereafter, and $660 (with no cap) for intentional disregard. The recipient-copy failure under Section 6722 is a separate penalty at the same scale, which means a missing 1099 costs roughly double its first-look fine.

The 10-Return E-Filing Threshold (the Rule Most Payers Missed)

The IRS dropped the e-filing threshold from 250 information returns to 10 aggregate information returns, effective for returns filed on or after January 1, 2024 (i.e., tax year 2023 filings). The rule is in IRS REG-102951-16 and codified at Treasury Regulation 301.6011-2.

The two parts of the rule that make it a sharper edge than the 250 threshold ever was:

- Aggregation across information-return types. The 10 includes every 1099 variant the payer files plus every W-2, every 1095 (Affordable Care Act), every 1098 (mortgage interest), and the other information returns the regulation enumerates. A payer with 4 W-2 employees and 7 contractors crosses the threshold even though no single form-type count crosses 10.

- No grandfather for paper habits. Payers that have always paper-filed are now required to e-file unless they qualify for a hardship waiver under Form 8508. The waiver is narrow and not granted for the year-after-year cost of e-filing software.

The practical result is that almost every US small business with a payroll and any contractor activity is now in the e-file population. The available paths:

- IRS FIRE (Filing Information Returns Electronically). The original e-file system for the 1099 family. Still operational, but the IRS is migrating to IRIS.

- IRS IRIS (Information Returns Intake System). The newer free e-file portal launched in January 2023, designed for the small-business population pulled in by the 10-return threshold. Supports 1099 series, no special software, free.

- Authorised third-party filer. Most payroll providers (Gusto, ADP, Justworks, QuickBooks, Rippling, etc.) file the 1099s as part of payroll service. Many AP and accounting tools also offer 1099 e-filing add-ons.

- Paper file under 10 aggregate. Still allowed when the payer is genuinely below 10 returns across all types. The payer mails Copy A to the IRS along with a Form 1096 transmittal.

The threshold has shifted the operational pressure forward. The historical December-and-January scramble for paper W-9s and a Form 1096 binder is now an e-file batch that depends on data quality. The payer-side discipline that matters is the W-9-at-onboarding and the TIN-matching at intake, because a clean W-9 file is what makes the e-file batch a one-click export instead of a B-Notice queue.

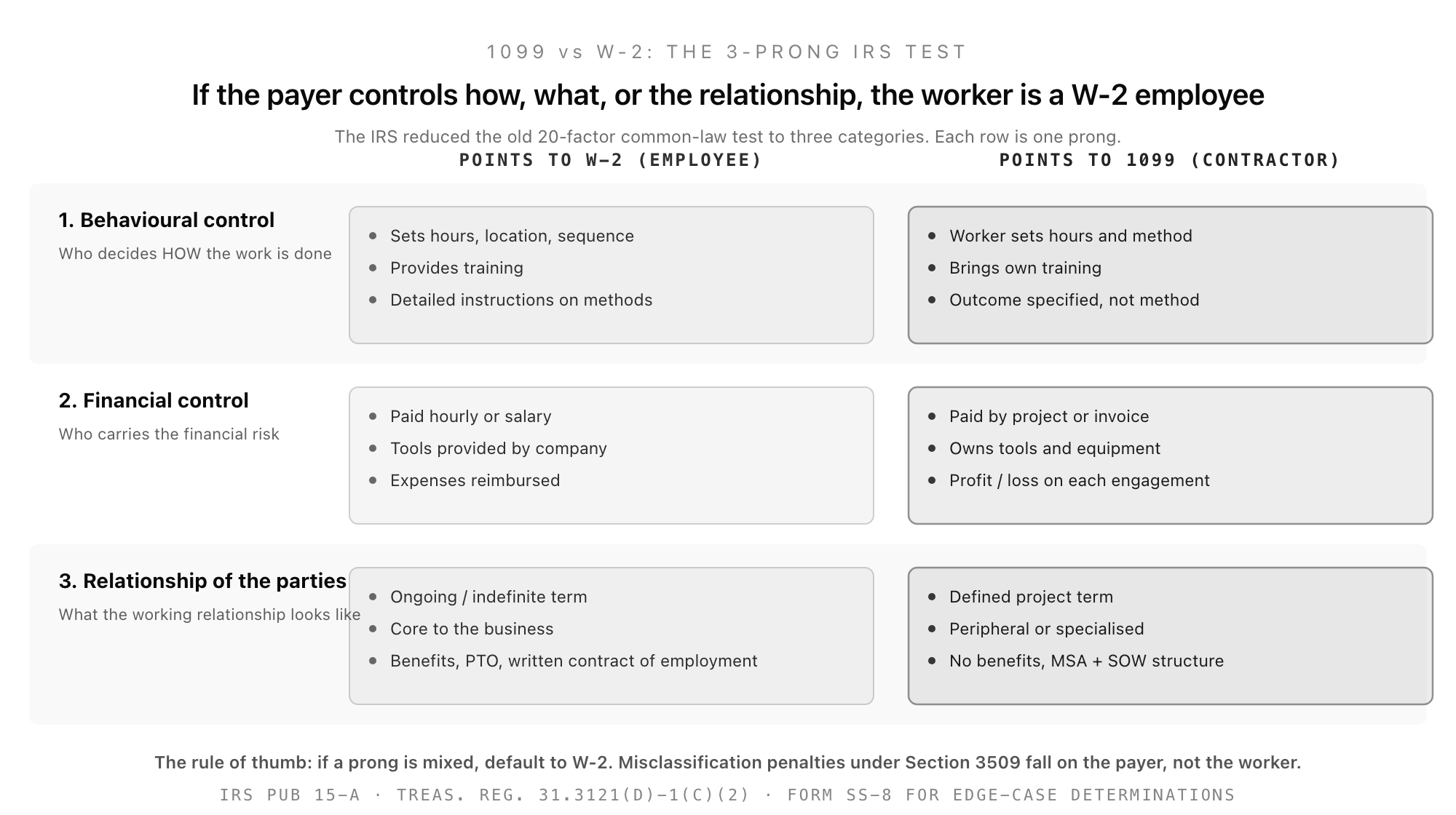

1099 vs W-2: The Three-Prong IRS Test

The single most expensive 1099 decision a small payer makes is the upstream one: whether the worker is a 1099 contractor or a W-2 employee. Collecting the wrong form does not change the worker's legal classification; it is the signal the IRS uses to start auditing.

The IRS reduced the old 20-factor common-law control test (the one most accountants still talk about) to three categories that the IRS examiner walks through on Form SS-8 determinations and in payroll audits:

1. Behavioural control. Who decides how the work is done? Indicators that point to W-2: the payer sets the worker's hours, the location of the work, the sequence of tasks, the tools and methods, and provides training. Indicators that point to 1099: the worker sets their own hours, uses their own tools, decides how to accomplish the deliverable, and brings their own training (often offered to other clients).

2. Financial control. Who carries the financial risk? Indicators that point to W-2: paid hourly or salary on a fixed schedule, tools and equipment provided by the company, business expenses reimbursed. Indicators that point to 1099: paid by project or invoice, owns the tools and equipment used for the work, takes a profit or loss on each engagement, often works for multiple clients in the same period.

3. Relationship of the parties. What does the working relationship look like? Indicators that point to W-2: ongoing or indefinite term, work core to the business's operations, benefits and PTO, a written contract of employment. Indicators that point to 1099: defined project term with an end date, work peripheral or specialised (legal, design, accounting, etc.), no benefits, a master services agreement plus a scope-of-work structure.

The IRS does not require all indicators in one column. The test is a totality-of-the-circumstances weighing, and the IRS examiner has wide discretion. The rule of thumb the small-business audit literature converges on: if any prong is mixed, default to W-2 + W-4. The cost of treating a contractor as a W-2 when the IRS would have accepted 1099 is roughly 7.65% in employer FICA. The cost of treating a W-2 as a 1099 when the IRS reclassifies is the unpaid employer FICA share, the income tax that should have been withheld, both halves of FICA the worker should have had withheld, penalties under Section 3509 of the Internal Revenue Code, and interest from the date of the misclassified payment.

Section 530 of the Revenue Act of 1978 (uncodified, but still in force) provides a narrow safe-harbor that prevents reclassification penalties if the payer has a documented reasonable basis for the contractor treatment, has treated similar workers consistently, and has filed all required 1099s for the workers it classified as contractors. The Section 530 protection is a refuge for payers with paperwork, not a defence for payers without it. The payers who lose 530 challenges almost always lose them because they never filed the 1099, which removes the third requirement of the safe-harbor and the rest of the analysis stops there.

The Form SS-8 process is the safety valve for edge cases. Either party (payer or worker) can file SS-8 to ask the IRS for a determination on whether the worker is an employee or contractor. The determination is not binding on the worker's tax return, but it is the cleanest cover the payer can get when the classification is genuinely close. The trade-off is that SS-8 takes 6 months or longer for a written determination, and the act of filing SS-8 is itself an audit signal.

For the W-2 side of the line, see the W-2 form: a 2026 employer's guide and the W-4 form: a 2026 employer's guide. The combination of W-9 plus 1099-NEC on the contractor side and W-4 plus W-2 on the employee side is the federal-form quad every US small employer in 2026 has to keep clean.

Form 1096: The Cover Sheet for Paper Filers

Form 1096 is the Annual Summary and Transmittal of US Information Returns, the paper cover sheet a payer attaches when mailing Copy A of paper 1099s to the IRS. One Form 1096 per form type per batch: separate 1096s for the 1099-NEC batch, the 1099-MISC batch, the W-2 batch (though W-2 uses Form W-3, not 1096), and so on. The 1096 carries the totals of the forms in the batch (number of forms, total federal income tax withheld, total reported amount) for the IRS to sanity-check against the individual forms.

Form 1096 is increasingly a paper-only artefact. E-filers do not file 1096 because the e-file system carries the same batch totals in the file header. With the 10-return e-filing threshold pulling almost every small payer into electronic submission, the population that still needs Form 1096 is small: payers filing genuinely under 10 returns who choose paper, and payers filing on a hardship waiver. For everyone else, 1096 is a vestige that the e-file path makes redundant.

The narrow case that comes up: Copy A of a 1099 (the IRS copy) is printed on red-drop-out ink that the IRS scanner reads. The standard 8.5"x11" red-ink form is the only acceptable paper Copy A; printing Copy A on a laser printer from a black-and-white PDF is rejected by the IRS scanner. Payers who paper-file have to order the IRS-printed red-ink Copy A from the IRS forms portal or buy it from an office-supply store that stocks the official red form. The recipient copies (Copy B, Copy C, Copy 2) can be plain black-and-white printouts.

State Copies: The CFSF Program and the 35-State Mandate

Federal 1099 filing is half the obligation. Most US states also require a state copy of certain 1099s, and the rules are not uniform.

The 2026 state map breaks roughly into three groups:

- States with no income tax (no 1099 state filing required). Florida, Texas, Tennessee, Nevada, South Dakota, Wyoming, Alaska, New Hampshire (interest and dividend tax only), and Washington (capital gains tax only). Payers with recipients in these states file federal 1099 only.

- CFSF (Combined Federal/State Filing) participating states. Around 30 states participate in the IRS CFSF program, which auto-forwards 1099 data filed with the federal IRS to the participating state. Payers who file federally through FIRE or IRIS, mark the CFSF participation box, and use the correct state code in Boxes 5-7 do not have to file separately with those states. The participating states change year to year; the IRS publishes the current list in Publication 1220.

- States that require separate state filing. Around 8-10 states require a separately filed state 1099 even if the payer files federally through the CFSF system. California, Pennsylvania, Massachusetts, Oregon, and several others are typically in this group. The state thresholds and forms vary; some states require only 1099-NEC, some require the full family.

The clean state-side workflow is: pick an e-filing path that opts into CFSF for participating states, use the correct state codes in Boxes 5-7 on every 1099 that has state-tax content, and identify the separately-filing states the payer's recipients live in. Most third-party filers (Gusto, ADP, QuickBooks, Track1099) handle the CFSF box and the state-by-state separate filings transparently.

Corrections: Type 1 vs Type 2 Errors

The 1099 corrections process is in IRS Publication 1220 and splits errors into two categories:

- Type 1 error: wrong amount, wrong code, wrong checkbox. The corrected 1099 has the right data, is marked CORRECTED in the header, and is filed as a single replacement. No VOID step is needed because the recipient name and TIN are unchanged.

- Type 2 error: wrong payee name, wrong TIN, wrong form type, or a 1099 issued that should not have been issued at all. A two-step correction: file a 1099 with the original (wrong) data and tick the VOID box, then file a separate corrected 1099 with the right data marked CORRECTED. The VOID step tells the IRS to remove the original; the CORRECTED step tells the IRS to add the new one.

The corrections must be filed on the same path as the original (paper or electronic, generally electronic now). Corrections trigger their own deadline rules: a correction filed within 30 days of the original error generally avoids the Section 6721 late-filing penalty for the error; corrections filed later carry the scaled penalties. The cleanest correction posture is a regular post-filing reconciliation in early February against the recipient's records and the payer's AP ledger, so any errors surface inside the 30-day window.

A recipient who reports an error to the payer (the contractor noticing their TIN or address is wrong on the recipient copy) should be treated as a paid-attention signal. The payer who corrects on the contractor's flag usually catches the error before the IRS does, which keeps the correction at the lowest-penalty tier.

A January 1099-NEC Workflow that Does Not Set Anyone's Hair on Fire

The reason January 1099 season feels chaotic is that the work is procedural and the data is fragmented across the AP ledger, the contract files, and the W-9 binder. The fix is to put the pieces in the same place during the year, not in January.

The Good Form 1099-NEC workflow in 2026:

- At contractor onboarding (day 0). Collect the W-9 intake with Line 1 name, Line 3a entity type, the TIN, and the four Part II certifications. Run the TIN through IRS TIN Matching. Attach the result to the vendor record.

- At every payment. AP system tags each invoice with the vendor's W-9 metadata: the recipient name from Line 1, the TIN from Part I, the corporate-exempt flag from Line 3a, and the year-to-date Box 1 running total. A flag fires automatically when the recipient crosses $600.

- Late November / early December. Pull a draft 1099 batch: every non-exempt vendor with $600 or more in Box 1 payments. Run a second TIN Match on any new vendor that joined mid-year. Reconcile the Box 1 totals against the AP ledger.

- Early January. Run the 1099-NEC prep template per vendor: payer block (consistent across the batch), recipient block (auto-pulled from the W-9), Box 1 amount, Box 4 backup withholding if any. The prep template is the structured pre-flight check that gates the e-file submission, not the e-file itself.

- By January 31. E-file the 1099-NEC batch through IRIS or the payer's third-party filer. Print and mail the recipient copies on the same day. Mail or upload the state copies for states that do not participate in CFSF.

- February. Reconcile against contractor questions about their recipient copies. File Type 1 corrections for any amount errors that surface; file Type 2 corrections for any name or TIN errors. Track any state separate-filings the payer is behind on.

The Good Form workspace plugs into this loop at three points: the W-9 intake collects the year-end recipient data at the start of the relationship instead of in January; the new hire information template catches the misclassification check at onboarding for any worker the payer is unsure about; and the 1099-NEC prep template turns the January batch into a structured walk-through of the eight or nine fields each 1099 needs, with the TIN-Match status flag and the corporate-exemption check baked in.

Start by cloning the Good Form 1099-NEC payer prep template and running every active contractor through it in the next batch. The work-of-the-year payoff is that January is a one-click export with no B-Notices, no Section 3509 exposure on a misclassified worker, and no scrambled-deposit Form 945 obligation from an unrecorded backup-withholding event.