Form 940 is the federal Employer's Annual Federal Unemployment (FUTA) Tax Return that every US employer who paid wages to employees during the year files once a year to report and pay the federal unemployment tax. Where the Form 941 is the quarterly accounting that reconciles federal income tax withholding plus Social Security and Medicare four times a year, the form 940 is the annual return that runs alongside it on a different cadence, with a different wage base, a different tax rate, and a completely different deposit rhythm. FUTA pays for the federal half of the federal-state unemployment-insurance system; SUTA, paid to each state, covers the state half. The two systems credit against each other on Form 940 itself, which is what produces the famous 0.6% effective rate that most employers actually see.

This guide is the line-by-line walkthrough of form 940 for a US employer in 2026: what each numbered line reports, why the 6.0% statutory FUTA rate drops to 0.6% for most employers, the $7,000 per-employee wage base that caps the FUTA wage figure regardless of pay level, the $500 quarterly deposit threshold that decides whether you make deposits during the year or just pay with the return, Schedule A and the credit-reduction state mechanism, the Form 941 quarterly sibling that runs on a different clock, and the Form 944 annual alternative for the smallest employers. The audience is small-business owners, HR teams of one to ten, office managers running payroll without a CPA on retainer, and finance leads picking up payroll responsibility from a previous owner. If you want a clean intake that captures the EIN, state SUTA list, credit-reduction status, and quarterly liability data every 940 depends on before you file your return, clone the Good Form 940 annual intake template.

The short version:

- Form 940 is the Employer's Annual Federal Unemployment Tax Return. It reports, for one employer for one year, the federal unemployment tax owed on the first $7,000 of wages paid to each employee during the year.

- It is filed once a year. The return for the year just ended is due January 31 of the following year. If every required quarterly deposit was made on time and in full, the filing deadline extends to February 10.

- The statutory FUTA rate is 6.0% on the first $7,000 of wages per employee. For most employers, the state UI credit drops the effective rate to 0.6%, capping FUTA at $42 per employee per year.

- The wage base is per employee per year, not per quarter and not per job. An employee who hits $7,000 in February stops accumulating FUTA wages for the rest of the year. An employee who works for two of your entities accumulates separately under each EIN.

- FUTA is employer-only. There is no employee share, no withholding, and the employee never sees it on a paycheck or a W-2.

- The $500 deposit threshold governs when you deposit. If quarterly FUTA liability is under $500, carry it forward. When the running total crosses $500, deposit by the end of the next month. If the year-end total is still under $500, pay with the return.

- Schedule A (Form 940) is required for multi-state employers and for single-state employers in a credit-reduction state. It computes the per-state credit-reduction increase that lands on line 11 of the main return.

- A credit-reduction state is one that has borrowed from the federal unemployment trust fund and not repaid on schedule. The credit reduction adds 0.3% per year the state has been behind, raising the effective rate by 0.3%, 0.6%, 0.9% and so on. The IRS publishes the year's credit-reduction state list in November.

- Form 944 is the annual alternative to Form 941 for the smallest employers (annual federal employment tax liability of $1,000 or less). Form 940 has no such alternative; every FUTA-paying employer files 940, regardless of size.

What Form 940 Is and Why It Exists

Form 940, formally the Employer's Annual Federal Unemployment (FUTA) Tax Return, is the once-a-year report every US employer with employees files to compute and pay the federal half of the federal-state unemployment insurance system. FUTA is collected by the IRS and used to fund federal-level unemployment programs (administrative costs of the state UI systems, the federal extended-benefits programs, and loans to states whose UI trust funds run dry). SUTA, the state version, is paid to each state separately and funds the actual unemployment-benefit payments to laid-off workers.

The two systems are deliberately interlocked. The federal statute sets FUTA at 6.0%, but credits up to 5.4 percentage points back to the employer for the state UI tax they paid to a participating state. The intent is that employers who pay their SUTA on time and in full to a state with a federally-conforming UI program face a residual 0.6% federal rate. Employers in states that have stopped conforming, or who paid SUTA late, lose part of the credit and pay a higher effective FUTA rate. Form 940 is the return that computes those credits and lands at the effective number.

The form is filed with the IRS, not with any state. State unemployment is paid to the state UI agency on the state's own forms and schedule. Form 940 is the federal piece only, and the state UI payments enter only as the credit calculation. The IRS publishes the form annually because the credit-reduction state list changes year-to-year (states fall into and out of credit-reduction status based on their loan repayment status as of November 10 each year).

The 2026 Due Date and the Ten-Day Filing Extension

Form 940 has one filing deadline per year. The return for the calendar year just ended is due January 31 of the following year. The 2025 return is due February 2, 2026 (January 31, 2026 is a Saturday, so the deadline shifts to the next business day under the IRS weekend-and-holiday rule). The 2026 return will be due February 1, 2027 (January 31, 2027 is a Sunday).

There is one built-in filing extension. If the employer made every required quarterly FUTA deposit on time and in full during the year, the filing deadline extends from January 31 to February 10. This is the same all-deposits-on-time extension that applies to the Form 941. The extension applies only to the return; it does not extend any deposit deadline that has already passed.

Where you mail a paper 940 depends on your state and on whether you are paying with the return. The IRS publishes the addresses in the form instructions and they change occasionally. E-filing through the IRS MeF system avoids the address question entirely and is the default path for most employers. Most payroll software files 940 electronically as part of the year-end run.

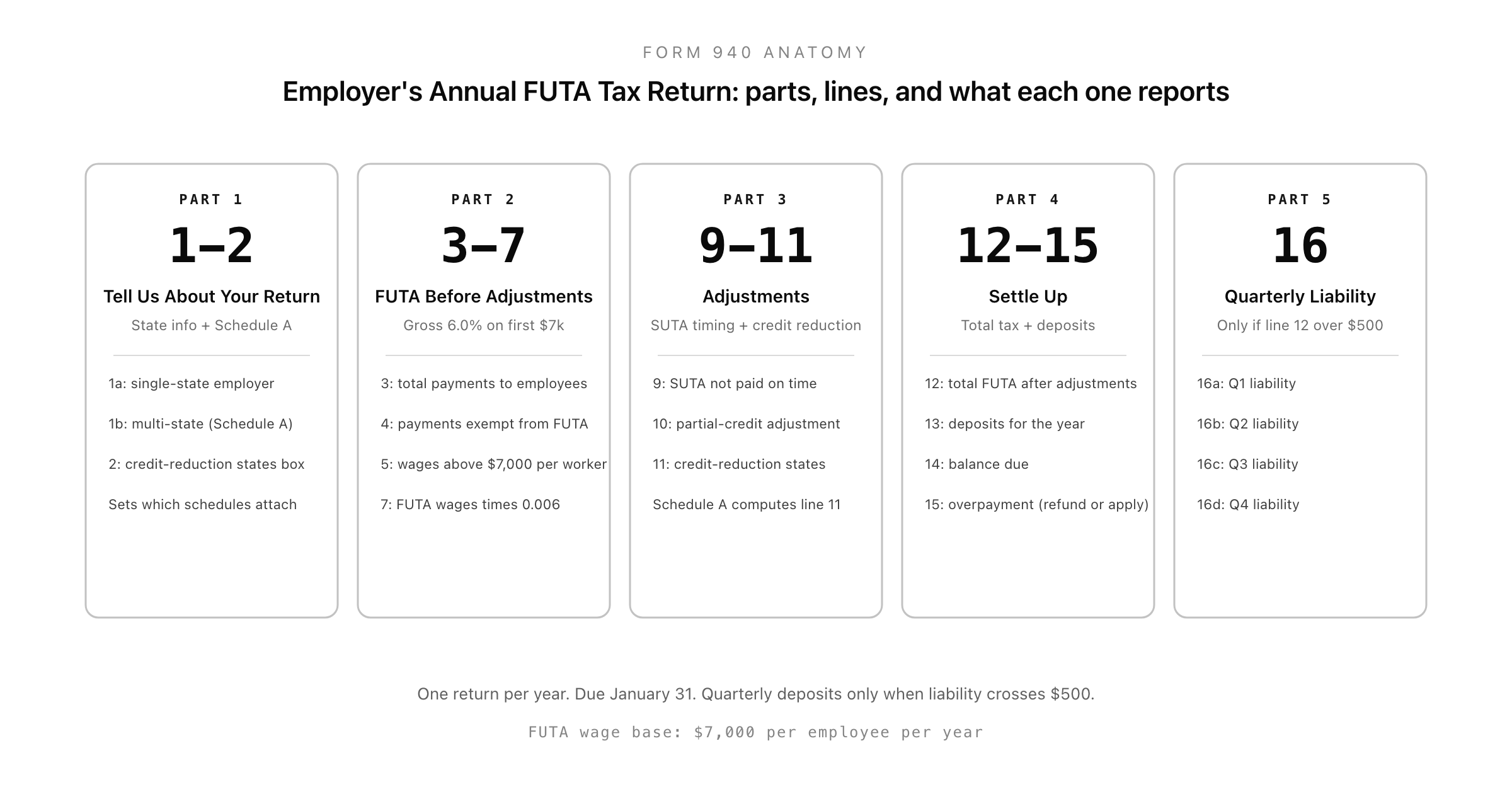

The Form 940 Line-by-Line Walkthrough

Part 1: Lines 1a, 1b, and 2, the state info that sets Schedule A

Part 1 is three short lines that decide the rest of the return.

Line 1a is for single-state employers: tick the box and enter the two-letter abbreviation of the state where SUTA was paid. Line 1b is for multi-state employers: tick the box and complete Schedule A listing every state. Line 2 is a separate box for any employer whose state appears on the year's credit-reduction list, single-state or multi-state. A single-state employer in a credit-reduction state ticks line 1a AND line 2, and still attaches Schedule A so the per-state increase computes properly.

The Part 1 boxes determine which schedules attach and which credits apply. They are the most common spot for a quiet mistake: an employer who hired into a new state mid-year and forgot to register for SUTA in the new state will still tick line 1a as a single-state employer and miss the multi-state Schedule A entirely. The downstream effect is that the credit-reduction add-on for the new state never lands on line 11, and the IRS computes a balance due during processing.

Part 2: Lines 3 to 7, the FUTA tax before adjustments

Part 2 is the wage and tax base. The arithmetic is simple in principle: total payments to employees, minus payments that are exempt from FUTA, minus payments above the $7,000 per-employee wage base, equals FUTA-taxable wages, times 0.006 equals FUTA tax before adjustments.

Line 3 is total payments to all employees in the year: gross compensation, pre-exemption, pre-cap. The starting figure. Line 4 is the exempt-payments subtotal: fringe benefits (group-term life insurance under $50,000, dependent-care assistance under $5,000), retirement and pension contributions, payments to retirees, statutory non-employees, and certain other narrow categories. Line 4 also breaks down by category in checkboxes 4a through 4e for the IRS's reconciliation. Line 5 is the total of payments above the $7,000 per-employee wage base, summed across all employees. Line 6 is the sum of lines 4 and 5 (total subtractions). Line 7 is line 3 minus line 6: the FUTA-taxable wages.

Line 7a is line 7 times 0.006, which is the FUTA tax before adjustments. This is the number the rest of the form either reduces (no, actually only marginally adjusts) or increases (via the credit-reduction mechanism).

The $7,000 wage base is the cap that makes FUTA so much cheaper than it looks. A $200,000 executive contributes the same $42 ceiling of FUTA as a $20,000 part-timer. A 50-person company with average wages of $50,000 has $2.5 million of payroll but only $350,000 of FUTA-taxable wages (50 × $7,000), and FUTA tax of $2,100 (0.006 × $350,000). The wage base also resets each calendar year, not each pay period, which means an employee who hits $7,000 of wages in February stops accumulating FUTA wages until January.

Part 3: Lines 9 to 11, the adjustments

Part 3 is two adjustments that handle the cases where the simple 0.6% effective rate breaks down.

Line 9 is for employers whose FUTA-taxable wages are NOT subject to state UI at all (the entire wages, not just some). This is rare: it applies to wages paid for services that no state's UI program covers, such as certain agricultural or household work outside a participating state, or to wages exempt under a tribal sovereignty arrangement. If line 9 applies, line 7a is multiplied by 0.054 (not 0.006), because there is no state credit available against those wages. Most employers leave line 9 blank.

Line 10 is for employers whose state UI was paid LATE. The federal credit drops from 5.4% to 5.4% × 90% = 4.86% on any wages where the SUTA was not paid by the Form 940 filing deadline (January 31). This is the late-SUTA adjustment, computed using the worksheet in the 940 instructions. Most employers also leave line 10 blank, because most pay their state UI on time.

Line 11 is the credit-reduction adjustment, computed on Schedule A. This is the line that brings the per-state credit-reduction increase into the main return. If any state where the employer paid SUTA is on the year's credit-reduction list, Schedule A computes 0.3% (or 0.6%, or 0.9%, depending on how many consecutive Januaries the state has been behind) times the FUTA-taxable wages in that state, and the sum lands on line 11.

Part 4: Lines 12 to 15, the settle-up

Line 12 is the total FUTA tax after adjustments: line 7a plus or minus the line 9 / 10 / 11 adjustments. This is the bottom of the calculation, the total FUTA tax the employer owes for the year.

Line 13 is total FUTA deposits made for the year, including any prior-year overpayment carried in. Line 14 is balance due: if line 12 is more than line 13, the difference is owed with the return. Line 15 is overpayment: if line 13 is more than line 12, the employer can check a box to either get the overpayment refunded or apply it as a credit to the next year's 940.

The reconciliation is structurally identical to the Form 941 settle-up at lines 13 to 15. The numbers are smaller because FUTA is smaller, but the logic is the same: the deposits arrived through the year, and the return is where you prove what they were supposed to add up to.

Part 5: Line 16, the quarterly liability breakdown

Line 16 is required only if line 12 (total FUTA tax after adjustments) is over $500. It splits the annual FUTA tax across four quarterly lines: 16a (Q1), 16b (Q2), 16c (Q3), 16d (Q4). The sum across the four quarters must equal line 12.

Line 16 is what the IRS uses to check that the quarterly deposits arrived in the right quarters. It does not change the tax owed; it audits the timing. Employers whose entire year stayed under $500 in liability leave line 16 blank because no deposits were required.

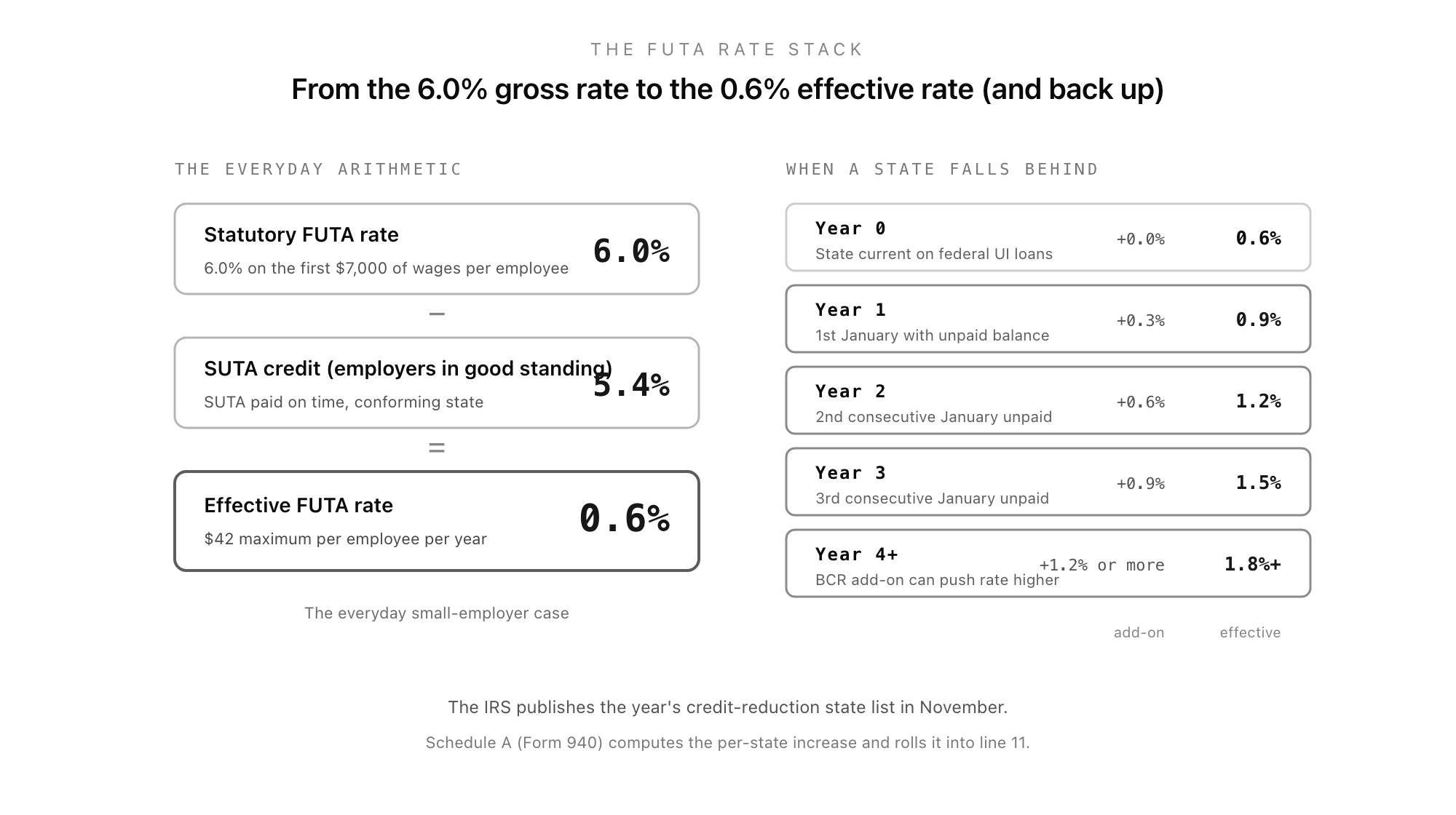

The FUTA Rate Stack: 6.0% Down to 0.6% (and Back Up)

The everyday arithmetic for most employers is short.

The statutory FUTA rate is 6.0% on the first $7,000 of wages per employee per year. That is the federal-law starting point and it is the rate any employer would face if no state UI system existed.

The state UI credit drops the federal rate by up to 5.4 percentage points for employers who paid SUTA on time and in full to a state with a federally-conforming UI program in good standing on the federal repayment schedule. Subtract: 6.0% minus 5.4% equals an effective FUTA rate of 0.6%.

At 0.6% on a $7,000 wage base, the maximum FUTA per employee per year is $42. A 25-employee company with all employees over $7,000 of annual wages pays a maximum of $1,050 of FUTA for the entire year. The federal share is genuinely small; the state SUTA bill is usually multiples of it.

The rate climbs back up in two cases. The late-SUTA adjustment on line 10 reduces the credit from 5.4% to 4.86% for the late wages, raising the rate from 0.6% to 1.14% on those wages. The credit-reduction adjustment on line 11 raises the rate by 0.3% per year the state has been behind on its federal UI loan repayments.

The credit-reduction mechanism is what trips employers in newly-affected states. The IRS publishes the list in November based on each state's status as of November 10. A state that started borrowing in 2024 and didn't repay by November 10, 2026 would face a 0.3% credit reduction on 2026 wages. The same state, still unpaid by November 10, 2027, would face 0.6%. By the time the credit reduction hits 0.9% or 1.2%, the effective FUTA on that state's wages can rival the SUTA itself.

Multi-state employers see the credit reduction state by state. A California employer with workers also in Nevada and Oregon would compute Schedule A separately for each state: each row gets the FUTA wages paid in that state times that state's credit-reduction percentage, summed into the line 11 add-back. Single-state employers in a non-credit-reduction state can skip Schedule A entirely; single-state employers in a credit-reduction state still attach it.

The $500 Deposit Threshold

Form 940 has a different deposit rhythm to Form 941. There is no monthly or semiweekly schedule. There is one threshold: $500 of accumulated quarterly liability.

The rule works on a rolling basis through the year:

- Quarterly FUTA liability under $500. No deposit required for the quarter; carry the balance forward and combine with the next quarter.

- Cumulative liability crosses $500. Deposit the entire accumulated amount by the end of the next month. The clock then resets, and the next quarter's liability accumulates again against a fresh $500.

- Year-end cumulative liability under $500. No deposit required at all; pay the entire FUTA tax with the annual 940 return.

A small employer with $1,200 of annual FUTA might never trigger a quarterly deposit (each quarter's $300 stays below the threshold), pay nothing during the year, and write one check for $1,200 with the January 940. A mid-size employer with $4,000 of annual FUTA might trigger every quarter (each quarter's $1,000 exceeds the threshold), making four deposits at end-of-April, end-of-July, end-of-October, and end-of-January.

The end-of-January deposit is technically also deemed timely with the return: a Q4 liability crossing $500 can be deposited or paid with the 940 itself by January 31, instead of requiring a separate deposit. That is the only quarter where the deposit deadline and the filing deadline align.

All FUTA deposits must be made via EFTPS (the Electronic Federal Tax Payment System), the same system used for Form 941 deposits. The IRS no longer accepts paper FUTA payments above any threshold for the routine case.

940 vs 941: Two Returns, Two Cadences, Same EIN

Form 940 and Form 941 are filed separately, on different cadences, with different deposit mechanics, but they describe the same employment relationship.

The structural differences:

- Form 941 is quarterly; Form 940 is annual. Four 941s per year, one 940.

- Form 941 covers federal income tax withholding plus Social Security and Medicare (FICA); Form 940 covers federal unemployment (FUTA). Different taxes, different statutes, different trust funds.

- Form 941 has both an employee share and an employer share of FICA; Form 940 is employer-only. FUTA never appears on a paycheck and never lands on a W-2.

- Form 941's wage base is the Social Security wage base ($168,600 in 2024, indexed annually); Form 940's wage base is the unchanging $7,000. The Social Security base goes up each year with the national wage index; the FUTA base has been $7,000 since 1983.

- Form 941 deposits run on a continuous monthly or semiweekly schedule keyed to the lookback rule; Form 940 deposits trigger only when quarterly liability crosses $500. Most small employers make zero FUTA deposits during the year.

- Form 941 has a 941-X correction return; Form 940 corrections are filed by amending a new 940 with the "Amended" box ticked and a written explanation attached. No separate amendment form.

What they share is the EIN, the legal-entity name, the employee headcount, and the wage base in the sense that the totals across the four 941s and the totals on the 940 must be internally consistent for the year. A mismatch between FUTA-taxable wages on line 7 of the 940 and the implied wages from headcount on lines 1 to 5 of the four 941s can prompt an IRS reconciliation notice.

Form 944: The Annual Alternative to Form 941

While Form 940 has no quarterly alternative, Form 941 has an annual alternative for the smallest employers: Form 944, the Employer's Annual Federal Tax Return.

Form 944 is for employers whose annual total of FICA plus federal income tax withholding is $1,000 or less. At that level, quarterly 941 filings are administrative overkill: the IRS would rather receive one annual 944 than four near-empty 941s. Eligibility is determined by the IRS in writing; an employer cannot self-select onto Form 944. The IRS notifies eligible employers by letter, usually in February for the current year, and the employer files Form 944 for that year instead of four 941s.

Two important interactions with Form 940. First, an employer on Form 944 still files Form 940 separately on the normal annual schedule. The 944 covers income-tax withholding and FICA; the 940 still covers FUTA, and FUTA is administered independently. Second, an employer on Form 944 still deposits FUTA quarterly when the $500 threshold trips. The 944 election only affects the FICA / withholding deposit schedule, not the FUTA deposit schedule.

Most small employers never see Form 944 because they cross the $1,000 threshold quickly. A single full-time employee on average wages typically produces enough FICA in a year to exceed it. Form 944 is realistic only for very small operations: a one-employee S-corp paying the owner a modest salary, a household-employer who has elected to file under business rules, or a brand-new business with one or two months of operation in the year.

Common Form 940 Errors and How to Avoid Them

Three errors cause most of the IRS notices employers receive after filing the 940.

The first is forgetting to update the Schedule A list when adding a new state mid-year. An employer who hires into a new state in Q3 must register for SUTA in that state AND must add that state to Schedule A on the 940 for the year. The most common pattern is an employer who tracks Q4 SUTA payments to the new state correctly through payroll but forgets to switch from line 1a (single-state) to line 1b (multi-state) on the 940 itself. The downstream notice asks for the missing Schedule A.

The second is late SUTA payments triggering the line 10 credit reduction. A SUTA payment made after January 31 reduces the federal credit on that quarter's wages from 5.4% to 4.86%, raising the effective FUTA rate from 0.6% to 1.14% on those wages. The line 10 calculation is fiddly: it asks for the state UI taxes that were paid by January 31 versus those paid late, broken down separately, and produces a worksheet number. Most payroll software handles this automatically when fed accurate SUTA payment dates, but employers who pay SUTA manually outside the payroll system frequently miss the late portion.

The third is the $7,000 wage base reset on rehires within the same year. The $7,000 wage base is per employee per year, not per spell of employment. An employee who works for the employer from January to April, hits $7,000 of FUTA wages in March, terminates in April, and is rehired in October starts October on a $7,000 cumulative FUTA wage base. No new wages of theirs accumulate FUTA-taxable in October, November, or December. Conversely, an employee who works for two unrelated employers in the same year accumulates $7,000 separately under each EIN (each employer pays FUTA on its first $7,000 to that employee). Multi-entity ownership groups with employees moving across entities need to track this entity-by-entity, not aggregated.

How Good Form Fits Around the 940

Form 940 itself is a tax return the IRS expects you to file from your payroll system, and the line-by-line numbers come out of payroll software, not a form builder. What you can do is make sure the operational data the 940 depends on is captured cleanly and confirmed once a year: the EIN as issued on the SS-4, the legal-entity name as registered, the single-state vs multi-state status (so Schedule A attaches when it should), every state where SUTA was paid (so the credit-reduction add-on lands correctly), the SUTA-payment timing (so the line 10 adjustment is computed correctly), and the running quarterly FUTA liability against the $500 threshold (so the quarterly deposit cadence is documented).

Good Form is a form builder used by HR teams and small finance teams to run the intake side of employment paperwork: new-hire packets, federal forms, and pre-filing prep capture for forms like the 1099, the W-2, and the Form 941. For the 940, Good Form lives upstream: it captures and confirms the EIN, multi-state status, every state's SUTA experience-rate, the credit-reduction flag, and the running per-quarter liability against the $500 threshold before the year-end payroll run pulls the return.

The Companion Template

The Good Form 940 annual intake template (clone it here) is a once-a-year readiness capture for the data Form 940 depends on. It asks the preparer to confirm the EIN exactly as issued on the SS-4, the legal-entity name as registered with the IRS, the single-state vs multi-state status (with the state abbreviation or the multi-state list), the credit-reduction-state flag for the year, every line 3 through line 5 wage figure that drives the FUTA-taxable wage calculation, the quarterly deposit pattern against the $500 threshold, the line 16 quarterly breakdown if line 12 exceeds $500, and explicit checkbox acknowledgements that SUTA was paid on time (to avoid the line 10 credit reduction) and Schedule A is attached when required.

It does not replace Form 940, which payroll software or a preparer produces and either e-files or prints. It is the data-hygiene step that catches the operational errors before they hit the return: a missing new-state SUTA registration, a forgotten credit-reduction flag, a stale entity name, a late SUTA payment that should have triggered the line 10 calculation. Run it in early January after the year closes and before the year-end payroll run computes the 940, and the filing becomes a verification, not a reconstruction.

Form 940 is the annual heartbeat of US federal unemployment-tax compliance. The wage base is small, the rate is small, and the deposits are infrequent. The errors are small too, but they compound year after year if the operational facts (which states, which SUTA timing, which credit-reduction status) aren't captured cleanly at the source. One return per year, due January 31, on $42 per employee per year before any credit-reduction add-on. Get the inputs clean and the return follows.