The Form 1095-C is the statement an Applicable Large Employer sends to each of its full-time employees, and files with the IRS, to report whether it offered health coverage that met the Affordable Care Act's standards. If you employed roughly fifty or more full-time and full-time-equivalent people last year, the 1095-C is how you document, month by month, what coverage you offered, what the cheapest version cost the employee, and why no employer-mandate penalty should apply. It is not a tax the employee pays or a form they fill in. It is your evidence, filed under the 1094-C transmittal, that you met the employer shared responsibility rules.

This is the 2026 walkthrough of the form 1095-C for the employer that has to file it: what the form actually does, who counts as an Applicable Large Employer, how it differs from the 1095-A and 1095-B, the Line 14, 15, and 16 code stack that carries all the meaning, the affordability safe harbors, the 1094-C transmittal, the furnishing and e-filing deadlines (with the recent changes that let you furnish on request), and the Section 4980H penalties that the whole exercise exists to avoid. If you want a clean way to capture the per-employee data your filing vendor needs, clone the Good Form 1095-C intake template before the next reporting cycle.

The short version:

- Form 1095-C, Employer-Provided Health Insurance Offer and Coverage, is filed by every Applicable Large Employer (ALE) for each employee who was full-time for at least one month of the year, plus anyone enrolled in a self-insured plan. It reports the offer of coverage under ACA Section 6056.

- An ALE is an employer that averaged 50 or more full-time employees, including full-time equivalents, during the prior calendar year. Full-time means 30+ hours a week or 130+ hours a month. Part-time hours roll up into full-time-equivalents for the headcount test.

- The 1095-C is one of three "1095" forms. The 1095-A comes from the Health Insurance Marketplace, the 1095-B comes from insurers and small self-insured plans, and the 1095-C comes from ALEs. An employer only files the C.

- Part II is the substance, read month by month: Line 14 is the offer-of-coverage code (Series 1: 1A to 1U), Line 15 is the employee's required contribution for the lowest-cost self-only plan, and Line 16 is the Section 4980H safe-harbor code (Series 2: 2A to 2H) that shows why no penalty applies.

- Part III is completed only by self-insured employers, listing each covered individual and their months of coverage. Fully-insured employers leave it blank because the insurer files the 1095-B.

- The affordability test drives Line 15 and the 2F/2G/2H codes. Coverage is "affordable" if the employee's cost for self-only minimum-value coverage stays under an IRS-indexed percentage of income, measured by one of three safe harbors: W-2 wages, rate of pay, or the federal poverty line.

- The forms are filed with the IRS under the Form 1094-C transmittal, the C's equivalent of the W-3 for W-2s or the 1096 for 1099s. Electronic filing through the AIR system is mandatory once an employer files 10 or more information returns of any type in aggregate.

- Deadlines: furnish the 1095-C to employees by early March; file with the IRS by February 28 on paper or March 31 electronically. Under the Paperwork Burden Reduction Act, ALEs may now post a notice and furnish the 1095-C only on request.

- The penalties are real on two fronts: information-return penalties under Sections 6721 and 6722 for late or wrong forms, and the Section 4980H employer shared responsibility payments for failing to offer affordable, minimum-value coverage to full-time staff. The 1095-C is how you prove you owe neither.

What the Form 1095-C Is and Who Files It

The Affordable Care Act created an "employer mandate," formally the employer shared responsibility provisions of Internal Revenue Code Section 4980H. Larger employers are expected to offer affordable health coverage that meets a minimum value standard to their full-time employees, or face a payment if a full-time employee instead buys subsidized coverage on the Marketplace. The IRS needs a way to see who offered what, and the Form 1095-C is that reporting mechanism, authorized by Section 6056.

Every Applicable Large Employer files a 1095-C for each person who was a full-time employee for at least one month of the calendar year. If the employer also self-insures its health plan, it files a 1095-C for any other individual (a part-time employee, a covered family member) who enrolled in that plan, because a self-insured ALE also has to do the Section 6055 minimum-essential-coverage reporting that would otherwise live on a 1095-B. The employee does nothing with the form except keep it; since the individual mandate penalty was zeroed out at the federal level, most employees no longer even need it to file their personal return. The form's real audience is the IRS.

The 1095-C sits next to the rest of an employer's annual federal filings. The same business files a W-2 for each employee's wages and a 1099-NEC for contractor payments. The 1095-C is the health-coverage filing in that same January-to-March reporting season, running on its own legal track (the ACA) rather than the payroll-tax track.

Applicable Large Employer: The 50-Employee Gate

Everything about 1095-C reporting hinges on whether you are an ALE, and that is a headcount question measured over the prior calendar year. An employer is an ALE for the current year if it employed an average of 50 or more full-time employees, including full-time equivalents (FTEs), during the previous year.

The math has two pieces. First, count your genuine full-time employees: anyone averaging 30 or more hours a week, or 130 or more hours in a month. Second, convert your part-time hours into full-time-equivalents: add up all the hours worked by part-timers in a month (counting no more than 120 hours per person), and divide by 120. That gives the FTE count for the month. Add full-time employees plus FTEs for each of the twelve months, average across the year, and if the result is 50 or more, you are an ALE.

Two traps catch employers here. The aggregation rule combines companies under common ownership (a controlled group or affiliated service group) into a single employer for the 50-count test, so a founder with three small LLCs that together cross 50 cannot dodge ALE status by staying small on paper. And the seasonal worker exception can pull you back under: if your workforce only exceeds 50 for 120 days or fewer in the year because of seasonal workers, you may not be an ALE despite the raw average. Getting the ALE determination right is the first thing your filing vendor will ask, because it decides whether you file at all.

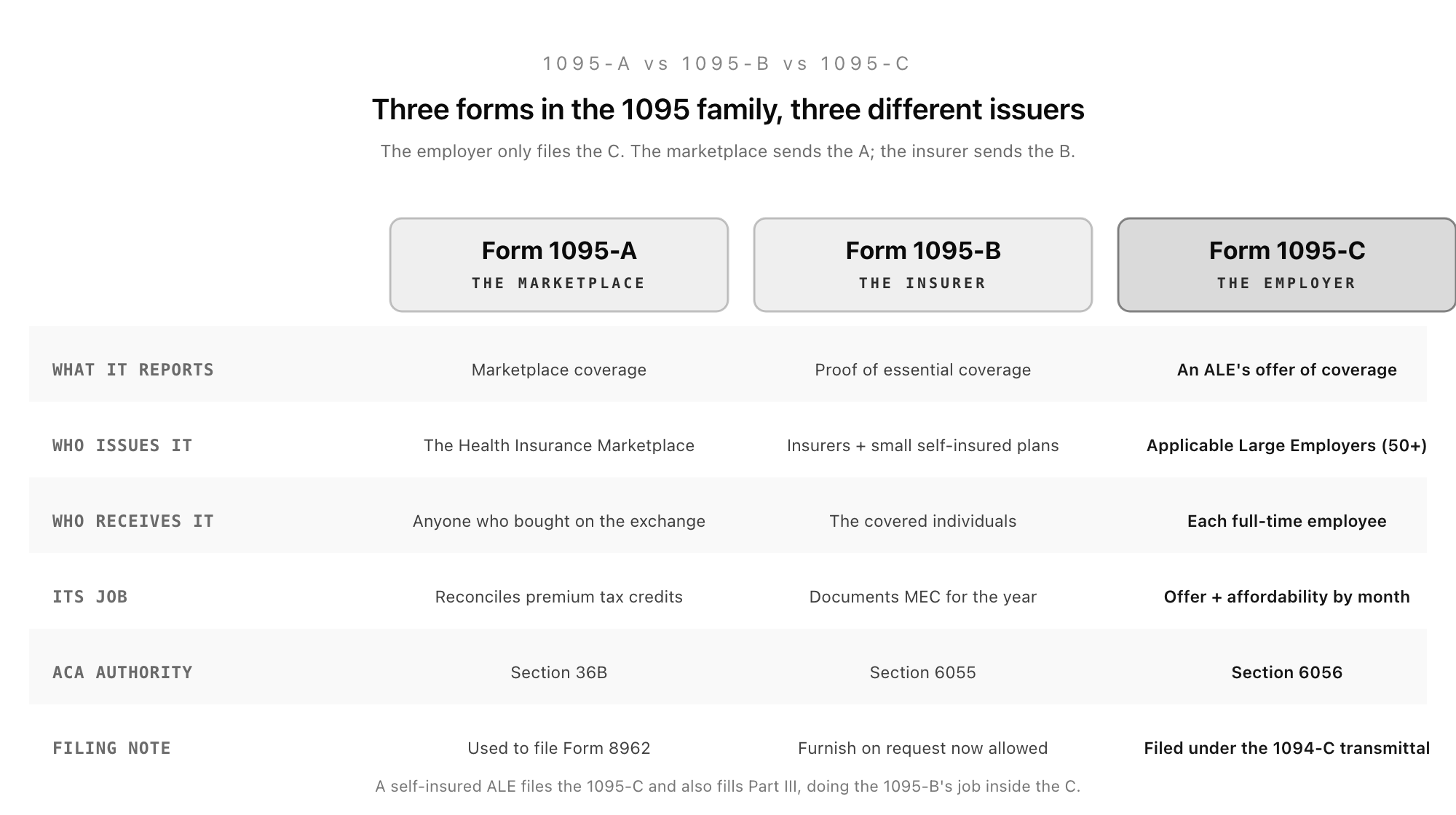

1095-A vs 1095-B vs 1095-C

The "1095" forms confuse people because there are three of them and they look similar. They differ entirely by who issues them.

Form 1095-A is the Marketplace statement. The Health Insurance Marketplace (the exchange) sends it to anyone who bought a plan there. It carries the monthly premium and any advance premium tax credit, and the individual uses it to fill out Form 8962 and reconcile their subsidy. Employers never issue a 1095-A.

Form 1095-B is the minimum-essential-coverage statement. Insurance carriers issue it for fully-insured plans, and small (non-ALE) self-insured employers issue it for their own plans. It simply documents that a person had qualifying coverage for the months listed, under Section 6055.

Form 1095-C is the ALE statement. It does more than the B: it reports the offer of coverage and its affordability, not just whether someone was covered. A self-insured ALE files the 1095-C and uses Part III to also carry the Section 6055 covered-individual data, so it never needs a separate 1095-B.

The Form Structure: Part I, Part II, Part III

The 1095-C has three parts, and only the middle one is complicated.

Part I is identity. Lines 1 through 6 carry the employee's name, Social Security number, and address. Lines 7 through 13 carry the employer's name, EIN, address, and a contact phone number. Nothing here is hard; it just has to match the EIN on the 1094-C transmittal.

Part II is the heart of the form: three lines (14, 15, 16) reported either once in an "All 12 Months" column or separately for each calendar month. If the same offer applied the whole year, you use the All-12-Months column. If anything changed mid-year (a hire, a termination, a waiting period ending, a plan switch), you complete the months individually.

Part III lists covered individuals and their months of coverage. It is completed only if the employer is self-insured. A fully-insured ALE leaves Part III empty because the insurer reports coverage on a 1095-B.

Line 14: The Offer of Coverage Codes

Line 14 answers a single question for each month: what did you offer this employee? The answer is a two-character Series 1 code, from 1A through 1U.

The most-used codes are 1E (minimum-value coverage offered to the employee, spouse, and dependents, the standard "good offer") and 1H (no offer of coverage that month, used for waiting periods, non-full-time months, or months before hire or after termination). 1A is special: the Qualifying Offer, signalling a minimum-value, affordable-to-the-federal-poverty-line offer with family coverage included; using 1A lets you skip Line 15 because affordability is already established. Codes 1B, 1C, and 1D describe narrower offers (employee only, employee plus dependents, employee plus spouse).

In 2020 the IRS added the 1L through 1S codes for Individual Coverage HRAs (ICHRAs), the arrangement where an employer funds an account the employee uses to buy their own Marketplace plan. Those codes encode how ICHRA affordability was measured (by the employee's primary residence or primary work site, and by age). If you offer an ICHRA, Line 14 is where it shows up, and the affordability math on Line 15 follows different rules than a traditional group plan.

Line 15: Employee Required Contribution and the Affordability Test

Line 15 reports a dollar amount: the employee's required contribution for the lowest-cost, self-only, minimum-value plan you offered, for the month. This is not what the employee actually paid for the plan they chose. It is the cheapest self-only option's monthly cost to the employee, even if they enrolled in a richer plan or declined coverage entirely. If your cheapest self-only plan is free to the employee, Line 15 is "0.00".

Line 15 is only completed for certain Line 14 codes (1B, 1C, 1D, 1E, 1J, 1K, and the ICHRA codes), because those are the codes where affordability has to be tested. It exists to support the affordability determination, the rule that an offer only protects you from the larger penalty if the employee's self-only cost stays under an IRS-indexed percentage of income. That percentage is reset every year by revenue procedure (it was 8.39% for 2024 and 9.02% for 2025; confirm the current plan-year figure before filing). Because employers cannot see an employee's household income, the IRS provides three safe harbors that substitute a measurable proxy: the employee's W-2 Box 1 wages, their rate of pay, or the federal poverty line. Whichever safe harbor you use shows up as the Line 16 code.

Line 16: The Section 4980H Safe-Harbor Codes

Line 16 is the relief line. It carries a Series 2 code (2A through 2H) that tells the IRS why no employer shared responsibility payment applies for that month. Where Line 14 says what you offered and Line 15 says what it cost, Line 16 closes the loop on why you are safe.

The common values: 2C means the employee was actually enrolled in the coverage you offered (the cleanest possible answer). 2A means the person was not employed that month. 2B means they were not full-time. 2D covers a "limited non-assessment period," most often a permitted waiting period for a new hire. And the trio 2F, 2G, and 2H each claim one of the affordability safe harbors: 2F for the W-2 safe harbor, 2G for the federal poverty line, 2H for rate of pay. If the offer was affordable under one of those tests, the matching 2-code on Line 16 is what documents it. A blank Line 16 is allowed but is a flag: it means none of the relief codes applied, which is exactly the situation that can trigger a penalty.

Form 1094-C: The Transmittal

Individual 1095-C statements do not travel to the IRS on their own. They are bundled under a Form 1094-C, Transmittal of Employer-Provided Health Insurance Offer and Coverage Information Returns. The 1094-C is to the 1095-C what the W-3 is to the W-2 and what the 1096 is to the 1099: a cover sheet that totals the batch and identifies the filer.

But the 1094-C does more than total. Its Part II carries the "Authoritative Transmittal," where the ALE certifies whether it offered minimum essential coverage to at least 95% of its full-time employees (the threshold that separates the two penalty regimes), claims any transition relief, and answers the aggregated-group questions. Its Part III reports, month by month, the ALE's full-time employee count and total employee count and whether minimum essential coverage was offered. That monthly grid is what the IRS cross-checks against Marketplace subsidy data to decide whether to send a penalty letter. An ALE that is part of an aggregated group files one Authoritative Transmittal per EIN and lists the other group members on Part IV.

The Deadlines and E-Filing Through AIR

ACA reporting runs on the same calendar as the rest of the year-end information returns, with one furnishing wrinkle.

Furnishing to employees: the statutory date is January 31, but the IRS made permanent an automatic 30-day extension, so the practical furnishing deadline lands in early March (March 2 or 3 depending on the year). More importantly, the Paperwork Burden Reduction Act, signed at the end of 2024, now lets an ALE skip mass-mailing the 1095-C entirely: post a clear, conspicuous notice that employees can request their form, and furnish it within 30 days of a request. Many employers will still send them, but the automatic-furnishing requirement is gone.

Filing with the IRS: the 1094-C and 1095-Cs are due to the IRS by February 28 on paper or March 31 if filed electronically. Electronic filing is mandatory once an employer files 10 or more information returns of any type in aggregate (counting W-2s, 1099s, and 1095-Cs together), a threshold that dropped from 250 to 10 for returns due in 2024 and after. In practice that means nearly every ALE e-files, through the IRS AIR (ACA Information Returns) system, generally via payroll or benefits software rather than by hand.

The Employer Reporting Improvement Act, also signed in late 2024, added employer-friendly mechanics worth knowing for a 2026 filing: it codified the furnish-on-request method, permits using a date of birth when a TIN is genuinely unavailable, gives employers at least 90 days to respond to a proposed penalty (Letter 226-J), and sets a 6-year statute of limitations on Section 4980H assessments.

The Penalties the 1095-C Exists to Avoid

There are two distinct penalty exposures, and the 1095-C touches both.

First, the information-return penalties under Sections 6721 and 6722, for filing late, filing with errors, or failing to furnish: these run a few hundred dollars per form for each side (the IRS copy and the employee copy), indexed annually, with a steep annual maximum. Sloppy or missing 1095-Cs cost money on their own, independent of whether your coverage was any good.

Second, and larger, the Section 4980H employer shared responsibility payments, which the whole reporting exercise is built to defend against:

- The 4980H(a) payment (the "sledgehammer") applies if an ALE fails to offer minimum essential coverage to at least 95% of its full-time employees and at least one of them receives a Marketplace premium tax credit. It is assessed across all full-time employees minus the first 30, and runs roughly $2,900 per employee per year for recent years (indexed).

- The 4980H(b) payment (the "tack hammer") applies when coverage was offered but was unaffordable or failed minimum value, and an employee got a subsidy. It is assessed only on the employees who actually received a credit, at a higher per-employee rate (roughly $4,350 for recent years, indexed).

The Line 14, 15, and 16 codes are the evidence. A clean run of 1E on Line 14, an affordable amount on Line 15, and 2C or a 2F/2G/2H safe harbor on Line 16 is what tells the IRS, before any letter goes out, that neither penalty is owed.

How the 1095-C Sits Next to the Federal-Form Pillar

For an HR or finance team, the 1095-C lives in the same January-to-March crunch as the payroll information returns, but on the ACA's legal track rather than the tax code's. The employer files a W-2 for each employee's wages, with a W-3 transmittal; a 1099-NEC for non-employee compensation, with a 1096 transmittal; and the 1095-C for each full-time employee, with a 1094-C transmittal. Each is a statement-plus-transmittal pair, each is due in the same window, and each now e-files under the 10-return aggregate threshold.

What makes the 1095-C different is that it is not reporting money paid. It is reporting an offer: who you offered coverage to, what the cheapest version cost, and why you are protected from the employer mandate. That makes the underlying data harder to assemble, because it lives across payroll (hours and wages), benefits (plan costs and enrollment), and HR (hire and termination dates), and has to be reconciled month by month per person.

A short, structured intake from each manager or location at the start of the reporting cycle (who was full-time which months, what was offered, the lowest-cost self-only premium, enrollment, and any mid-year changes) is what keeps the filing clean and the codes defensible. The Good Form 1095-C intake template captures exactly those per-employee fields in one pass, so your filing vendor has the Line 14, 15, and 16 inputs before the AIR deadline arrives.

The Short Version

Form 1095-C is the Affordable Care Act reporting statement that every Applicable Large Employer files for each full-time employee, plus anyone enrolled in a self-insured plan, under Section 6056. An ALE is an employer that averaged 50 or more full-time employees, including full-time equivalents, over the prior year, with controlled-group aggregation and a seasonal-worker exception both in play. It is one of three 1095 forms: the Marketplace files the 1095-A, insurers and small self-insured plans file the 1095-B, and ALEs file the 1095-C. Part II carries the meaning, read month by month: Line 14 is the offer-of-coverage code (Series 1, 1A to 1U), Line 15 is the employee's required contribution for the lowest-cost self-only minimum-value plan, and Line 16 is the Section 4980H safe-harbor code (Series 2, 2A to 2H) that shows why no penalty applies. Part III lists covered individuals and is completed only by self-insured employers. Affordability, the rule that the self-only cost stays under an IRS-indexed percentage of income, drives Line 15 and the 2F/2G/2H codes via the W-2, rate-of-pay, or federal-poverty-line safe harbors. The statements file under the Form 1094-C transmittal, whose Authoritative Transmittal certifies the 95% offer threshold and reports the monthly full-time count. Furnish to employees by early March (or post a notice and furnish on request under the Paperwork Burden Reduction Act); file with the IRS by February 28 on paper or March 31 electronically, through the AIR system, with e-filing mandatory at 10 aggregate returns. Get the codes right and the 1095-C is what proves you owe neither the Section 6721/6722 information-return penalties nor the Section 4980H employer shared responsibility payments. Teams that want a clean per-employee intake of the offer, cost, and safe-harbor data before the deadline can clone the Good Form 1095-C intake template and start documenting this year's coverage today.