The W-9 form is the federal Request for Taxpayer Identification Number and Certification that every US payer collects from every independent contractor, freelancer, vendor, royalty recipient, and other 1099 payee before issuing the first payment. The current edition is Form W-9 (Rev. March 2024), which kept the same seven-line structure but tightened Line 3 by adding a new Line 3b that explicitly captures the LLC sub-classification (C, S, or P). The form is short, the payee fills the whole thing, the payer files nothing with the IRS, and yet it is the single piece of paperwork that decides whether the year-end 1099 cycle is a calm export or a 24% backup-withholding scramble.

This guide is the line-by-line walkthrough of Form W-9 for a US payer in 2026: what each line collects, when to send it (and when not to), how the Line 3 classification decides which 1099 you owe at year-end, the four Part II certifications and the one that gets struck out, the backup-withholding triggers and the 24% rate, the TIN-matching process the IRS gives payers for free, the retention rule that is different from the W-4 retention rule, and the W-9 versus W-4 line that small companies cross when they accidentally treat a contractor like an employee. The audience is the same one we have been writing for through the federal-form triad: small finance and HR teams of one to ten, office managers who run payroll and AP from the same browser tab, and operations leads who just had a contractor send a $4,500 invoice and asked whether the company is supposed to file something at year-end. If you want a pre-payment intake that collects Line 1 name, the Line 3 classification, the TIN, and the four Part II certifications from a new contractor before the first invoice posts, clone the Good Form W-9 intake template.

The short version:

- Form W-9 is a one-page IRS form the payee gives the payer so the payer has a verified legal name and taxpayer identification number (TIN) on file. The payer keeps it. The IRS never sees it directly.

- Request a W-9 before the first payment, not at year-end. Year-end requests are the single biggest source of backup-withholding penalties because the contractor has already left and the TIN never arrives.

- The seven lines collect: (1) legal name, (2) DBA, (3a) federal tax classification, (3b) LLC sub-class C/S/P, (4) exempt payee and FATCA codes, (5-6) address, Part I TIN (SSN or EIN), and Part II four certifications.

- The Line 3 classification decides everything downstream: which TIN type goes in Part I, whose name goes on Line 1, and whether you owe a 1099 at year-end. Most C and S corporations are exempt from 1099 reporting; sole proprietors and partnerships are not.

- Backup withholding kicks in at 24% when the payee fails to provide a TIN, provides an incorrect TIN, fails to certify the TIN, or has been flagged by the IRS for unreported interest or dividends. The payer is liable if it does not withhold when required.

- The IRS TIN Matching program lets payers verify a W-9 name and TIN against IRS records before filing the 1099. It is free, requires an e-Services account, and prevents almost every B-Notice the payer would otherwise receive.

- Retention: keep every signed W-9 on file for as long as the payee relationship lasts, plus four years after the due date of the last 1099 the W-9 fed into.

- W-9 is for independent contractors and other payees (1099). W-4 is for employees (W-2). Collecting the wrong one is the misclassification signal the IRS looks for when auditing payroll.

What the W-9 Form Is and Why It Exists

Form W-9, formally the Request for Taxpayer Identification Number and Certification, is the document a US payer asks every non-employee payee to complete before the first reportable payment. It collects the payee's legal name, business or trade name, federal tax classification, address, and taxpayer identification number, and it includes a four-part certification that the information is accurate and that the payee is not currently subject to backup withholding.

The form has existed in its modern shape since the 1980s, but the current edition is Form W-9 (Rev. March 2024), which is the version every US payer should be sending in 2026. The March 2024 revision is the result of the IRS responding to two specific patterns. First, single-member LLCs and disregarded entities were filling Line 3 incorrectly so often that the IRS split the old "Limited liability company" checkbox into a Line 3a entity-type selection plus a new Line 3b sub-classification (C, S, or P) that is required only when the entity on Line 3a is an LLC taxed as a corporation or partnership. Second, the IRS clarified that single-member LLCs that are disregarded entities for federal tax purposes do not use Line 3b at all: they tick the Individual / sole proprietor box on Line 3a and put the owner's name on Line 1.

The form is never sent to the IRS. The payer keeps it on file. The IRS only sees the information that the payer copies onto the 1099 at year-end.

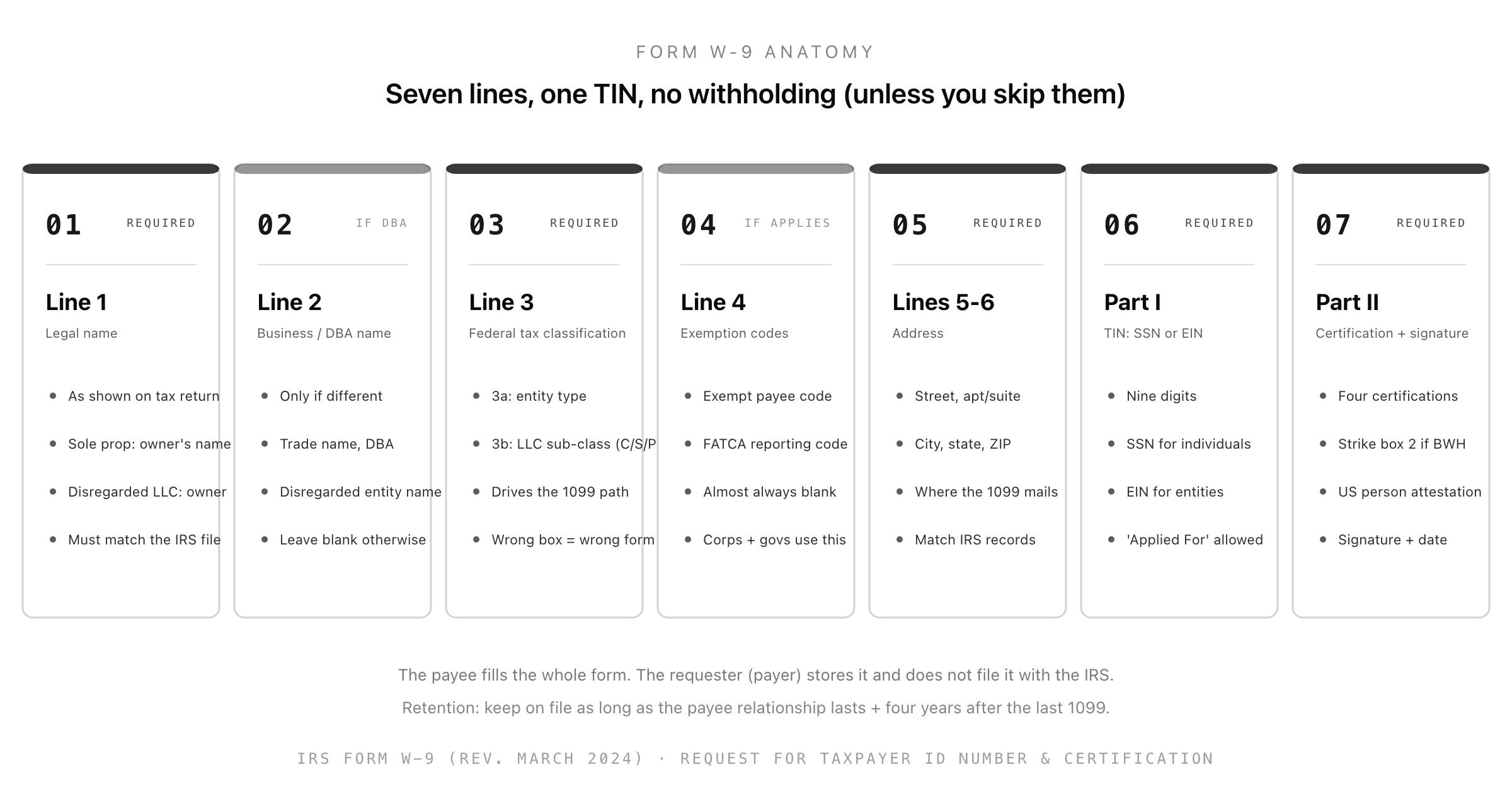

Form W-9 Anatomy

The seven lines and two parts split into four jobs the form does in order: identity (Lines 1 and 2), classification (Lines 3a and 3b), location and exemptions (Lines 4 to 6), and the TIN and certifications (Parts I and II). The rest of this guide walks each one.

When to Request a W-9

The trigger for requesting a W-9 is the start of any payee relationship that might result in a year-end information return. The standard list:

- Independent contractors, freelancers, consultants, and any non-employee paid for services

- Vendors that provide services as part of the trade or business, even one-time

- Landlords receiving rent of $600 or more in a year (paid in the course of trade or business)

- Attorneys, regardless of corporate status, for any legal services payment

- Medical and health-care service providers (corporate exemption does not apply)

- Royalty recipients paid $10 or more

- Anyone receiving prizes, awards, or other non-employee compensation likely to hit $600

The mistake to avoid is sending the W-9 request after the work is done. The IRS rule is unambiguous: the payer is required to begin backup withholding the moment a payment is made to a payee who has not provided a TIN. Most small companies do not actually backup-withhold because they trust the contractor to fix the paperwork before year-end, but the legal exposure is real, and the contractor leaving without ever sending the W-9 (which happens more than people expect) leaves the payer either filing the 1099 with a blank TIN and getting a B-Notice, or eating the under-withheld amount as a payer-paid backup withholding liability.

The Good Form workflow puts the W-9 intake into contractor onboarding alongside the master services agreement and the first scope of work, which is the moment the contractor cares most about getting it right. Sending the request a week after the first payment is approximately ten times harder.

Line 1: Legal Name

Line 1 is the name as it appears on the payee's income tax return. The rule is exact-match, not close-enough.

- Individuals (including sole proprietors and single-member LLCs that are disregarded entities): the owner's individual legal name. Not the business name. The owner's social security card name.

- C and S corporations, partnerships, multi-member LLCs taxed as partnerships or corporations: the entity's legal name as registered with the IRS (the name on the EIN application or the Articles of Incorporation).

- Trusts and estates: the legal name of the trust or estate, not the trustee or executor's personal name.

A Line 1 mismatch is the single most common reason the IRS issues a CP2100 or CP2100A notice (the B-Notice) to the payer. The IRS computer matches Line 1 against the TIN in Part I; if the name on file with the SSA or the IRS for that TIN differs from the name on the 1099, the notice is triggered and the payer is required to begin backup withholding within 30 days unless the payee fixes the W-9.

Line 2: Business Name, DBA, or Disregarded Entity Name

Line 2 is optional and only used when the payee's business name, trade name, or DBA is different from Line 1. The 1099 prints both, and downstream automation matches on Line 1 only.

The narrow case that matters: a sole proprietor with a DBA puts the owner's individual name on Line 1 and the DBA on Line 2. The TIN in Part I is the owner's SSN (preferred) or the EIN issued in the DBA's name. A common error is putting the DBA on Line 1 and the individual name on Line 2, which inverts the IRS match and triggers a B-Notice at year-end.

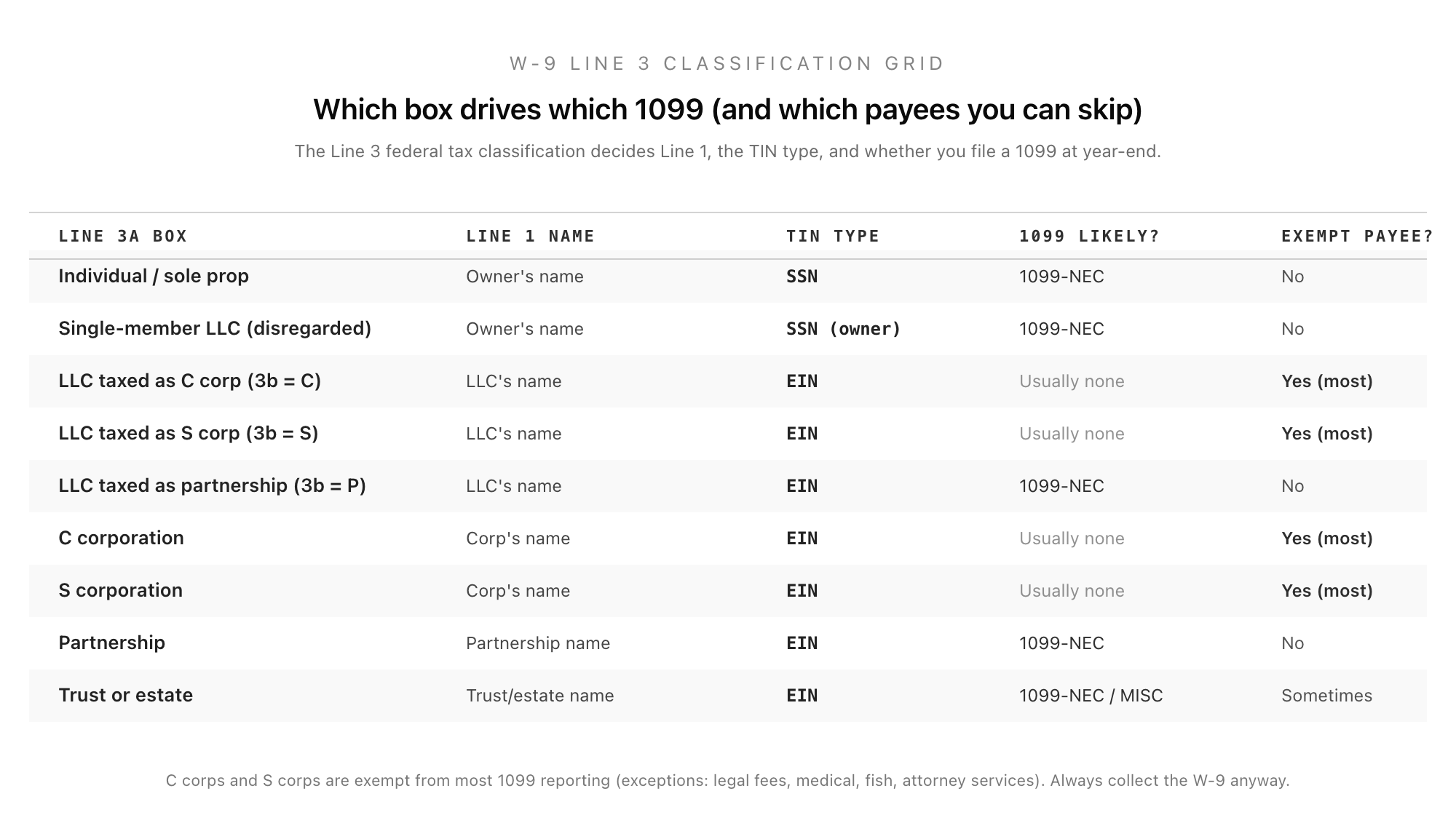

Line 3a: Federal Tax Classification

Line 3a is the single most important line on the W-9 because it drives every other decision downstream: which name goes on Line 1, which TIN goes in Part I, whether the payer files a 1099 at year-end, and which 1099 form is the right one. The seven options the March 2024 revision recognises:

- Individual / sole proprietor. Used by individuals and by single-member LLCs that have not elected corporate taxation (which are disregarded entities by default). Line 1 is the owner's name; Part I uses the owner's SSN.

- C corporation. Line 1 is the corporation's name; Part I uses the EIN. Most payments to C corporations are not 1099-reportable, with specific exceptions for legal services, medical and health services, fish purchases, and a handful of other categories.

- S corporation. Same Line 1 and Part I treatment as a C corporation. Same exemption logic.

- Partnership. Line 1 is the partnership name; Part I uses the EIN. Partnerships are not exempt from 1099 reporting; payments of $600+ in services are 1099-NEC reportable.

- Trust or estate. Line 1 is the trust or estate name; Part I uses the trust or estate EIN. Reporting varies by payment type.

- Limited liability company (LLC) taxed as a C corporation, S corporation, or partnership. This is the only Line 3a option that triggers Line 3b. The LLC's name goes on Line 1; Part I uses the LLC's EIN.

- Other. Used by foreign entities, government entities, certain tax-exempt organisations, and other categories. Most US payers do not see this option.

The Line 3a selection has a side effect that small companies miss: it decides the 1099 form. Services to a sole proprietor, partnership, or partnership-taxed LLC produce a 1099-NEC for non-employee compensation. Rent paid to a non-corporate landlord produces a 1099-MISC box 1. Royalties of $10+ produce a 1099-MISC box 2. Attorney fees produce a 1099-NEC even if the attorney is a corporation. The W-9 Line 3a does not pick the form for the payer, but it determines which forms are even available for that payee.

Line 3b: LLC Sub-Classification (Only When Line 3a Is LLC)

Line 3b is the March 2024 revision's clean-up of the most-mis-filled W-9 in the IRS's experience. It is required only when Line 3a is set to LLC; otherwise it stays blank.

- C. The LLC has elected corporate taxation and is treated as a C corporation. Same exemption treatment as a native C corp.

- S. The LLC has elected S corporation taxation. Same exemption treatment as a native S corp.

- P. The LLC is multi-member and taxed as a partnership by default. Not exempt from 1099 reporting.

The trap the March 2024 revision was designed to fix: single-member LLCs that are disregarded entities for federal tax purposes do not use Line 3a's LLC option at all. They tick Individual / sole proprietor on Line 3a and put the owner's individual name on Line 1, with the owner's SSN in Part I. The disregarded-entity LLC's name goes on Line 2 if there is a DBA. Filling Line 3b with the LLC's checkbox in this case is the IRS's most-flagged W-9 error and the most common reason a disregarded-entity contractor's 1099 mismatches at year-end.

The classification grid above maps every Line 3a / Line 3b combination to the correct Line 1, TIN type, and 1099 path.

Line 4: Exempt Payee Code and FATCA Reporting Code

Line 4 has two boxes that are blank on almost every W-9 a small US payer will ever receive.

- Exempt payee code. A one-digit code (1 through 13) that identifies the payee as a category exempt from 1099 backup withholding. The most common code is 5 (corporations exempt under section 6049(b)(4)), used by C and S corps to flag their corporate exemption to the payer. The official W-9 instructions list every code. Individuals do not use this box.

- FATCA reporting code. A one-letter code (A through M) used by accounts maintained outside the US. Almost always blank for US payers paying US contractors.

The two codes are independent. Most W-9s a US small-business payer collects will have both boxes empty, which is correct.

Lines 5 and 6: Address

Address (street and apt/suite on Line 5, city/state/ZIP on Line 6) is the address the year-end 1099 mails to. It must match the address the payee uses on the income tax return for the year the 1099 covers. Address changes mid-year are common; the payer should ask for an updated W-9 whenever a contractor moves, or accept a written statement attached to the existing W-9.

The address is also where the IRS sends any tax-related notice that flows from a 1099 mismatch, which is the second reason it has to be right.

Line 7: Account Numbers (Optional)

Line 7 is rarely used. The requester (payer) can ask the payee to write account numbers maintained between the two parties (vendor numbers, internal accounting codes) for the requester's own record-keeping. Most payers leave it blank and add the internal vendor ID to their AP system after receipt.

Part I: Taxpayer Identification Number

Part I is two boxes: the social security number box (nine slots, XXX-XX-XXXX format) and the employer identification number box (nine slots, XX-XXXXXXX format). The payee fills exactly one of them, never both.

Which box maps to which entity type:

- Individuals, sole proprietors, single-member disregarded-entity LLCs: SSN. A sole proprietor with both an SSN and an EIN can use either, but the IRS prefers the SSN.

- C corps, S corps, partnerships, multi-member LLCs, trusts, estates: EIN.

The narrow case that comes up: a payee whose TIN application is in progress writes "Applied For" in the TIN box and signs the form. The payer must withhold at 24% on every reportable payment until the actual TIN arrives, or take written certification from the payee that the application is pending and treat the W-9 as provisional for 60 days. Most small payers simply hold the first payment until the TIN arrives.

The IRS provides a free TIN Matching service through e-Services that lets the payer verify a Line 1 name + Part I TIN against IRS records before filing the 1099. The service runs the same match the IRS will run at year-end. A pre-filing match catches almost every B-Notice the payer would otherwise receive. Setting up TIN Matching takes one e-Services account and a 48-hour activation; small payers should set it up once and route every new W-9 through it.

Part II: The Four Certifications

Part II is the legal weight of the W-9. The payee signs once at the bottom, certifying four things by signing:

- The TIN is correct (or the application is pending and "Applied For" is in the TIN box).

- The payee is not subject to backup withholding. Specifically: not exempt from backup withholding and not currently flagged by the IRS for unreported interest or dividends or has been notified that the IRS has released the flag. This is the certification the payee strikes out (literally crosses through on the paper form) if the IRS has notified them they are currently subject to backup withholding.

- The payee is a US person. US citizen, US resident alien, US partnership, US corporation, US-domiciled trust or estate. Non-US persons do not file a W-9; they file the W-8 series (W-8BEN, W-8BEN-E, W-8ECI, W-8EXP, W-8IMY) depending on the type of payee and the type of income.

- The FATCA code on Line 4 is correct (only relevant if a FATCA code was entered).

The signature line below the four certifications is the payee's, dated. An unsigned W-9 is not a W-9. The payer must treat the payee as a recipient with no valid TIN, which triggers backup withholding from the first payment.

The certification box 2 strike-out is the one piece of W-9 procedure that comes up surprisingly often. A contractor who is currently subject to backup withholding (for instance, because the IRS flagged unreported 1099 interest from a previous year) cannot sign Part II unmodified. They are required to cross through certification 2 on the form before signing. The payer who receives a W-9 with certification 2 struck out must withhold at 24% on every reportable payment until the IRS issues a release notice to the contractor.

Backup Withholding: When, Why, and How Much

Backup withholding is the 24% federal tax the payer is required to withhold from a 1099-reportable payment when one of four triggers fires:

- No TIN. The payee did not provide a TIN, or provided one that is obviously wrong (less than nine digits, all zeros, etc.).

- Incorrect TIN. The IRS issued a CP2100 or CP2100A B-Notice and the payee did not respond with a corrected W-9 within 30 days.

- No certification. The payee did not sign the W-9, or signed without completing Part II.

- IRS notification of under-reporting. The IRS flagged the payee for unreported interest or dividends from a prior year and sent the payer a C-Notice naming the payee.

The 24% rate is set in section 3406 of the Internal Revenue Code and has been at 24% since the Tax Cuts and Jobs Act of 2017 (it was 28% before). The withholding applies to the gross payment, not the net, and the payer is liable for the under-withheld amount plus penalties if it fails to withhold when required.

Backup-withheld amounts are deposited with the IRS on the same schedule as the payer's payroll tax deposits, reported on Form 945 (Annual Return of Withheld Federal Income Tax), and shown in box 4 of the 1099-NEC or 1099-MISC. The payee gets credit for the withholding on their personal tax return.

Two practical notes on backup withholding. First, it is the payer's exposure, not the payee's; the payer who skips required backup withholding can be assessed for the full amount plus penalties even if the payee eventually pays their own taxes. Second, the 24% applies to the entire 1099-reportable payment, not just the labour portion, which means a $5,000 contractor invoice with no W-9 on file can produce a $1,200 backup-withholding liability if the IRS catches it.

TIN Matching: The Free Pre-Flight Check

The IRS TIN Matching program is the underused tool that prevents almost every B-Notice a small payer would otherwise receive. It is free, runs against the same IRS database that the year-end 1099 match runs against, and is available through the IRS e-Services portal.

Setup takes one principal officer e-Services account, a 48-hour activation, and an application that the IRS approves after a brief vetting. Once active, the payer can submit up to 25 name-TIN pairs per online query or 100,000 per bulk upload. The system returns one of:

- 0 – Match

- 1 – TIN missing or incorrect format

- 2 – TIN not currently issued

- 3 – TIN and name do not match

- 4 – Invalid request

- 5 – Duplicate request

- 6 – Matched on SSN

- 7 – Matched on EIN

- 8 – Matched on either SSN or EIN

A small payer with 5 to 50 contractors a year should run every new W-9 through TIN Matching the day it arrives. A return code other than 0, 6, 7, or 8 means the payer should ask the contractor for a corrected W-9 before the first payment, which is hundreds of times cheaper than fixing it during 1099 season.

Substitute W-9 Forms

Most modern payers do not send the IRS Form W-9 PDF as a fillable file. They use a substitute W-9, which is a digital form that captures the same fields and produces the same legal certification. The IRS explicitly permits substitute W-9 forms under IRS Publication 1281 (Backup Withholding for Missing and Incorrect Name/TINs), provided the substitute form:

- Captures every field on the official Form W-9.

- Includes the exact Part II certification language (the four certifications cannot be summarised or paraphrased).

- Captures an electronic signature that records the date and authenticates the signer (a typed full name plus a timestamp meets this when paired with an audit trail).

- Allows the payee to strike certification 2 if they are currently subject to backup withholding.

The Good Form W-9 intake template at /templates/w-9-intake is a substitute W-9 in this exact sense: it captures Line 1 through Part II, it preserves the four Part II certifications as separate confirm-boxes (so the contractor can decline certification 2 by leaving it unchecked, which triggers a notes field for the strike-out reason), and it stores the typed signature and timestamp as the audit trail. It does not replace the official Form W-9 PDF for vendors that require the IRS file by policy; for those vendors, the captured fields make the PDF a five-minute copy-paste rather than an hour of email back-and-forth.

W-9 Retention

Keep every signed W-9 on file for as long as the payee relationship lasts, plus four years after the due date of the last 1099 the W-9 fed into. The four-year tail is the IRS's general assessment-statute window for information-return penalties under section 6501(e), and it is the same window the W-9 has to be producible in case the IRS audits the 1099 filings.

Some specifics that come up:

- A contractor relationship that ends in 2026 with a final 1099 due 31 January 2027 has a W-9 retention requirement through 31 January 2031.

- A W-9 that produces a corrected 1099 in a later year extends the retention to four years after the corrected 1099's due date.

- A contractor who returns to the payer after a gap of more than three years should provide a fresh W-9, both because circumstances change and because the IRS expects a current W-9 on file at the time of payment.

Retention does not have to be on paper. Digital storage is acceptable as long as the file is producible, legible, and tied to the timestamp and audit trail. Most modern AP systems keep the W-9 attached to the vendor record and surface it on every 1099 export.

W-9 vs W-4: The Misclassification Line

The single biggest mistake small payers make in the federal-forms world is collecting the wrong form: a W-9 from someone who is actually an employee, or a W-4 from someone who is actually a contractor. The form does not change the worker's classification, but it is the signal the IRS uses to start auditing payroll.

The legal test for employee vs contractor is the common-law control test (the IRS calls it the "three categories" test: behavioural control, financial control, and the relationship of the parties). The IRS Form SS-8 is the canonical worker-classification determination request. Treasury Regulation 31.3121(d)-1(c)(2) is the underlying authority.

The practical short form, from a payer's perspective:

- W-4 + W-2: the company controls how the work is done, sets hours and tools, integrates the worker into the team. Federal income tax, social security, and Medicare are withheld from each paycheck. The company pays the employer share of FICA.

- W-9 + 1099: the worker controls how the work is done, brings their own tools, sets their own hours, often works for multiple clients. No federal income tax is withheld unless backup withholding applies. No employer FICA share. The worker pays self-employment tax on their own return.

Collecting a W-9 from a worker who is functionally an employee saves about 7.65% in employer FICA in the short term and creates a six-figure misclassification liability if the IRS audits. The IRS Section 530 safe-harbor exists but is narrow. Most small payers err on the side of W-2 + W-4 when the work is ongoing and W-9 + 1099 when the work is a defined deliverable, and they document the classification call.

For the W-4 (employee) walkthrough that pairs with this article, see the W-4 form: a 2026 employer's guide. For the I-9 employment-eligibility piece that completes the federal-form triad, see the I-9 form: a 2026 employer's guide.

A Day-One Workflow for the W-9

The reason year-end 1099 cycles go wrong is that the W-9 is collected late. The fix is procedural, not technical: put the W-9 intake into the same onboarding moment as the master services agreement and the first scope of work.

The Good Form contractor-onboarding pattern in 2026 looks like:

- Day 0 (offer accepted). Send the master services agreement (MSA) and the W-9 intake template in a single email. Contractor signs both within 48 hours.

- Day 1 (intake submitted). TIN Match the captured Line 1 + TIN through IRS e-Services. Resolve any mismatch with a corrected intake before the first scope.

- Day 2 (first scope of work). Attach the first SOW. Contractor returns countersigned. AP system creates the vendor record with the W-9 and the TIN-Match result attached.

- First payment. Issues from the AP system against the vendor record. No backup withholding unless the W-9 missed certification 2 or the TIN Match returned a mismatch.

- Mid-year address or entity change. Contractor submits a fresh intake. AP updates the vendor record. The old W-9 stays in the file with the date superseded.

- Year-end (31 January). 1099-NEC issues automatically from the AP system. Every vendor has a verified, TIN-matched W-9 on file. Zero B-Notices.

The Good Form workspace is built for this loop: contractor-onboarding forms feed AP systems via API, the W-9 intake template drops into an onboarding workflow in a click, and the captured data is structured cleanly enough for any AP system to ingest. Combined with the I-9 intake, W-4 intake, and new-hire information template, the federal-form triad covers every day-one paperwork moment a US small employer encounters in 2026, on either the employee or the contractor side of the misclassification line.

Start by cloning the Good Form W-9 intake template and putting it into your contractor-onboarding sequence today. The work-of-the-year payoff is that next January's 1099 cycle is a one-click export with no B-Notices and no scrambling backup withholding.