The Form 1099-R is the statement a payer sends to a recipient, and files with the IRS, to report money that came out of a pension, annuity, profit-sharing or retirement plan, an IRA, or an insurance contract during the year. If you are a plan administrator, an IRA custodian, an annuity issuer, or any business that paid out $10 or more of retirement money, the 1099-R is how you report what left the account, how much of it is taxable, how much tax you withheld, and (through a single short code) how the IRS should tax it. It is not a form the recipient fills in. It is your report, and the recipient uses it to fill in their own return.

This is the 2026 walkthrough of the form 1099-R for the payer who has to file it: what the form does, who files it and when, the difference between Box 1 (gross) and Box 2a (taxable amount) that trips up most filers, the Box 7 distribution codes that carry all the tax meaning, the IRA/SEP/SIMPLE checkbox, how a direct rollover is reported, the early-distribution penalty the codes flag, and the furnishing and e-filing deadlines. If you administer a retirement plan and want a clean way to capture each distribution before your filing vendor needs it, clone the Good Form 1099-R intake template before year-end.

The short version:

- Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc., is filed by the payer for each recipient who received $10 or more of distributions during the year. The recipient gets a copy; the IRS gets a copy.

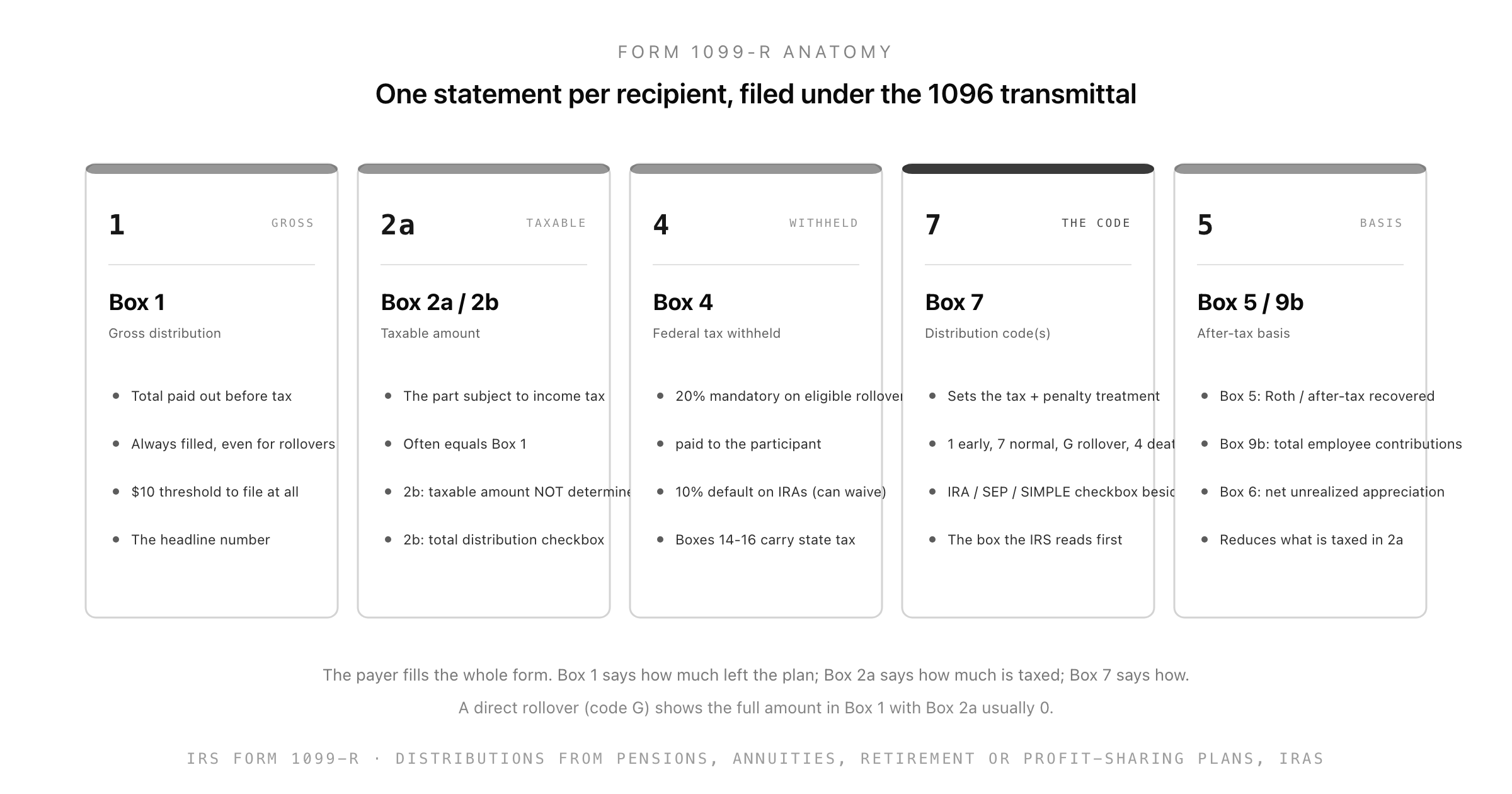

- Box 1 is the gross distribution (everything that left the account). Box 2a is the taxable amount (the part subject to income tax). They are often equal, but not always, and confusing the two is the most common 1099-R error.

- Box 2b carries two checkboxes: "taxable amount not determined" (used by IRA trustees who cannot compute basis) and "total distribution" (the account was fully emptied).

- Box 7 is the keystone. Its one or two distribution codes tell the IRS whether the money is taxed now and whether the 10% early-distribution penalty applies. Code 7 is a normal distribution, code 1 is an early distribution with no known exception, code G is a direct rollover, code 4 is a death benefit.

- The IRA/SEP/SIMPLE checkbox next to Box 7 says the distribution came from an IRA rather than a qualified employer plan. It changes which rules and which boxes apply.

- Box 4 is federal income tax withheld. A 20% mandatory rate applies to an eligible rollover distribution paid to the participant; a 10% default applies to IRA and periodic payments, which the recipient can adjust or waive on Form W-4P / W-4R.

- A direct rollover (code G) reports the full amount in Box 1 with Box 2a usually 0, because the money moved trustee-to-trustee and is not taxed now.

- Deadlines: furnish the recipient copy by January 31; file with the IRS by February 28 on paper or March 31 electronically. Electronic filing is mandatory once you file 10 or more information returns of any type in aggregate.

- Get Box 1, Box 2a, and Box 7 right and the 1099-R does its whole job: it tells the recipient and the IRS exactly how much of the distribution is taxed and why.

What the Form 1099-R Is and Who Files It

Form 1099-R reports distributions from tax-advantaged retirement vehicles and certain insurance contracts. The list of what it covers is broad: traditional, Roth, SEP and SIMPLE IRAs; 401(k), 403(b), and 457(b) plans; defined-benefit pensions; commercial and charitable annuities; profit-sharing plans; and some life-insurance and endowment contracts. If money came out of any of those and reached the recipient (or moved on their behalf), a 1099-R is how it gets reported.

The payer files it. That is whoever actually controls and distributes the funds: the plan administrator or trustee, the IRA custodian, the annuity company, the insurer. The recipient does nothing with the form except keep it and copy the numbers onto their own Form 1040. The 1099-R's audience is twofold: the recipient, who needs it to file, and the IRS, which matches it against what the recipient reports.

The threshold is low. A 1099-R is required for any designated distribution of $10 or more. That $10 floor is far below the $600 threshold most people associate with the 1099-NEC; retirement reporting is deliberately comprehensive, because the IRS wants every dollar of distributed retirement money on the record. A federal pension paid to a retiree or survivor shows up on the same form with a "CSA" or "CSF" prefix on the OPM-issued version (the CSA 1099-R), but the boxes and codes work the same way.

Box 1 vs Box 2a: Gross Distribution and Taxable Amount

The single most important thing to understand about the 1099-R is that Box 1 and Box 2a are not the same number, and the difference is where the tax lives.

Box 1, Gross distribution, is the total amount that left the account before any withholding or adjustment. It is always filled in. Even a direct rollover, where nothing is taxed, shows the full amount in Box 1.

Box 2a, Taxable amount, is the portion of Box 1 that is subject to income tax. For most plain-vanilla distributions from a fully pre-tax account, Box 2a equals Box 1: every dollar was contributed before tax, so every dollar is taxed coming out. But Box 2a is smaller than Box 1 whenever some of the money was already taxed going in, which happens with after-tax 401(k) contributions, nondeductible IRA contributions, qualified Roth distributions, or the cost basis in an annuity. The difference between the two boxes is the recipient's basis, the money they already paid tax on, and it should not be taxed twice.

This is also why people search for 1099-r taxable amount so often: they see two different dollar figures and want to know which one they actually owe tax on. The answer is Box 2a, with the caveats that Box 2b and Box 7 add.

Box 2b: The "Taxable Amount Not Determined" Trap

Box 2b is two small checkboxes that change how Box 2a should be read.

The "Taxable amount not determined" box is checked when the payer genuinely cannot compute the taxable portion. IRA trustees check it routinely, because they do not track the owner's nondeductible-contribution basis (that lives on the owner's Form 8606). When this box is checked, Box 2a is often left blank or simply repeats Box 1, and the burden shifts to the recipient to figure out the taxable amount on their own return. A checked 2b is not a free pass to ignore the tax; it is a signal that the payer is not vouching for the Box 2a figure.

The "Total distribution" box is checked when this payment emptied the account entirely. It tells the IRS no further distributions are coming from this plan, which matters for things like net unrealized appreciation, lump-sum elections, and basis recovery.

For a qualified employer plan, the payer usually can and does determine the taxable amount, so 2b stays unchecked. For IRAs, expect 2b checked far more often. Knowing which situation you are in keeps you from either over-reporting the taxable amount or leaving a recipient stranded without one.

Box 7: The Distribution Codes That Carry the Tax Treatment

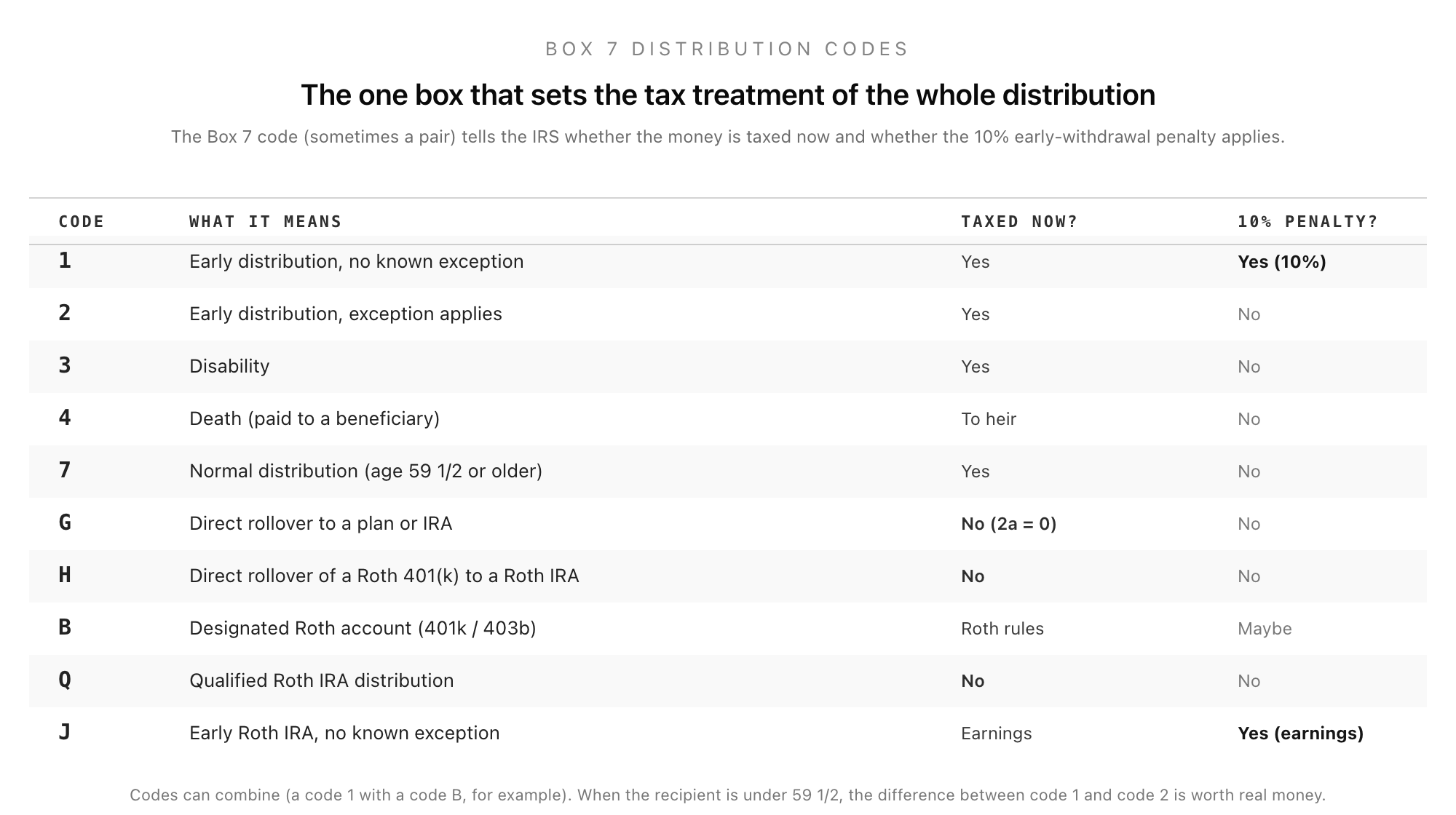

Box 7 is the heart of the form. It holds one or two characters, and those characters tell the IRS, in shorthand, exactly how to treat the distribution: whether it is taxed now, whether it is a rollover, whether it is a death benefit, and crucially whether the 10% additional tax on early distributions applies.

The codes you will use most:

- Code 7, Normal distribution. The recipient was at least 59 1/2. Taxable per Box 2a, no early-withdrawal penalty. The default for most retiree payments. People search 1099-r distribution code 7 precisely because it is the most common code on the form.

- Code 1, Early distribution, no known exception. The recipient was under 59 1/2 and you are not aware of an exception. Taxable, and the 10% additional tax applies. This is the expensive code.

- Code 2, Early distribution, exception applies. Under 59 1/2, but a known exception removes the penalty (a series of substantially equal periodic payments, a qualified first-home or higher-education distribution from an IRA, an IRS levy, and so on). Taxable, no penalty.

- Code 3, Disability. The recipient is disabled within the meaning of the code. Taxable, no penalty.

- Code 4, Death. Paid to a beneficiary after the account owner's death. Taxable to the heir, never subject to the early-distribution penalty regardless of the heir's age.

- Code G, Direct rollover. Covered in its own section below. Not taxed now.

- Codes B, H, J, Q, T, and others handle the Roth world (designated Roth accounts and Roth IRAs), where the taxability turns on whether the distribution is "qualified" and whether it is contributions or earnings coming out.

Codes can combine. A distribution can carry a code 1 alongside a code B, for example, when an early distribution comes from a designated Roth account. When the recipient is under 59 1/2, the gap between code 1 and code 2 is the difference between owing the 10% penalty and not, so getting the exception determination right is worth real money to the recipient. Anyone trying to understand 1099-r distribution codes is really asking one question: does this code mean I owe extra tax?

The IRA/SEP/SIMPLE Checkbox

Just to the right of Box 7 sits a small but consequential checkbox: IRA/SEP/SIMPLE. Check it and you are telling the IRS the distribution came from a traditional IRA, a SEP-IRA, or a SIMPLE IRA, rather than from a qualified employer plan like a 401(k) or a pension.

That single checkbox changes the rules that apply. IRA distributions follow the IRA basis-recovery rules (tracked by the owner on Form 8606), are far more likely to have "taxable amount not determined" checked in Box 2b, and have their own penalty exceptions. A SIMPLE IRA distribution in the first two years of participation even has its own elevated penalty (25% rather than 10%), flagged with code S in Box 7. Leave the box unchecked for 401(k), 403(b), pension, and annuity payments. The checkbox and the Box 7 code together tell the whole story of what kind of account this was and how it should be taxed.

Box 4 and Withholding: 20% vs 10%

Box 4 reports the federal income tax you withheld from the distribution, and the withholding rules differ sharply by distribution type.

An eligible rollover distribution paid directly to the participant (rather than rolled trustee-to-trustee) is subject to mandatory 20% federal withholding. This is the rule that catches people who take a 401(k) payout intending to roll it over themselves: 20% is withheld, and to complete a full rollover they have to make up that 20% out of pocket within 60 days or it becomes a taxable, possibly penalized, distribution.

IRA distributions and periodic pension payments instead carry a 10% default withholding rate that the recipient can change or waive entirely. Recipients elect their withholding on Form W-4R (for nonperiodic payments and eligible rollover distributions) or Form W-4P (for periodic pension and annuity payments). If the recipient lives in a state with income tax, Boxes 14 through 16 carry the state tax withheld, the state, and the payer's state number. As the payer you remit what you withhold and report it here; the recipient claims it as tax already paid.

How a Direct Rollover Is Reported (Code G)

A direct rollover is when retirement money moves straight from one plan or IRA to another without the participant taking possession. It is the cleanest way to move money, and it is reported in a way that surprises first-time filers.

When you process a direct rollover, you still issue a 1099-R. Box 1 shows the full amount rolled over. But Box 2a is usually 0, because nothing is taxable now, and Box 7 carries code G (or code H for a direct rollover of a designated Roth 401(k) to a Roth IRA). No 20% withholding applies, because the money never passed through the participant's hands. The result is a 1099-R that reports a large Box 1 and a zero Box 2a, telling the IRS "this much moved, none of it is taxed this year." This is exactly what someone searching 1099-r rollover or 1099-r code g needs to see: the rollover is reported, it is just reported as non-taxable. Forgetting to file the 1099-R because "it wasn't taxable" is a filing error; the form is still required.

Filing Mechanics: Thresholds, Transmittals, and Deadlines

The 1099-R runs on the same year-end information-return calendar as the rest of the 1099 family.

Furnishing to the recipient: the recipient copy is due by January 31 following the distribution year.

Filing with the IRS: the deadline is February 28 if you file on paper, or March 31 if you file electronically. Paper filings travel under a Form 1096 transmittal, the cover sheet that totals the batch and identifies the payer, exactly as the 1096 totals a batch of 1099-NEC forms or the way a W-3 totals W-2s.

Electronic filing is mandatory once you file 10 or more information returns of any type in aggregate. That aggregate threshold (dropped from 250 to 10 for returns due in 2024 and later) counts your W-2s, your 1099-NECs, your 1099-Rs, and every other information return together. In practice most plans well exceed ten distributions a year and e-file through the IRS FIRE system or, increasingly, the IRIS portal, generally via recordkeeping or payroll software rather than by hand.

Corrections follow the standard 1099 correction process: file a new 1099-R marked "CORRECTED," and furnish the corrected copy to the recipient. Because the recipient may have already filed using the original, a corrected 1099-R issued late can force them to amend, so accuracy in the first filing matters more here than almost anywhere else.

Where the 1099-R Sits in the 1099 Family

For a finance team or plan administrator, the 1099-R is the retirement-distribution member of a larger family of year-end information returns, each reporting a different kind of money paid out.

The 1099-NEC reports non-employee compensation to contractors. The 1099-INT and 1099-DIV report investment income. The 1099-R reports distributions from retirement and annuity accounts. All of them share the same January-to-March filing rhythm, the same 1096 transmittal for paper filers, and the same 10-return aggregate e-file mandate. What sets the 1099-R apart is that the taxability is rarely "all of it": the gap between Box 1 and Box 2a, and the meaning packed into the Box 7 code, mean a 1099-R carries far more interpretation than a flat payment report.

If you sponsor a retirement plan, the 1099-R also sits downstream of your annual Form 5500 ERISA return. The 5500 reports the plan's overall financial activity for the year, including total distributions; the 1099-Rs report those same distributions at the per-participant level. Keeping the two reconciled (the sum of your 1099-R Box 1 amounts should tie to the distributions reported on the 5500) is a quiet but real year-end control.

Capturing Distribution Data Cleanly

The hard part of 1099-R reporting is rarely the form itself; it is assembling, per distribution, the facts that decide the boxes. Was the recipient over 59 1/2? Was this a rollover, and was it direct or did the participant take possession? Did any of the money come from after-tax or Roth contributions? Was an early-withdrawal exception established? Each of those answers maps to a specific box or code, and getting them at the moment of distribution is far easier than reconstructing them in January.

A short, structured intake captured when each distribution is processed (the recipient's identity and TIN, the gross amount, the account type, the rollover treatment, the basis if any, and the facts behind the distribution code) is what lets your filing vendor produce clean 1099-Rs without a year-end scramble. The Good Form 1099-R intake template captures exactly those fields in one pass, so the Box 1, Box 2a, and Box 7 inputs are settled long before the January 31 furnishing deadline arrives.

The Short Version

Form 1099-R is the statement a payer files for every recipient who received $10 or more in distributions from a pension, annuity, profit-sharing or retirement plan, an IRA, or an insurance contract. Box 1 reports the gross distribution, everything that left the account; Box 2a reports the taxable amount, the part subject to income tax, which is smaller than Box 1 whenever the recipient has basis from after-tax or Roth money. Box 2b's checkboxes flag a taxable amount the payer could not determine (common for IRAs) or a total distribution that emptied the account. Box 7 is the keystone: its distribution code tells the IRS whether the money is taxed now and whether the 10% early-distribution penalty applies, with code 7 the normal distribution, code 1 the penalized early distribution, code 2 the excepted early distribution, code 4 the death benefit, and code G the non-taxable direct rollover that shows the full amount in Box 1 with Box 2a at zero. The IRA/SEP/SIMPLE checkbox marks an IRA distribution and changes the rules that apply. Box 4 carries the federal tax withheld, 20% mandatory on an eligible rollover distribution paid to the participant and 10% default on IRAs and periodic payments. Furnish the recipient copy by January 31, file with the IRS by February 28 on paper (under a 1096) or March 31 electronically, with e-filing mandatory once you file 10 or more information returns in aggregate. Plan administrators who want a clean per-distribution intake of the amount, account type, rollover treatment, and distribution-code facts before the deadline can clone the Good Form 1099-R intake template and start capturing this year's distributions today.