Form SS-4 is the IRS Application for Employer Identification Number, the single form that issues the Employer Identification Number (EIN) every US business uses as its federal tax ID. The EIN is the nine-digit number, written XX-XXXXXXX, that appears on every W-2 an employer issues, every quarterly Form 941 and annual Form 940 it files, every 1099 it sends a contractor, and every W-9 it gives a payer. Before any of those forms can exist, the entity behind them needs an EIN, and the SS-4 is how it gets one. The number is free, it comes directly from the IRS, and for most applicants it is issued in a single online session.

This guide is the line-by-line walkthrough of form SS-4 for a US business in 2026: who actually needs an EIN and who can skip it, the four ways to apply (online for instant issuance, fax in about four business days, mail in about four weeks, and phone for international applicants), the responsible-party rule that has required a natural person since 2018, the one-EIN-per-day online limit, and the IRS rules for when a change to your business forces a brand-new EIN. The audience is founders forming a first company, sole proprietors deciding whether to get an EIN at all, HR and finance leads setting up payroll for a new entity, and anyone who has been handed the job of "go get us a tax ID." If you want a clean intake that captures the legal name, responsible party, entity type, and reason-for-applying an SS-4 needs before you sit down to file it, clone the Good Form SS-4 intake template.

The short version:

- Form SS-4 is the Application for Employer Identification Number. It produces the EIN, the nine-digit federal tax ID (XX-XXXXXXX) that identifies a business to the IRS.

- The EIN is free. The IRS never charges for it. Any site that charges a fee to "get your EIN" is a paid middleman submitting the same free application.

- There are four ways to apply: online (immediate, end-of-session issuance), fax (about four business days), mail (about four weeks), and phone (for international applicants only, +1 267-941-1099).

- Online application requires a principal business in the US or its territories AND a responsible party who has a valid SSN, ITIN, or EIN. Without that, you fax, mail, or (if international) phone.

- The responsible party (line 7a) must be a natural person, an actual individual who owns or controls the entity, not another company. This has been the rule since 2018. Government entities are the narrow exception.

- The IRS limits issuance to one EIN per responsible party per day. You cannot batch-create EINs for multiple entities in a single session.

- Not every business needs an EIN. Sole proprietors with no employees can use their SSN. But you need an EIN the moment you hire employees, form an LLC, corporation, or partnership, set up a solo 401(k) or Keogh, file excise tax, or want to keep your SSN off the W-9s you hand clients.

- A change to your business sometimes forces a new EIN and sometimes does not. Incorporating a sole proprietorship needs a new EIN; renaming or relocating the same entity does not. The rules differ by entity type.

- Apply only after the entity legally exists. A corporation or LLC should be formed with the state before the SS-4 names it, so the legal name on line 1 matches the state registration exactly.

What Form SS-4 Is and Why It Exists

Form SS-4, formally the Application for Employer Identification Number, is the IRS form a business completes to be assigned an EIN. The EIN is to a business what a Social Security number is to a person: a permanent federal identifier the IRS uses to track the entity across every return and payment it ever makes. Once issued, the EIN belongs to that entity for the life of the entity. It is not reissued, recycled, or transferred to a different business.

The number exists because the IRS needs a single key that ties together everything an employer or business files. The same EIN appears on the employment-tax returns (Form 941 quarterly and Form 940 annually), the wage statements (W-2) sent to the Social Security Administration, the information returns (1099) sent to contractors, the entity's own income-tax return, and the W-9 it provides when a client needs its tax ID. A mismatch between the EIN on any one of those and the IRS's registration record produces a notice, so getting the SS-4 right at the source matters for every form downstream.

The IRS issues the EIN at no cost. This is worth stating plainly because a large industry of paid filing sites positions itself between applicants and the free IRS application, charging fifty to three hundred dollars to submit the same SS-4 you can submit yourself in about fifteen minutes. The official application lives at IRS.gov, the EIN it produces is identical, and the IRS does not endorse or partner with any paid EIN-filing service.

Do You Even Need an EIN?

Not every business is required to have one. A sole proprietor with no employees can legally use their own Social Security number as the business tax ID on every federal filing. Whether to get an EIN anyway is a judgment call, and for most people the answer is yes.

You are required to have an EIN if any of the following is true: you have employees (the EIN is mandatory before the first payroll run); your business is a corporation or a partnership; your business is a multi-member LLC; you file employment, excise, or alcohol-tobacco-and-firearms tax returns; you have a Keogh plan or a solo 401(k); you withhold taxes on income (other than wages) paid to a non-resident alien; or you administer certain trusts, estates, or non-profit organizations.

You are not required to have one as a single-member LLC with no employees (which is a disregarded entity using the owner's SSN by default) or as a sole proprietor with no employees. But getting an EIN even when it is optional is usually the right move, for four practical reasons. It lets you open a business bank account, which most banks will not do on an SSN alone. It keeps your Social Security number off every W-9 you hand a client, replacing it with an EIN that exposes far less. It is a prerequisite the day you hire your first employee or contractor, so getting it early avoids a scramble. And it signals to lenders, processors, and partners that the business is a real, separately identified entity.

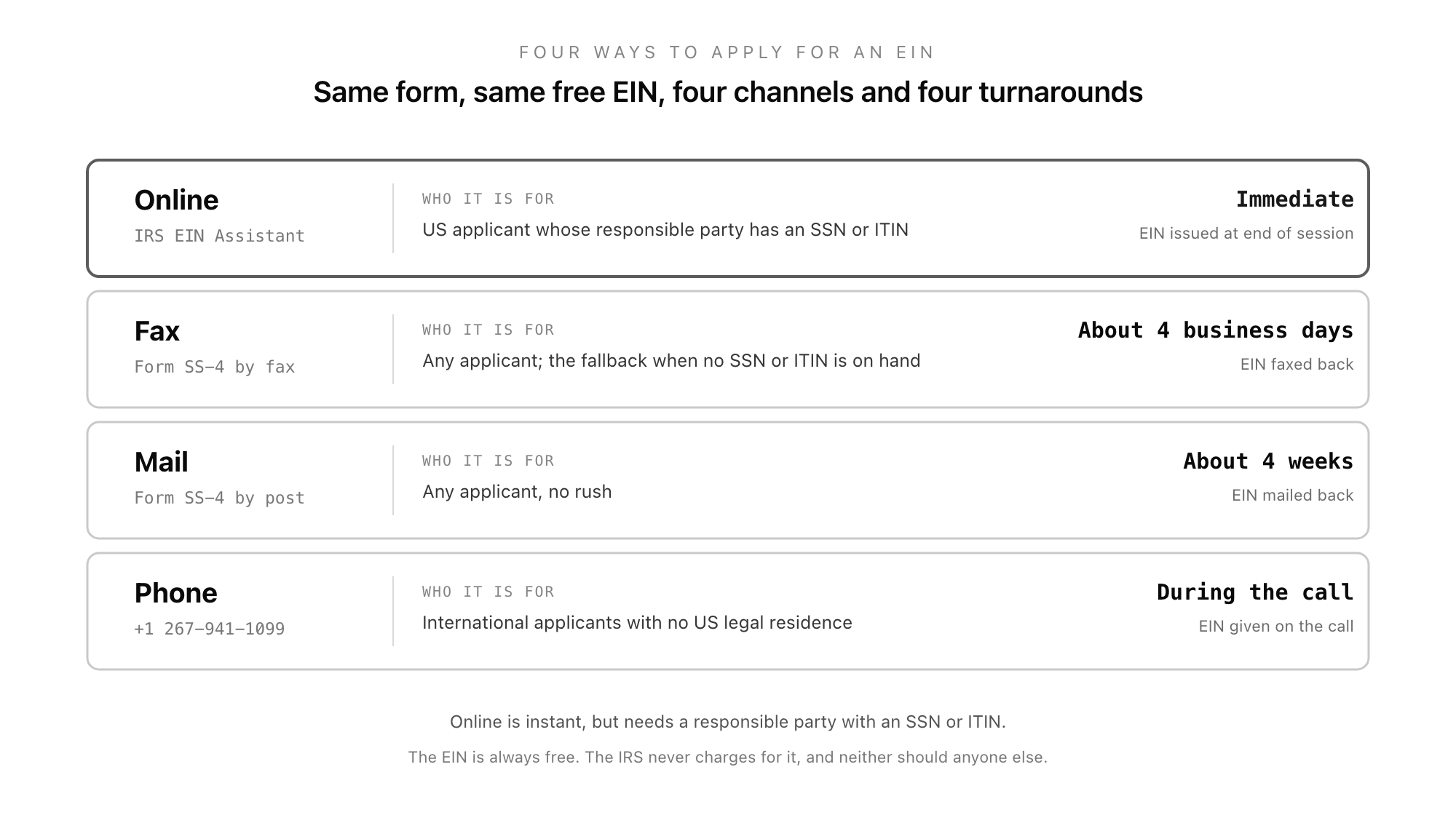

The Four Ways to Apply for an EIN

There are four channels for submitting an SS-4, and they differ enormously in speed.

Online is the default and the fastest. The IRS EIN Assistant walks through the SS-4 questions as an interview and issues the EIN at the end of the session, immediately, in a downloadable confirmation letter (the CP 575 equivalent). Online application has two hard requirements: the principal business must be located in the United States or a US territory, and the responsible party must have a valid SSN, ITIN, or EIN. The assistant is available during posted hours (roughly 7am to 10pm Eastern, Monday to Friday) and a single session must be completed in one sitting, with a fifteen-minute inactivity timeout.

Fax is the fallback for applicants who cannot use the online tool, typically because the responsible party does not have a US taxpayer ID to hand. You fax the completed SS-4 to the IRS, and if you include a return fax number, the EIN is faxed back in about four business days.

Mail is the slowest channel: a completed paper SS-4 posted to the IRS, with the EIN mailed back in about four weeks. It works for any applicant but is rarely the right choice when fax or online is available.

Phone is reserved for international applicants, meaning entities with no legal residence, principal office, or agency in the United States. They call the IRS international EIN line at +1 267-941-1099 (not toll-free), answer the SS-4 questions on the call, and receive the EIN during the call. The person calling must be authorized to receive the EIN and answer questions about the form.

The one rule that catches people regardless of channel is the one-EIN-per-responsible-party-per-day limit. The IRS will issue only one EIN per day to the same responsible party, online or otherwise. An accountant or founder setting up several entities at once has to spread the applications across multiple days.

The Form SS-4 Line-by-Line Walkthrough

The SS-4 is one page. Most lines are short, and the answers come from documents you already have (the formation paperwork, the responsible party's tax ID, the business address).

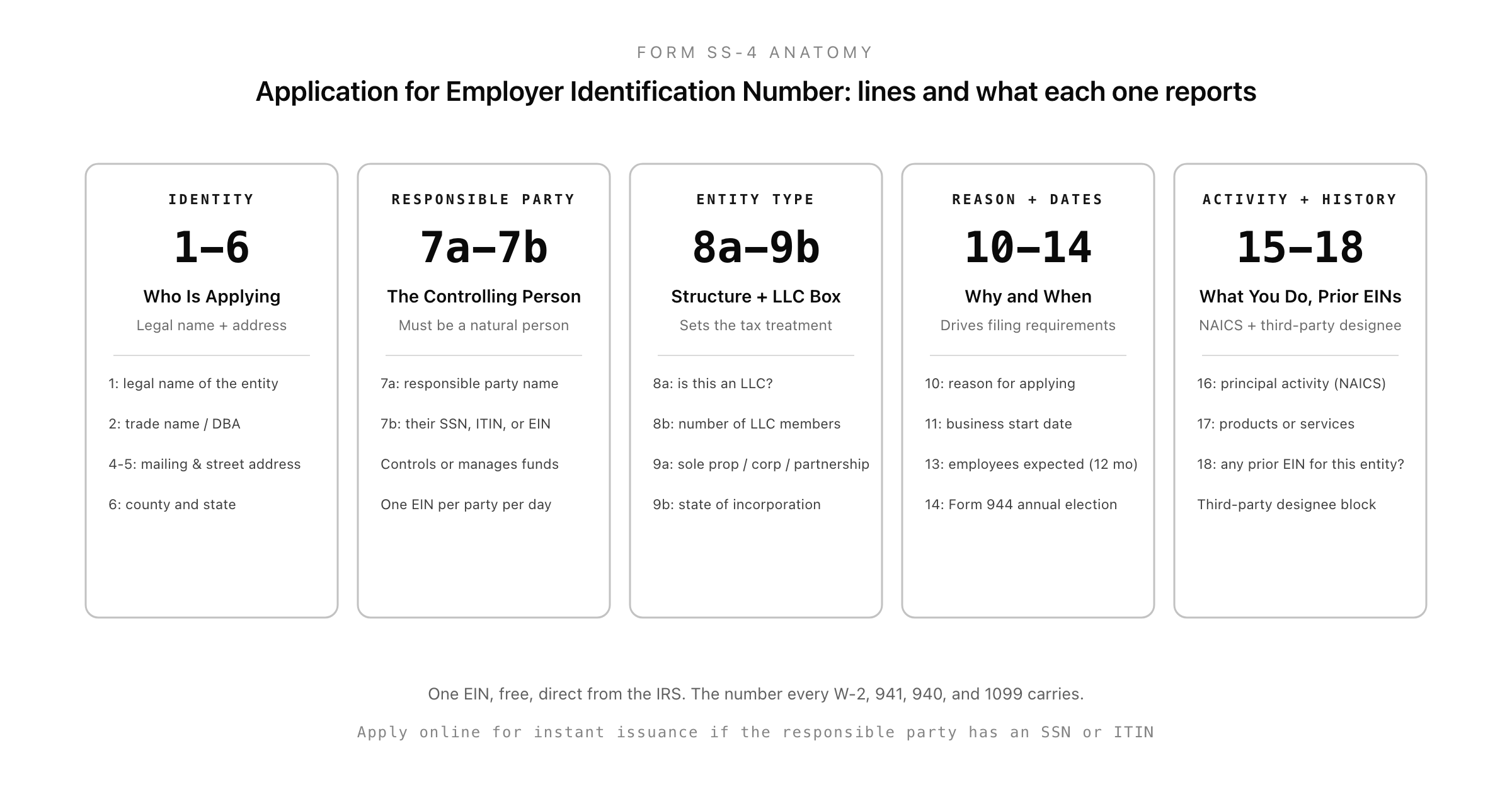

Lines 1 to 6: who is applying

Line 1 is the legal name of the entity (or individual) for whom the EIN is being requested. For a corporation or LLC, this must match the name registered with the state, exactly, including punctuation and the entity designator (Inc., LLC, Corp.). For a sole proprietor, it is the individual's own legal name. Line 2 is the trade name (the DBA, "doing business as") if it differs from line 1. Line 3 is a "care of" name, used mainly for estates and trusts to name the executor, administrator, or trustee. Lines 4a and 4b are the mailing address; lines 5a and 5b are the physical street address if it differs from the mailing address. Line 6 is the county and state where the principal business is located.

Lines 7a and 7b: the responsible party

Line 7a is the name of the responsible party, and line 7b is that person's SSN, ITIN, or EIN. This is the most consequential pair of lines on the form, and it has its own section below, because the rules about who can be named here changed in 2018.

Lines 8a to 9b: the entity type

Line 8a asks whether the application is for a limited liability company; line 8b asks the number of LLC members; line 8c asks whether the LLC was organized in the United States. Line 9a is the entity type itself, a set of checkboxes: sole proprietor (with a space for the proprietor's SSN), partnership, corporation (with the income-tax form number it will file, such as 1120 or 1120-S), personal service corporation, church or church-controlled organization, other non-profit, estate, trust, and several others. Line 9b is the state or foreign country where a corporation is incorporated.

A single-member LLC is the line most likely to confuse. An LLC ticks line 8a "yes," but on line 9a it generally selects the tax classification it has elected or defaulted into: a single-member LLC with no election is a disregarded entity and usually files as a sole proprietor, while a multi-member LLC defaults to partnership.

Lines 10 to 14: reason, dates, and the Form 944 option

Line 10 is the reason for applying, by checkbox: started a new business, hired employees, banking purposes, changed type of organization, purchased a going business, created a trust, created a pension plan, or compliance with IRS withholding regulations. Line 11 is the date the business started or was acquired. Line 12 is the closing month of the accounting year (December for most). Line 13 is the highest number of employees expected in the next 12 months, split into agricultural, household, and other.

Line 14 is the Form 944 annual-filing election. If you expect your total annual employment-tax liability to be $1,000 or less (which corresponds to paying $5,000 or less in wages for the year), you can check this box to file the annual Form 944 instead of the quarterly Form 941. The IRS confirms eligibility; checking the box is a request, not a guarantee.

Lines 15 to 18: activity, history, and the designee

Line 15 is the first date wages or annuities were paid (or will be paid). Line 16 is the principal business activity, a set of broad checkboxes (construction, real estate, manufacturing, retail, health care, accommodation and food service, finance and insurance, and so on) that the IRS uses to classify the entity. Line 17 is the specific line of products sold or services provided. Line 18 asks whether the applicant entity has ever applied for and received an EIN before, which catches duplicate applications. Below the numbered lines, the Third Party Designee section lets you authorize a named person (an accountant, for example) to receive the EIN and answer questions about the form, and the signature block closes it out.

The Responsible Party Rule

Lines 7a and 7b deserve their own treatment because the rule changed in a way that still trips applicants. Since 2018, the IRS has required that the responsible party named on line 7a be a natural person, an actual human being, not another entity. The only exceptions are government entities and a small number of specifically permitted cases.

The responsible party is defined as the individual who ultimately owns or controls the entity, or who exercises ultimate effective control over it, including control of the funds and assets. For a single-owner business, that is the owner. For a corporation, it is typically a principal officer. For a partnership, a general partner. For a trust, the grantor, owner, or trustor. The point of the rule is to put a real, identifiable person behind every EIN, so that the IRS is not chasing a chain of shell entities that name each other as responsible parties.

This is why an online application requires the responsible party to have an SSN, ITIN, or EIN: the IRS validates the responsible party's identity against an existing tax record in real time. An entity whose only available responsible party lacks a US taxpayer ID (common for foreign-owned businesses) cannot use the online tool and must apply by fax, mail, or the international phone line, where the validation is handled differently.

If the responsible party changes after the EIN is issued (a business is sold, a controlling officer leaves), the IRS expects an update via Form 8822-B within 60 days. The EIN itself does not change; only the responsible-party record behind it is updated.

When You Need a New EIN (and When You Don't)

A common and expensive misunderstanding is that any change to a business requires a new EIN. It does not. The EIN stays with the entity through most changes; only certain structural changes require a fresh one, and the rules differ by entity type.

For a sole proprietorship, you need a new EIN if you incorporate, if you take in partners and become a partnership, or if you are subject to a bankruptcy proceeding. You do not need a new EIN if you simply change the business name, change the location, or operate multiple businesses as the same sole proprietor.

For a corporation, you need a new EIN if you receive a new charter from the state (a genuine new entity), if you become a subsidiary of a corporation using the parent's EIN, if you change to a partnership or a sole proprietorship, or if a statutory merger creates a new corporation. You do not need a new EIN for an S-corporation election, a name change, a location change, or a reorganization that changes only identity or place.

For a partnership, you need a new EIN if you incorporate, if one partner takes over and runs it as a sole proprietorship, or if you end the partnership and form a genuinely new one. You do not need one for a name change or a location change.

The thread running through all of these is that a new EIN follows a new legal entity, not a cosmetic change to an existing one. Renaming, relocating, or restyling the same legal entity keeps the EIN. Dissolving one entity and creating another, or fundamentally changing the entity's legal type, gets a new one.

Common SS-4 Errors and How to Avoid Them

Three mistakes account for most of the friction applicants hit.

The first is paying a third-party site for a free service. Search results for "apply for EIN" are dominated by paid filing services that charge a fee to submit the SS-4 on your behalf. The application is free at IRS.gov, the EIN is identical, and the only thing the fee buys is a form-filling intermediary. The exception is genuinely wanting an accountant or formation service to handle the whole entity setup as a package; that is a legitimate service, but it is not the same as the EIN costing money.

The second is naming an entity as the responsible party. Since the 2018 rule, line 7a must be a natural person. An application that lists a holding company or another LLC as the responsible party will be rejected. Name the actual human who controls the entity, with their SSN, ITIN, or EIN on line 7b.

The third is applying before the entity legally exists, or with a name that does not match the state registration. A corporation or LLC should be formed with the state first, so the legal name on line 1 exactly matches the articles of incorporation or organization. Applying for the EIN before the entity is formed, or with a slightly different name (a missing "LLC," a different punctuation), creates a permanent mismatch between the EIN record and the state record that surfaces later when a bank, a payment processor, or the IRS cross-checks them. A close cousin of this error is requesting more than one EIN in a day for the same responsible party and being blocked by the one-per-day limit.

How Good Form Fits Around the SS-4

The SS-4 itself is an IRS application you submit directly to the IRS, online or on paper. A form builder does not file it for you, and you should be wary of anything that offers to. Where Good Form fits is upstream: collecting and confirming the facts the SS-4 depends on before you sit down to apply, so the application is fifteen minutes of data entry instead of an hour of hunting for the responsible party's SSN and the exact state-registered legal name.

Good Form is a form builder used by HR and small finance teams to run the intake side of business and employment paperwork: new-hire packets, the federal forms that follow a hire, and pre-filing capture for the returns that all carry the EIN, like the W-2, the 1099, the Form 941, and the Form 940. For the SS-4, Good Form sits at the very start of that chain, capturing the legal name, responsible party, entity type, and reason-for-applying that the EIN application needs, and that every later form will reference back to.

The Companion Template

The Good Form SS-4 intake template (clone it here) is a pre-application capture for the data Form SS-4 asks for. It collects the legal name exactly as it should appear on line 1 (with a reminder to match the state registration), the trade name for line 2, the mailing and street address for lines 4 and 5, the responsible party's name and SSN, ITIN, or EIN for lines 7a and 7b (with the natural-person reminder built in), the entity type and LLC details for lines 8 and 9, the reason for applying and key dates for lines 10 to 13, the Form 944 election question for line 14, and the principal-activity classification for lines 16 and 17. It also asks which application method you intend to use, so the responsible-party-needs-an-SSN-or-ITIN requirement for online filing is surfaced before you discover it mid-session.

It does not file the SS-4, and it does not produce an EIN. Only the IRS does that, for free. What the template does is make the application a verification step rather than a research project: gather the answers cleanly, confirm the responsible party qualifies, check the legal name against the state record, and then go to IRS.gov and enter them. Run it the day the entity is formed, and the EIN follows in a single session.

Form SS-4 is the first form in the life of a business that has employees or files federal returns. It is short, it is free, and it produces the one number that ties every later filing together. Get the legal name, the responsible party, and the entity type right at the source, apply directly through the IRS, and the EIN it issues will carry cleanly through every W-2, 941, 940, and 1099 the business ever files.