Form 941 is the federal Employer's Quarterly Federal Tax Return that almost every US employer files four times a year to report the federal income tax, Social Security, and Medicare taxes withheld from employee paychecks during the quarter, alongside the employer's matching share. Where the W-4 form is the per-employee input that decides how much to withhold and the W-2 form is the per-employee output filed once a year, the form 941 is the per-employer reconciliation that runs underneath every payroll cycle in between. It is the quarterly accounting the IRS uses to track that the trust-fund taxes you withheld from your employees actually arrive in Treasury's bank account.

This guide is the line-by-line walkthrough of form 941 for a US employer in 2026: what each numbered line reports, the lookback rule that decides whether you deposit monthly or semiweekly, when Schedule B is required, the four 2026 quarterly due dates, the 941-X amendment path, the FUTA Form 940 sibling that lives alongside it, and the Trust Fund Recovery Penalty under IRC Section 6672 that pierces the corporate veil and assesses unpaid trust-fund taxes personally against responsible owners and officers. The audience is HR teams of one to ten, office managers running payroll without a CPA on retainer, and finance leads picking up payroll responsibility from a previous owner. If you want a clean intake that captures the EIN, legal-entity, and depositor-status data every 941 quarter depends on before you file your first return, clone the Good Form 941 quarterly intake template.

The short version:

- Form 941 is the Employer's Quarterly Federal Tax Return. It reports, for one employer for one quarter, the federal income tax withheld plus the employee and employer shares of Social Security and Medicare.

- It is filed four times a year. Q1 (Jan to Mar) is due April 30. Q2 (Apr to Jun) is due July 31. Q3 (Jul to Sep) is due October 31. Q4 (Oct to Dec) is due January 31. If every deposit for the quarter was made on time, you get an extra 10 days to file.

- The form is in five parts. Part 1 (lines 1 to 15) is the wage and tax reconciliation. Part 2 (line 16) is the deposit-schedule attestation. Part 3 covers business closure and seasonal status. Part 4 names a third-party designee. Part 5 is the signature.

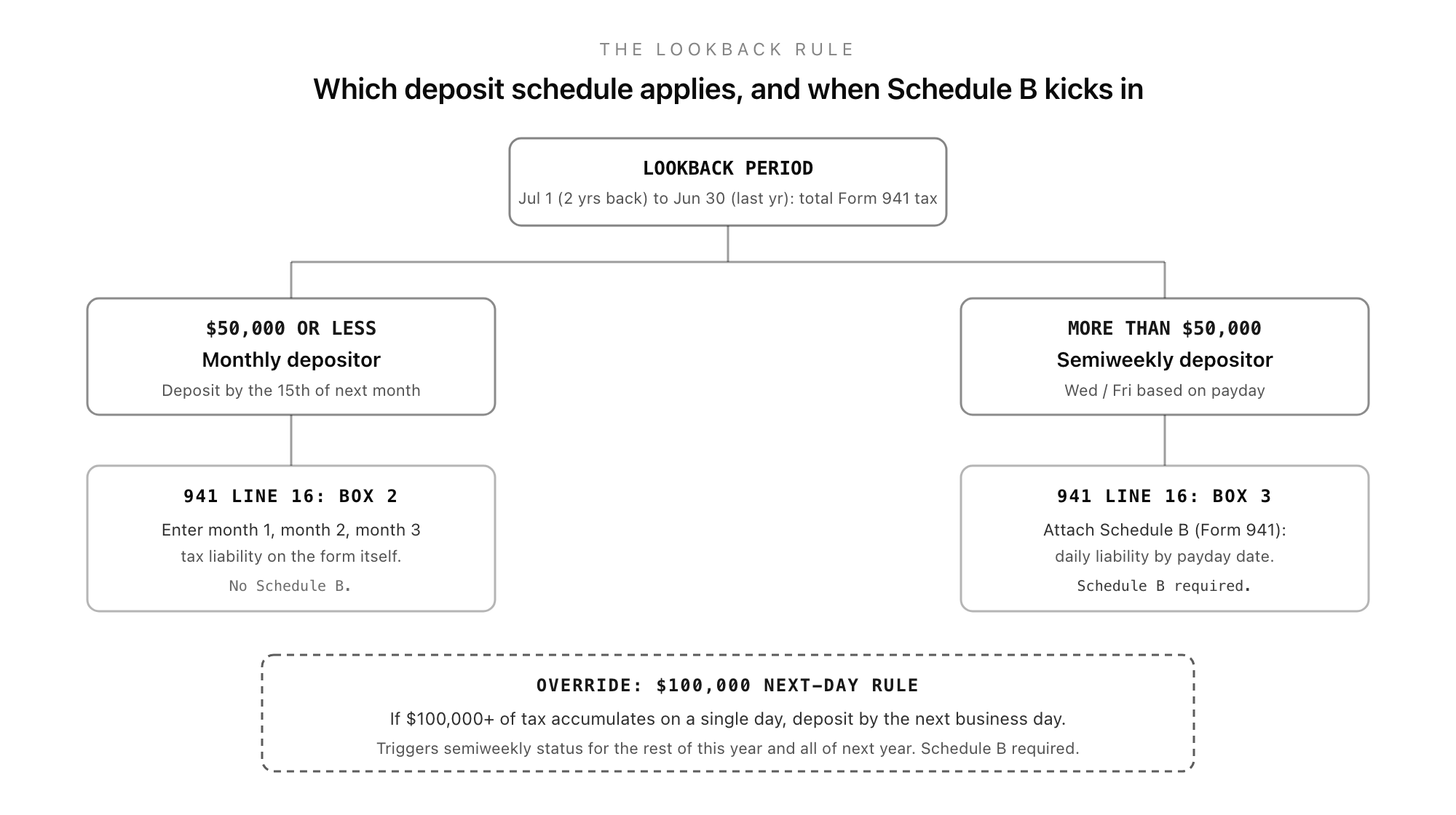

- The lookback rule decides your deposit schedule. If your total Form 941 tax in the four-quarter lookback period (July 1 two years back through June 30 last year) was $50,000 or less, you deposit monthly. Over $50,000 makes you a semiweekly depositor.

- Semiweekly depositors must attach Schedule B (Form 941) reporting daily tax liability. Monthly depositors enter three monthly totals on line 16 itself and do not attach Schedule B.

- The $100,000 next-day rule overrides everything. Any single day your accumulated unpaid trust-fund tax hits $100,000, you must deposit by the next business day, and you become a semiweekly depositor for the rest of the year and all of next year.

- To correct a filed 941, file a Form 941-X. There are two paths: an adjusted return (the correction is applied on a future 941) or a refund/abatement claim (the IRS sends a refund). 941-X cannot be e-filed; it is paper-only and must be filed within three years of the original 941 or two years from when the tax was paid, whichever is later.

- Form 940 is the annual FUTA sibling. 6.0% of the first $7,000 of wages per employee, dropped to an effective 0.6% by the state-UI credit, deposited quarterly when liability crosses $500, and reported on one annual return due January 31.

- The Trust Fund Recovery Penalty under IRC Section 6672 personally assesses 100% of unpaid trust-fund taxes against responsible persons who willfully fail to pay. Owners, officers, bookkeepers, and check-signers who divert payroll taxes to pay vendors instead are individually liable. The corporate veil does not protect them.

What Form 941 Is and Why It Exists

Form 941, formally the Employer's Quarterly Federal Tax Return, is the quarterly report every US employer with employees files to reconcile three federal taxes: the federal income tax withheld from employees' wages under the W-4 they filed at hire, the employee and employer shares of Social Security tax, and the employee and employer shares of Medicare tax including the 0.9% Additional Medicare surcharge on wages above the $200,000 threshold. The form tells the IRS, for the quarter just ended, how much wage tax the employer accumulated, how much it deposited along the way, and whether the deposits and the obligation reconcile.

Form 941 exists because the federal payroll-tax system is pay-as-you-go on two clocks. The deposit clock is continuous: employers must deposit the taxes shortly after each payroll, on either a monthly or semiweekly schedule depending on size. The reporting clock is quarterly: the 941 is the formal return that reconciles those deposits against the actual quarterly liability and either books a balance due or claims an overpayment. The deposit and the return are deliberately separated, because the IRS wants the money continuously and the paperwork periodically.

The form is filed with the IRS, not the SSA. The SSA receives annual W-2 data once a year; the IRS receives 941 data four times a year. The two systems crosswalk: the totals across the four quarters of 941s should reconcile to the totals on the W-3 transmittal of the W-2s for the same year, and the IRS runs that crosswalk automatically. A mismatch triggers a CP2000 notice asking the employer to explain.

The Four 2026 Due Dates

Form 941 has a strict quarterly cadence. The return for each quarter is due on the last day of the month following the quarter end:

- Q1 2026 (January 1 to March 31): due April 30, 2026 (Thursday)

- Q2 2026 (April 1 to June 30): due July 31, 2026 (Friday)

- Q3 2026 (July 1 to September 30): due November 2, 2026 (October 31 is a Saturday, so the next business day)

- Q4 2026 (October 1 to December 31): due February 1, 2027 (January 31, 2027 is a Sunday, so the next business day)

Note: the Q4 2025 return that lands inside 2026's calendar was due February 2, 2026 for the same Saturday-shift reason. The IRS uses the next-business-day rule whenever a return deadline lands on a weekend or federal holiday.

There is one filing extension built into the rule. If the employer made every deposit on time and in full for the entire quarter, the return is not due until the tenth day of the second month after the quarter ends. So a perfectly on-time depositor effectively has until May 10, August 10, November 10, and February 10. The extension applies only to the return; it does not extend any deposit deadline.

Where you mail a paper 941 depends on your state and on whether you are paying with the return. The IRS publishes the addresses in the form instructions, and they change occasionally. E-filing through the IRS MeF system avoids the address question entirely and is now the default path for most employers. Note that the federal information-return e-file mandate that applies to W-2s and 1099s at 10 returns aggregate does not technically apply to 941, which has its own thresholds, but most payroll software files 941 electronically by default.

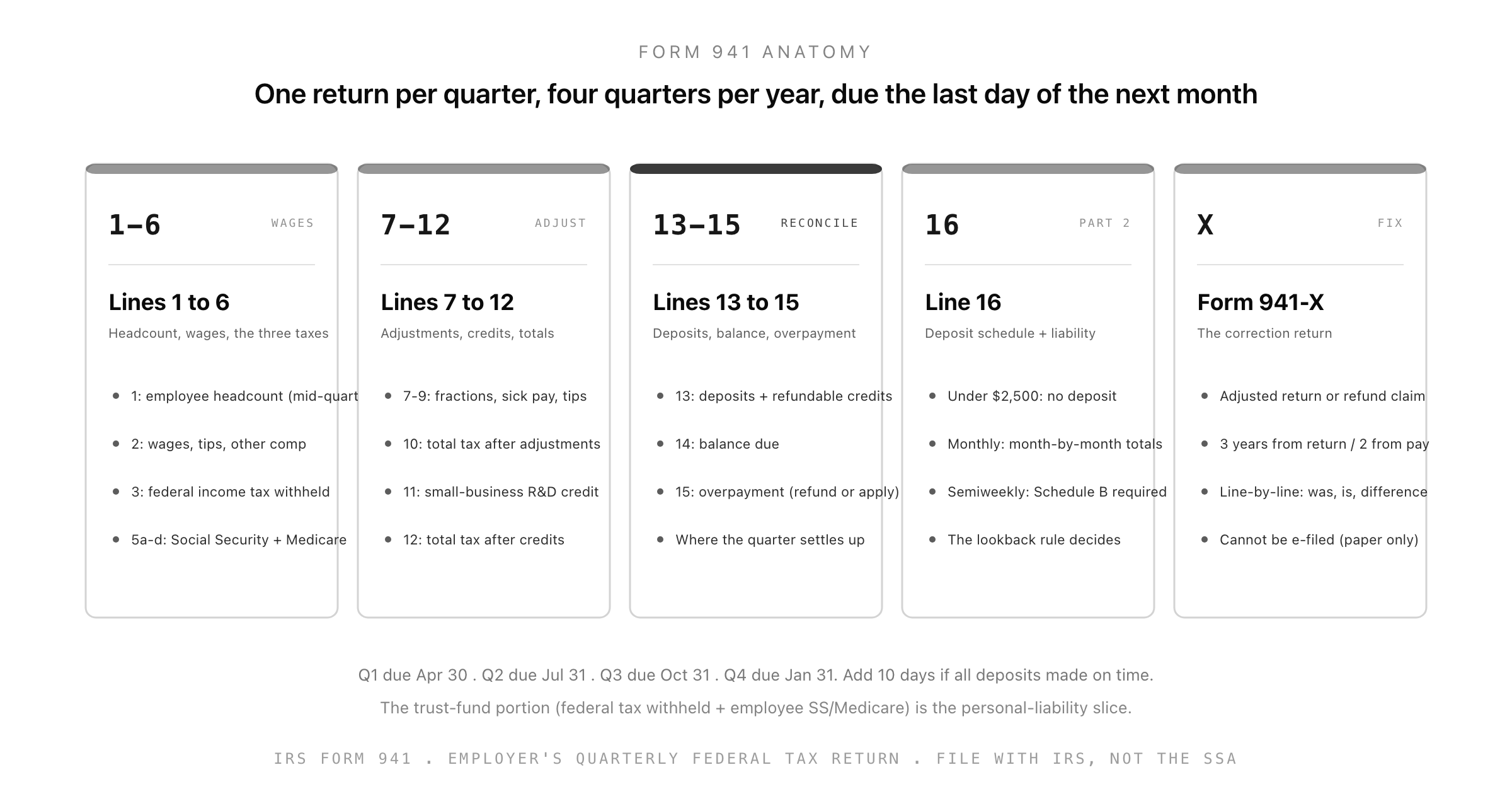

The Form 941 Line-by-Line Walkthrough

Part 1: Lines 1 to 6, the wage and tax base

Line 1 is the number of employees who received wages, tips, or other compensation for the pay period that includes a specific mid-quarter date: March 12 for Q1, June 12 for Q2, September 12 for Q3, and December 12 for Q4. It is a snapshot, not a quarterly average, which means a company that hires a hundred people on March 14 reports zero on Q1 line 1 even though it ran a March payroll.

Line 2 is total wages, tips, and other compensation paid in the quarter. Line 3 is the federal income tax withheld against those wages, driven by each employee's W-4. Line 4 is a checkbox for the rare case where wages are not subject to Social Security or Medicare withholding at all.

Lines 5a through 5d are where Social Security and Medicare get reported. Line 5a is taxable Social Security wages times 12.4% (the combined employee and employer rate). Line 5b is the same calculation on taxable Social Security tips. Line 5c is taxable Medicare wages and tips times 2.9% (combined). Line 5d is the Additional Medicare 0.9% on wages above the $200,000 employee threshold, employee share only (the employer does not match the Additional Medicare). Line 5e sums them. Line 5f handles a rare correction for an unreported-tip notice from the IRS.

Line 6 is the total of line 3 plus line 5e plus line 5f. This is the quarter's gross tax before any adjustments or credits.

Part 1: Lines 7 to 12, adjustments and credits

Lines 7 through 9 are the adjustment block. Line 7 is the rounding adjustment that reconciles fractions of cents on Social Security and Medicare across payroll runs (always small, but always there). Line 8 adjusts for sick pay paid by a third party where the third party did not withhold and remit. Line 9 adjusts for group-term life insurance above $50,000 for former employees, where the employer cannot withhold from a paycheck because there is no paycheck.

Line 10 is the total tax after adjustments: line 6 plus or minus the adjustment lines.

Line 11 is the qualified small-business payroll tax credit for increasing research activities, computed on Form 8974 and brought across. It is a narrow credit, but eligible early-stage companies should not leave it on the table because it directly offsets the employer Social Security tax on line 5a.

Line 12 is the total tax after credits: line 10 minus line 11. This is the bottom of the calculation; everything below reconciles deposits against this number.

Part 1: Lines 13 to 15, the quarterly settle-up

Line 13a is the total deposits made for the quarter, including any prior-quarter overpayment applied to this quarter on a previous 941. Line 13b through 13g are now mostly inactive (they previously captured COVID-era credits and refunds). Line 13g (or whatever the current consolidated total line is in the current revision) totals deposits plus any current refundable credits.

Line 14 is balance due. If line 12 (total tax after credits) is more than line 13 (deposits plus credits), the difference is owed with the return.

Line 15 is overpayment. If line 13 exceeds line 12, the employer can check a box to either get the overpayment refunded or apply it as a credit to the next quarter's 941.

The reconciliation is the entire purpose of the form. The deposits arrived continuously throughout the quarter; the 941 is where you prove what they were supposed to add up to.

Part 2: Line 16, the deposit-schedule attestation

Part 2 is one line, and it does more work than its size suggests. Line 16 has three checkboxes. The employer ticks exactly one:

- Box 1: line 12 is less than $2,500 for the quarter, or line 12 on the prior quarter was less than $2,500. In this case no deposits are required and the tax can be paid with the return. This is the small-employer escape hatch.

- Box 2: monthly schedule depositor. Below the box, the employer fills in three subtotals: tax liability in month 1, month 2, and month 3 of the quarter, summing to line 12. The IRS uses these to check that the deposits arrived in the right months.

- Box 3: semiweekly schedule depositor or the $100,000 next-day rule applied. The employer attaches Schedule B (Form 941), which reports daily tax liability by payday across every business day of the quarter.

Which box applies is not the employer's choice. It is determined by the lookback rule.

The Lookback Rule: Monthly vs Semiweekly

Every employer falls into one of two deposit schedules, and the schedule is set once a year by looking backward, not forward.

The lookback period is the four quarters from July 1 two years prior to June 30 of the prior year. For deposits in 2026, the lookback period is July 1, 2024 through June 30, 2025. The employer adds up the total taxes reported on lines 12 of those four 941s.

- $50,000 or less in the lookback period: the employer is a monthly schedule depositor for the entire current year. The trust-fund taxes for each month must be deposited by the 15th day of the following month. So January's payroll taxes are deposited by February 15. There is no Schedule B; the three monthly totals go directly on line 16 of the quarterly 941.

- More than $50,000 in the lookback period: the employer is a semiweekly schedule depositor for the entire current year. The deposit deadline depends on the payday. Wednesday, Thursday, or Friday payrolls are deposited by the following Wednesday. Saturday, Sunday, Monday, or Tuesday payrolls are deposited by the following Friday. Schedule B is attached to every 941, reporting the daily tax liability for each business day of the quarter.

New employers (those with no lookback history) are monthly depositors by default.

The $100,000 next-day rule overrides both schedules. If the employer accumulates $100,000 or more of unpaid trust-fund tax on any single day, that day's tax must be deposited by the next business day. Hitting the $100,000 trigger also flips the employer to semiweekly status for the remainder of the current year and all of the following year. A one-day spike (a stock-vesting day, a year-end bonus run, a sale-of-business closing payment) can move a small employer onto the semiweekly schedule for 18+ months.

The lookback rule is annoying because it sets schedules based on backward-looking data, which means a fast-growing employer can spend a year as a monthly depositor while genuinely operating at semiweekly volume. The remedy is to plan ahead: if your prior year crossed $50,000, you know now that next year is semiweekly, and your payroll system should be configured before January.

Form 941-X: The Correction Return

If you discover an error on a filed 941 (a wage misstatement, an over-withholding, an under-withholding, a missed credit, a duplicated deposit), you do not file a corrected plain 941. You file Form 941-X, the Adjusted Employer's Quarterly Federal Tax Return or Claim for Refund.

941-X works on a quarter-by-quarter basis: one 941-X per affected original 941. The form asks, line by line, for the originally reported figure, the corrected figure, and the difference. The employer then chooses one of two paths in Part 1:

- Adjusted employment tax return. The correction is rolled into a future 941 as a current-period adjustment. This is the path when you underreported tax (you owe more) or when you overreported and want the credit applied to a future return rather than refunded.

- Claim for refund or abatement. The IRS issues a refund of the overpayment or abates a penalty. This is the path when you overpaid and want the money back rather than carried forward.

Three procedural notes that catch employers out. First, 941-X cannot be e-filed. It is paper-only, even for employers who e-file their original 941s. Second, the filing window is three years from the date the original 941 was filed, or two years from when the tax was paid, whichever is later. Outside that window, the IRS will reject the correction. Third, an interest-free adjustment is available only if the underpayment is corrected by the due date of the 941 for the quarter in which the error was discovered, otherwise interest accrues from the original due date.

The 941-X is also the form that processed retroactive credit claims (notably the Employee Retention Credit during and after the pandemic). The credit-claim path is the same form with different boxes.

Form 940: The Annual FUTA Sibling

Form 941 sits inside a tight family of employer payroll-tax returns. The most important sibling is Form 940, the Employer's Annual Federal Unemployment (FUTA) Tax Return.

FUTA is the federal unemployment tax. It is 6.0% on the first $7,000 of wages paid to each employee during the year, which means the FUTA wage base resets at $7,000 per employee per year, not per quarter. Because most employers also pay state unemployment tax (SUTA) and the state systems are credited against the federal tax, the effective FUTA rate drops to 0.6% for employers in good standing in non-credit-reduction states. A few credit-reduction states (states that have borrowed from the federal unemployment fund and not repaid on schedule) raise the effective rate by 0.3% per year of borrowing, which the IRS publishes in November for the year just ending.

Form 940 differs from form 941 in three structural ways. It is annual, not quarterly: one 940 per year, due January 31. It is employer-only: there is no employee share, no withholding, and the employee never sees it. And it has a deposit threshold of $500 per quarter, not a continuous deposit schedule. If quarterly FUTA liability stays under $500, no quarterly deposit is required and the entire balance can be paid with the annual 940. If quarterly liability crosses $500, the employer deposits by the end of the next month and tracks the rolling balance.

The practical pattern most small employers hit: a company with eight to fifteen low-paid employees keeps quarterly FUTA under $500 all year and pays once with the January 940. A company that grows past about twenty employees, or pays higher wages, starts triggering quarterly FUTA deposits. The 940 itself is a one-page form with about a dozen lines, conceptually simpler than the 941 because there are no withholdings to reconcile.

940 and 941 are filed separately, on different cadences, with different deposit mechanics, but they describe the same wage base. The headcount line on the 941 and the wage figures on the 940 must be internally consistent across the year.

The Trust Fund Recovery Penalty: The Personal-Liability Stick

This is the part of payroll-tax compliance that punishes complacency. The Internal Revenue Code, at Section 6672, authorises the IRS to assess a Trust Fund Recovery Penalty (TFRP) against any "responsible person" who "willfully" fails to collect, account for, or pay over trust-fund taxes.

A few definitions. The trust-fund portion of payroll tax is the slice the employer withholds from the employee's paycheck and holds in trust for the federal government: federal income tax withheld (line 3 of the 941) and the employee share of Social Security and Medicare (half of line 5a, line 5c, and all of line 5d). The employer's matching share is not trust-fund money; only the withheld portion is.

A responsible person is anyone with the duty and authority to direct payment of payroll taxes. The IRS applies a multi-factor test: officer or director title, ownership stake, signature authority on bank accounts, hiring and firing authority, control of payroll. Bookkeepers and outside accountants can qualify if they had real control. The IRS routinely assesses TFRP against more than one person at the same employer.

Willful does not require malice. It requires that the responsible person knew the taxes were owed and chose to pay other creditors (vendors, landlords, the bank) instead. The classic fact pattern: a company runs into cash trouble, the owner pays the rent and the suppliers to keep the doors open, and the payroll-tax deposits are skipped. When the company later fails, the IRS assesses TFRP against the owner personally.

The penalty is 100% of the unpaid trust-fund taxes, not a percentage on top. So if an employer skipped $80,000 of trust-fund deposits, the IRS can assess the responsible persons individually for $80,000 each (with internal coordination so it does not collect more than the total). The corporate-veil protection that shields owners from most business debts does not apply. The TFRP also survives the company's bankruptcy and is not dischargeable in personal bankruptcy.

The takeaway is operational. The 941 is not a paperwork form. It is the public record that the trust-fund taxes were withheld, and the deposit cadence is the public record that they were paid over. Falling behind on deposits is a personal-liability event, not a cash-management decision.

Form SS-4 and the EIN: Where the Whole System Starts

Every form 941 requires an Employer Identification Number (EIN) in the header. The EIN is issued by the IRS via Form SS-4, the Application for Employer Identification Number, filed once per legal entity at the point the entity decides it will hire employees, open a business bank account, or file an entity-level tax return.

SS-4 is a one-page application that asks for the legal name and trade name of the entity, the responsible-party SSN, the entity type (sole proprietorship, partnership, corporation, LLC, etc.), the reason for applying ("started new business" or "hired employees"), and the projected number of employees and first payroll date. The IRS has three filing channels: online (instant issuance, the only realistic path for US-based applicants), fax (about four business days), and mail (four to five weeks). Foreign applicants without an ITIN cannot use online and must use fax or phone.

The EIN issued from the SS-4 is the same EIN that appears on the W-9 form when the entity acts as a payer, on the W-2 and 1099 it issues at year-end, and at the top of every 941 and 940 it files. One EIN, one entity, one set of returns. A legal-entity name change keeps the EIN; a change in legal structure (sole proprietorship to LLC, LLC to S-corp election) usually requires a new EIN.

The single most common SS-4 mistake is the responsible party field. The IRS requires a natural person with control of the entity, not a holding company or trust, and the responsible party should be updated via Form 8822-B within 60 days when it changes. A stale responsible-party record can route IRS payroll-tax correspondence to the wrong person, which means TFRP notices can land somewhere they will not be read.

How Good Form Fits Around the 941

Form 941 itself is a tax return the IRS expects you to file from your payroll system, and the line-by-line numbers come out of payroll software, not a form builder. What you can do is make sure the operational data the 941 depends on is captured cleanly and confirmed quarterly: the EIN as issued on the SS-4, the legal-entity name as registered, the depositor-status set from the lookback calculation, and the headcount snapshot for the four mid-quarter pay dates that line 1 asks for.

Good Form is a form builder used by HR teams and small finance teams to run the intake side of employment paperwork: new-hire packets, federal forms, and pre-filing prep capture for forms like the 1099 and the W-2. For the 941, Good Form lives upstream: it captures and confirms the EIN, responsible-party name, depositor schedule, and mid-quarter headcount before each quarter closes, so the quarterly run reads from already-verified data rather than scrambling for it.

The Companion Template

The Good Form 941 quarterly intake template (clone it here) is a per-quarter readiness capture for the data form 941 depends on. It asks the preparer to confirm the EIN exactly as issued on the SS-4, the legal-entity name as registered with the IRS, the deposit schedule (monthly or semiweekly) as determined by the prior-year lookback, the mid-quarter pay-date headcount for line 1, and a checkbox acknowledgement that the operational facts feeding the 941 have been verified before the payroll system pulls the return.

It does not replace Form 941, which payroll software produces and either e-files or prints. It is the data-hygiene step that catches the operational errors before they hit the return: a stale EIN, a forgotten deposit-schedule change for the new year, a missed mid-quarter pay-date snapshot. Run it the week before each quarter close and the filing becomes a verification, not a reconciliation.

Form 941 is the quarterly heartbeat of US payroll-tax compliance. The deposits arrive continuously, the return reconciles four times a year, and the Trust Fund Recovery Penalty is what happens when the heartbeat stops.