The Form 5500 is the annual return that an employer-sponsored benefit plan, the kind of plan ERISA governs, files every year with the Department of Labor, the IRS, and the PBGC. If you run a 401(k), sponsor health insurance for fifty staff, or set up a one-person solo 401(k) for yourself, the form 5500 family is how the plan reports who it is, who it covers, what it holds, who it pays for services, and what happened during the year. The form itself is short. The schedules attached to it are where the real disclosure happens, and the question of which variant a plan files (5500, 5500-SF, or 5500-EZ) and which schedules go with it is the question that decides whether the filing takes an afternoon or a full audit.

This is the 2026 walkthrough of the form 5500 for the employer that has to file it: what the annual ERISA return actually does, the line-by-line map of the form and the schedules, the 100-participant gate that separates a small plan from a large plan and triggers an independent audit, the EFAST2 electronic-filing requirement, the July 31 deadline for calendar-year plans, the Form 5558 extension, and how the Delinquent Filer Voluntary Compliance Program (DFVCP) caps the penalty for a plan that missed the date. If you want a clean way to capture the plan-year identifiers and the data points your TPA needs for filing, clone the Good Form 5500 intake template before this year's deadline.

The short version:

- Form 5500 is the annual return that an employee benefit plan governed by ERISA files with the DOL, the IRS, and the PBGC. It covers pension plans (401(k), profit-sharing, defined benefit) and welfare plans (medical, dental, life, disability) above the small-plan exemptions.

- Three variants: 5500 (the full form, large plans and any plan not eligible for SF), 5500-SF (small plans under 100 participants meeting all SF conditions), and 5500-EZ (one-participant owner-only plan, file when assets exceed $250,000 at year-end).

- The schedule map matters more than the form: Schedule A (insurance contracts), Schedule C (service-provider compensation, large plans), Schedule D (DFE participation), Schedule G (loans, leases, prohibited transactions), Schedule H (large plan financial statements), Schedule I (small plan financial info), Schedule R (retirement plan info), Schedule SB (defined benefit actuary), Schedule MB (multiemployer pension actuary).

- The 100-participant rule is the gate. Plans with 100 or more participants at the start of the plan year are "large plans," file the full 5500 with Schedule H, and need an independent qualified public accountant (IQPA) audit attached to the H. Under 100, "small plans" can file 5500-SF if all other SF conditions are met. The "80/120 rule" lets a plan that hovered around 100 keep its prior small or large status if the count stays between 80 and 120.

- Calendar-year plans file by 31 July, the last day of the seventh month after the plan year ends. Form 5558 gives a one-time 2.5-month extension to 15 October; it has to be filed by the original due date.

- Filing is electronic only via EFAST2, the DOL's processing system. The plan administrator signs the filing with EFAST2 credentials, not on paper. Most filings become public on the DOL site.

- Late filing penalties are heavy: up to $250 per day to the IRS (capped at $150,000 per filing) and up to roughly $2,739 per day to the DOL (the DOL rate adjusts annually). The Delinquent Filer Voluntary Compliance Program (DFVCP) caps the DOL penalty at $750 per filing for small plans and $2,000 for large plans (with a cap on multiple late years), if you file before the DOL writes to you.

- The 5500 reports the plan, not the employer. The employer entity files its Form 941 for payroll taxes, Form 940 for FUTA, and W-2 for wages. The 5500 sits next to those as the plan-level annual return that exists because ERISA, not the tax code, requires it.

What the Form 5500 Is and Who Files It

The Employee Retirement Income Security Act of 1974 (ERISA) created a federal regulatory floor for employer-sponsored pension and welfare plans, and the annual report it requires is what eventually became today's Form 5500, Annual Return/Report of Employee Benefit Plan. The form is jointly developed by the Department of Labor's Employee Benefits Security Administration (EBSA), the IRS, and (for defined benefit pension plans) the Pension Benefit Guaranty Corporation (PBGC); the three agencies share what the filing produces.

Two big categories of plan file a 5500. Pension plans include 401(k) and 403(b) salary-deferral plans, profit-sharing plans, money-purchase plans, defined benefit pension plans, and similar retirement arrangements. Welfare plans include employer-sponsored medical, dental, vision, life, disability, severance, and certain fringe-benefit arrangements. Whether a welfare plan has to file depends on its size and structure: small fully-insured or unfunded welfare plans (under 100 participants at the beginning of the plan year) are generally exempt from filing entirely, which is why most small-employer health plans never see a 5500.

The form is the plan's return, not the employer's. The same employer files Form 941 quarterly for payroll-tax purposes and a W-2 for each employee at year-end; those returns are about wages and tax. The 5500 is about the plan itself, its participants, its assets, its service providers, and its operation during the plan year, sitting on a different legal track (ERISA disclosure) from the payroll-tax pillar.

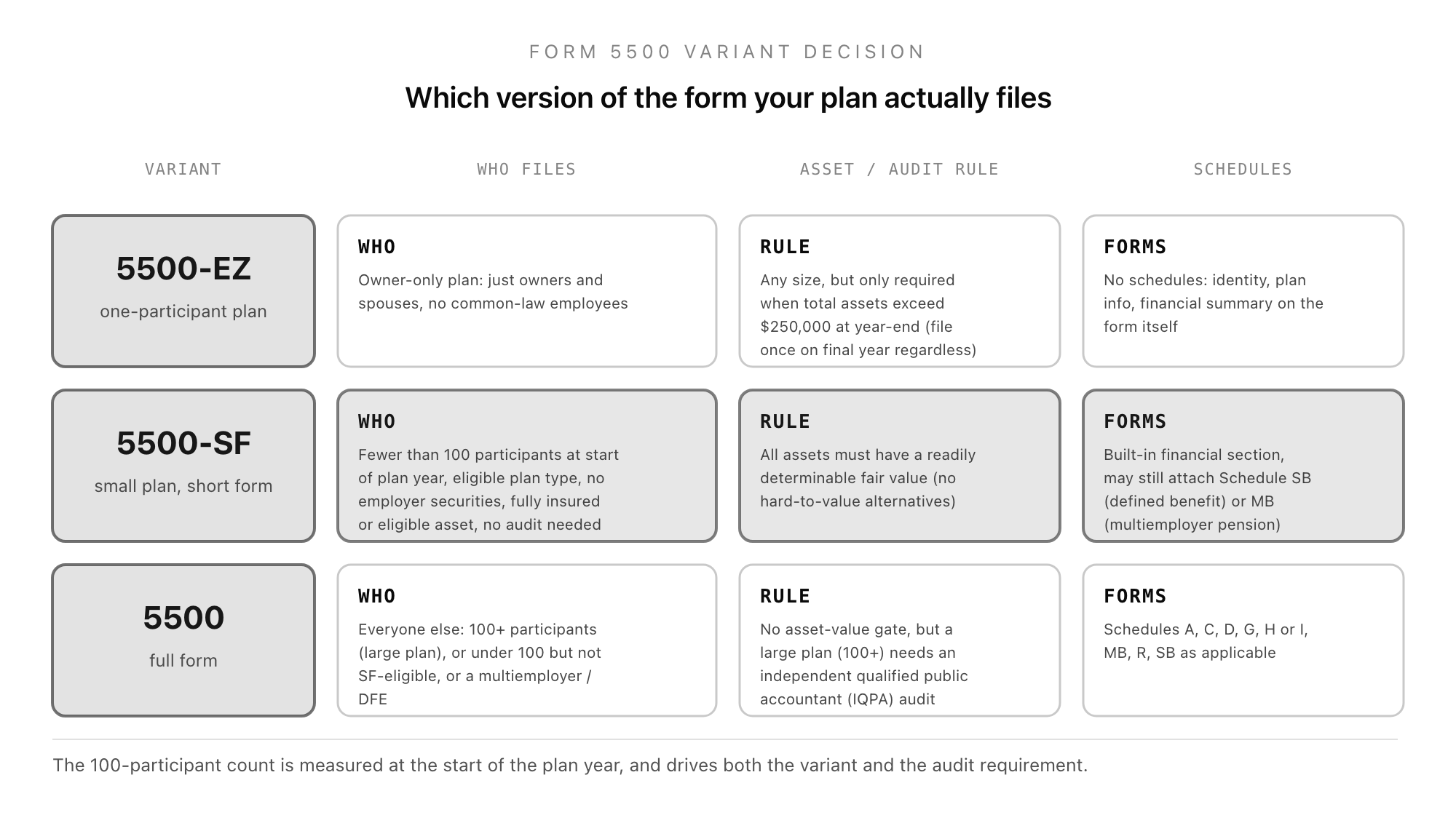

The Three Variants: 5500, 5500-SF, and 5500-EZ

The first decision is which version of the form the plan actually files. The choice comes down to participant count, plan type, and the structure of the assets.

Form 5500-EZ is the one-participant plan return. It is for "owner-only" plans where the only participants are the business owner (and the owner's spouse), or partners in a partnership (and their spouses). A solo 401(k) is the typical case. The 5500-EZ does not need to be filed every year: an EZ filer is required to file only when the plan's total assets at the end of the plan year exceed $250,000, and in the plan's final year regardless of size. When required, it is electronic on EFAST2 (the paper-only era ended) but it stays out of the public-disclosure stream that applies to the standard 5500.

Form 5500-SF is the "short form." It is for small plans (under 100 participants at the start of the plan year) that also meet several other conditions: the plan is not a multiemployer plan, is not required to be audited, holds no employer securities, and (the one most people miss) holds only assets that have a readily determinable fair value. A plan with hard-to-value alternative investments (private real estate, private equity interests held directly) is not SF-eligible even if the headcount is right.

Form 5500 is the full form. Everything that is not EZ-eligible and not SF-eligible files the regular 5500 with the appropriate schedules. That includes large plans (100+ participants), small plans that hold hard-to-value alternative assets or employer securities, multiemployer plans, and Direct Filing Entities (DFEs) such as Master Trusts.

The 100-Participant Rule and the Audit Trap

The single most consequential number on a Form 5500 filing is the count of participants at the start of the plan year. It does two things at once.

First, it decides which financial schedule goes with the form. Small plans (under 100 participants) file Schedule I, a simplified financial information schedule. Large plans (100 or more participants) file Schedule H, a fuller financial statements schedule with line-item assets, liabilities, contributions, distributions, expenses, and net change.

Second, and this is the trap, a large plan filing Schedule H also has to attach an opinion from an independent qualified public accountant (IQPA), in other words, an audit. The audit is a real audit, with field work, sampling of participant data and contribution timing, and a written opinion. For a mid-size 401(k), it commonly runs $8,000-$20,000 a year in audit fees, sometimes more. Plans that grow from 98 participants to 102 over a single year sometimes discover that they have just inherited a recurring five-figure cost they did not budget for.

The DOL provides one mercy here, the so-called 80/120 rule. A plan that filed as a small plan the previous year can continue to file as a small plan in the current year, even if the participant count has crept above 100, so long as the count stays at or below 120. The reverse also applies for a plan dropping from large back toward small. The rule is in the 5500 instructions and is intended to spare plans the audit-cost cliff for a single year of fluctuation.

Counting participants correctly matters. For a 401(k)-type plan, "participants" generally includes active participants (employees who have met the eligibility requirements, whether or not they have actually elected to defer), separated employees with account balances still in the plan, and retired or deceased participants whose beneficiaries are still owed something. It is not just "people currently contributing," which is where employers most often miscount and miss the gate. The instructions to the 5500 give the precise definition for each plan type.

The Schedule Map: What Attaches to a Full 5500

The form 5500 itself is short. The reason filings get heavy is that the schedules carry the disclosure, and which schedules apply depends on what the plan does. Reading a real 5500 means reading the schedules.

Schedule A, Insurance Information. Required for plans that have insurance contracts, including fully-insured pension plans and most welfare plans of any size that contract with an insurer. Each insurance contract gets its own Schedule A, populated by the insurer itself, showing premiums, fees, and commissions paid.

Schedule C, Service Provider Information. Required for large plans only. Lists every service provider that received $5,000 or more in direct or indirect compensation tied to the plan during the year. The indirect-compensation piece is the consequential one: revenue-sharing payments from mutual funds to recordkeepers, fund "12b-1" fees, and similar arrangements that historically were invisible to plan sponsors have to be disclosed here.

Schedule D, DFE/Participating Plan Information. For plans that participate in a Direct Filing Entity such as a Master Trust Investment Account or Common/Collective Trust, or for DFEs themselves.

Schedule G, Financial Transaction Schedules. Where loans deemed uncollectible, leases in default, and prohibited transactions get listed. Most filings do not need a Schedule G; it is the schedule the auditor flags when something has gone wrong.

Schedule H, Financial Information. Large plans only. The full balance-sheet view of the plan, with assets and liabilities and a year-of-year change in net assets, plus the IQPA opinion attachment.

Schedule I, Financial Information (Small Plan). Small plans (under 100) that file the regular 5500. A simpler financial summary than Schedule H.

Schedule MB, Multiemployer Defined Benefit Pension Plan Actuarial Information. Multiemployer pension plans only. Actuarial enrollment data, funding standard account, current liability, withdrawal liability information.

Schedule R, Retirement Plan Information. Most retirement plans attach this. Distributions, single-employer DB plan funding-target attainment percentage, ESOP information for employee stock ownership plans.

Schedule SB, Single-Employer Defined Benefit Plan Actuarial Information. The other actuary schedule. The enrolled actuary signs Schedule SB attesting to the plan's funding target, present value of vested benefits, contributions, and minimum required contribution. For single-employer defined benefit plans, the SB is the schedule the actuary owns and the plan sponsor signs off on, and it is the basis for the PBGC's view of the plan's funded status.

The 5500-SF folds in the financial information directly (so there is no Schedule H or I attached) and does not need Schedules A, C, D, or G. It can still need Schedule SB or MB if the plan is a defined benefit or multiemployer plan that happens to be small.

EFAST2: Electronic Filing Only

Form 5500 filings have not been accepted on paper for plan years 2009 and later. Everything goes through the DOL's EFAST2 (ERISA Filing Acceptance System II), a web application that accepts the form, the schedules, and any required attachments (the IQPA audit report, actuary's certification, summary plan description for the rare initial filing case).

Two roles file electronically. The plan administrator signs the return using credentials issued by EFAST2 after free registration on the site, the credentials being a "Filing Author" or "Filing Signer" ID. The plan sponsor may sign for plans where the sponsor and administrator are the same entity (often the case for small employers). EFAST2 also supports filings prepared by service providers (TPAs and recordkeepers) using their own credentials to author the filing, with the plan administrator signing it.

The system runs validation checks at submission. Common rejections: the prior-year participant count and current-year prior-year-end participant count do not match, a required schedule is missing for the plan-characteristic codes given, a fully-insured indicator conflicts with the absence of a Schedule A. Rejections do not count as filings; the date that matters is the date EFAST2 accepts the submission. A rejected filing sent on 31 July is not on time if the corrected version is accepted on 1 August.

Filings that are not 5500-EZ become public. The DOL publishes the 5500 dataset on its EFAST2 website; tools such as the FreeERISA database and FormERISA index every filing. A plan's investment lineup, asset balance, and service-provider compensation are visible to anyone who looks. That is by design under ERISA's transparency mandate. Plan sponsors who would rather not have this be public should at least be aware that it is.

The Deadline: 31 July and the Form 5558 Extension

The standard due date for a Form 5500 is the last day of the seventh month after the plan year ends. For a calendar-year plan, that is 31 July. A non-calendar plan year shifts the deadline accordingly: a plan with a 30 June year-end is due 31 January.

Most plans take the extension. Form 5558, Application for Extension of Time to File Certain Employee Plan Returns, grants a one-time, no-questions-asked 2.5-month extension that moves the calendar-year deadline from 31 July to 15 October. The catch is procedural: Form 5558 has to be filed by the original due date (31 July for a calendar plan); a 5558 filed on 1 August does not extend anything. The 5558 is filed on paper by mail to the IRS at the address in the form instructions, with a copy retained by the plan administrator; it is not filed through EFAST2.

If the plan sponsor's corporate return is on extension (Form 7004 for entity returns), some plans get an automatic extension that lines up with that, but for most plans the 5558 is the route.

Late and Missed Filings: The DFVCP Lifeline

The penalties for missing a 5500 deadline without an extension are large. The IRS may assess up to $250 per day, capped at $150,000 per filing. The DOL may assess up to (a number that adjusts annually for inflation) roughly $2,739 per day, with no cap. For a plan that simply forgot to file, these numbers can accumulate fast.

The Department of Labor's Delinquent Filer Voluntary Compliance Program (DFVCP) is the off-ramp. A plan that comes forward voluntarily, before the DOL has sent notice that the filing is delinquent, can resolve the DOL penalty for a fixed and capped amount. Current DFVCP rates are roughly $10 per day to a maximum of $750 per filing for small plans (under 100 participants) and $10 per day to a maximum of $2,000 per filing for large plans (100 or more participants). There is also a per-plan cap that limits the total across multiple delinquent years.

DFVCP also satisfies the IRS penalty for the late filing, by interagency agreement: if you complete the DFVCP filing correctly, the IRS does not separately assess its own penalty for the same year. The filing happens on EFAST2 just like a normal 5500, with a DFVCP indicator selected, and the penalty is paid online by credit card or electronic transfer. The whole process is structured to make catching up cheap, on the theory that a low-friction off-ramp gets more late filings into the system than a high-stakes one.

For an employer that discovers a missed 5500 two or three years in, the math is essentially: DFVCP costs a few thousand dollars and ends the exposure; doing nothing and waiting for the DOL to notice is open-ended six-figure liability per year. The decision is mostly a process question (who actually files it, the TPA or the sponsor) rather than a strategic one.

The Actuary, the Auditor, and the Plan Administrator: Who Signs What

The 5500 is signed by the plan administrator, which for ERISA purposes is the entity named in the plan document (often the employer itself, or a designated administrator committee, or a third-party administrator). The signature is electronic, applied through EFAST2 with the administrator's filing credentials. There is no paper signature page; if the administrator dictates a signature to a TPA, the TPA cannot sign on the administrator's behalf without using the administrator's own EFAST2 credentials with permission.

Defined benefit plans add the enrolled actuary. An enrolled actuary, credentialed by the Joint Board for the Enrollment of Actuaries, signs Schedule SB (single-employer) or Schedule MB (multiemployer) and certifies the funding numbers. The actuary's signature is a professional attestation; the plan sponsor is not signing the SB itself, the actuary is, although the plan sponsor signs the 5500 it attaches to. For a small-employer cash balance plan, the actuary fee plus the SB preparation usually runs $2,000-$5,000 a year on top of recordkeeping.

Large plans add the independent qualified public accountant, the auditor, who issues the opinion attached to Schedule H. The auditor's report is the most expensive and visible piece of the filing, and the part most likely to generate "limited scope" certifications (where the auditor relies on a regulated-institution certification of participant-level investment values rather than auditing them directly, a route that has been narrowed in recent years).

The plan administrator coordinates these signers. A clean filing for a large 401(k) typically means: the TPA prepares the form and schedules, the auditor finishes the IQPA opinion in time for the 15 October extended deadline, the actuary (if it is also a defined benefit plan) signs the SB, the administrator signs the 5500 on EFAST2, and the filing transmits. Most of the friction is timing, the auditor delivering the opinion before the deadline, not legal complexity.

How the Form 5500 Sits Next to the Payroll-Tax Pillar

For a business reading this, the 5500 lives in a different lane from the federal payroll forms most HR teams handle directly. The employer files Form 941 quarterly for income-tax withholding and FICA. Form 940 annually for FUTA. W-2s annually to each employee plus a W-3 transmittal. 1099-NEC and 1099-MISC annually for non-employee compensation and other reportable payments. Form 5500 annually for the benefit plan itself.

The 5500 is not a payroll-tax filing and is not an income-tax filing. It is the ERISA disclosure return: the document that tells the federal government (and, for most filings, the public) what is happening inside an employer-sponsored benefit plan. Filing it is a duty of the plan administrator under ERISA, separate from the employer's payroll-tax duties under the Internal Revenue Code, even when the same person inside the company is doing both jobs.

A practical workflow for a mid-size employer running, say, a 401(k) and a fully-insured group medical plan:

- Calendar the plan year. For most employer plans, this is the calendar year, so 31 July is the date that matters.

- Decide variant in advance. Count participants at the start of the year. If under 100 and SF-eligible, plan to file 5500-SF. If 100+ or holding hard-to-value assets, plan to file the full 5500.

- Arrange the audit if needed. Engage an IQPA early; mid-size plan audits in spring are easier to scope than in September.

- File Form 5558 by 31 July. Buys time for the audit and the actuary; almost everyone takes it.

- Coordinate the schedules. Schedule A from the insurer, Schedule C compensation data from the recordkeeper, Schedule H from the TPA with IQPA opinion, Schedule R, Schedule SB if defined benefit.

- Sign and submit on EFAST2 by 15 October. The plan administrator signs with EFAST2 credentials.

- Retain the filing and the attachments for at least six years; longer for participant-related records under ERISA section 107.

A short structured intake from the plan sponsor to the TPA at the start of each filing cycle (plan-year confirmation, participant counts at start and end of year, contribution totals, distribution summary, fidelity bond information, insurance contract counts, service-provider list) makes the whole thing run faster. The Good Form 5500 intake template captures exactly those fields in one pass, so the TPA has everything they need before the 31 July clock starts.

The Short Version

Form 5500 is the annual ERISA return filed for an employer-sponsored employee benefit plan: pension plans (401(k), profit-sharing, defined benefit) and most welfare plans (medical, disability, life) above the small-plan exemption. The variant call is the first decision: 5500-EZ for one-participant owner-only plans (and only when assets exceed $250,000 at year-end), 5500-SF for small plans meeting all short-form conditions, 5500 (the full form) for everyone else. The schedule map is the substance: Schedule A for insured contracts, Schedule C for service-provider compensation (large plans), Schedule H for large-plan financials with an attached IQPA audit opinion, Schedule I for small-plan financials, Schedule R for retirement plan information, Schedule SB or MB for defined benefit plan actuarial information. The 100-participant count at the start of the plan year is the gate that drives both the variant and the audit requirement, with the 80/120 rule giving plans that hover around the line one year of grace. Calendar-year plans file by 31 July; Form 5558 buys a 2.5-month extension to 15 October if filed by the original date. The whole filing goes through EFAST2 electronically; the plan administrator signs with EFAST2 credentials, the actuary signs Schedule SB or MB, and the IQPA opinion attaches to Schedule H. Late filings that come forward through the DFVCP cap the DOL penalty at $750 (small plans) or $2,000 (large plans) and resolve the IRS penalty for the same year. Sponsors who want a clean intake of the plan-year data the TPA needs before the deadline can clone the Good Form 5500 intake template and start documenting their plan for this filing cycle today.