The 1099-MISC form is how a business reports the miscellaneous payments it made during the year that are not wages and not pay for a contractor's services: rent, royalties, prizes, medical payments, and the gross proceeds of a settlement paid to an attorney. If you paid $600 or more of rent, $10 or more of royalties, or $600 or more of most other reportable categories in the course of your trade or business, the 1099-MISC is the statement you send the recipient and file with the IRS. It is not a form the recipient fills in. It is your report, and the recipient uses it to complete their own return.

This is the 2026 walkthrough of the 1099-MISC form for the payer who has to file it: what is a 1099-MISC after the 2020 split that moved nonemployee compensation onto its own form, the box-by-box breakdown, the 1099-MISC vs 1099-NEC decision that trips up most filers, the $600 and $10 thresholds, and the furnishing and e-filing deadlines. If you want a clean way to capture each payment before your filing vendor needs it, clone the Good Form 1099-MISC intake template before year-end.

The short version:

- Form 1099-MISC, Miscellaneous Information, is filed by the payer for each recipient paid reportable miscellaneous income in the course of business. The recipient gets a copy; the IRS gets a copy.

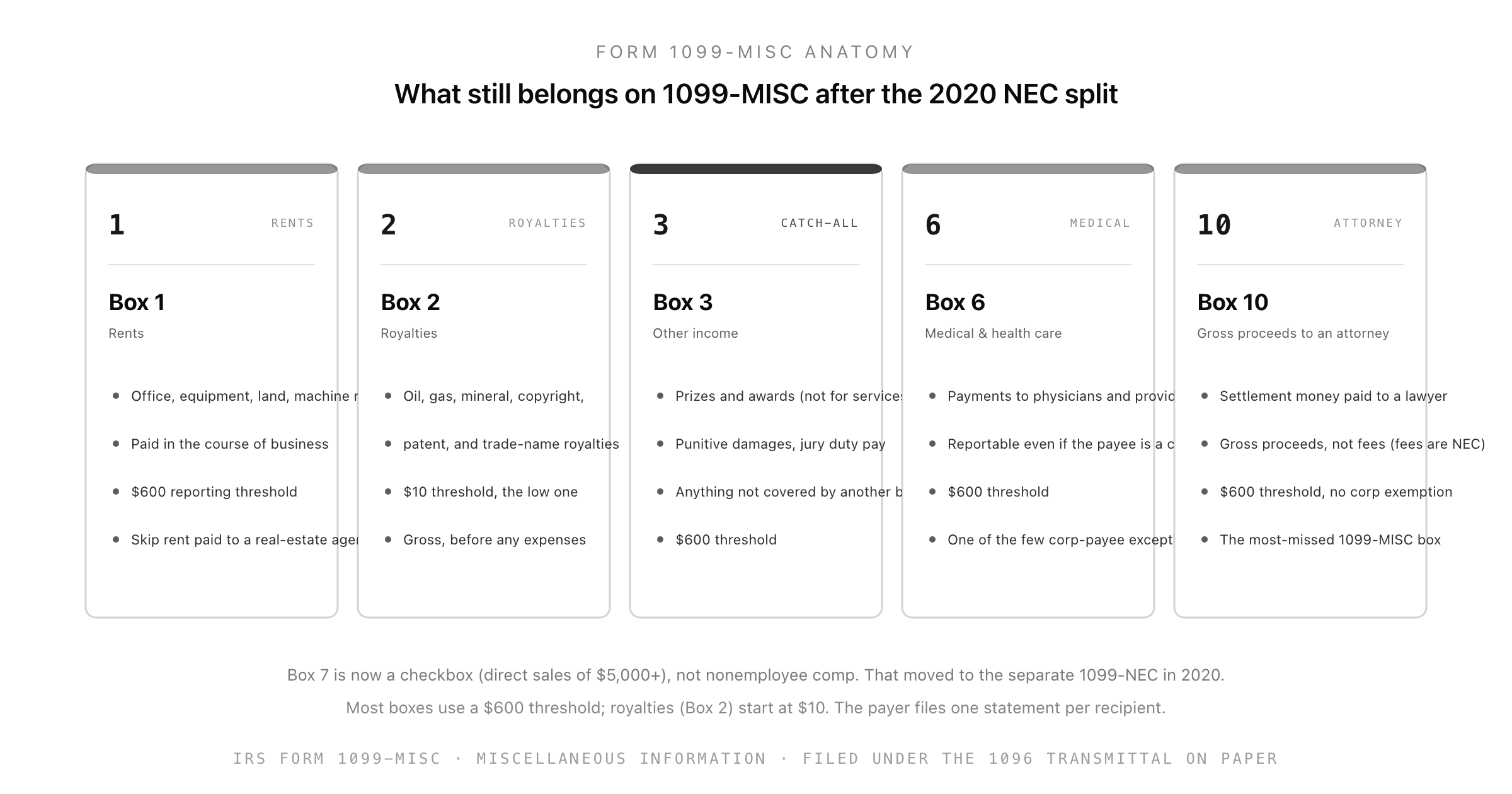

- In 2020 the IRS pulled nonemployee compensation out of the old Box 7 and put it on the revived 1099-NEC. The 1099-MISC kept everything else and renumbered its boxes.

- Box 1 is rents, Box 2 is royalties, Box 3 is other income (the catch-all), Box 6 is medical and health care payments, and Box 10 is gross proceeds paid to an attorney.

- The general threshold is $600. Royalties (Box 2) start at $10, the lowest threshold on the form.

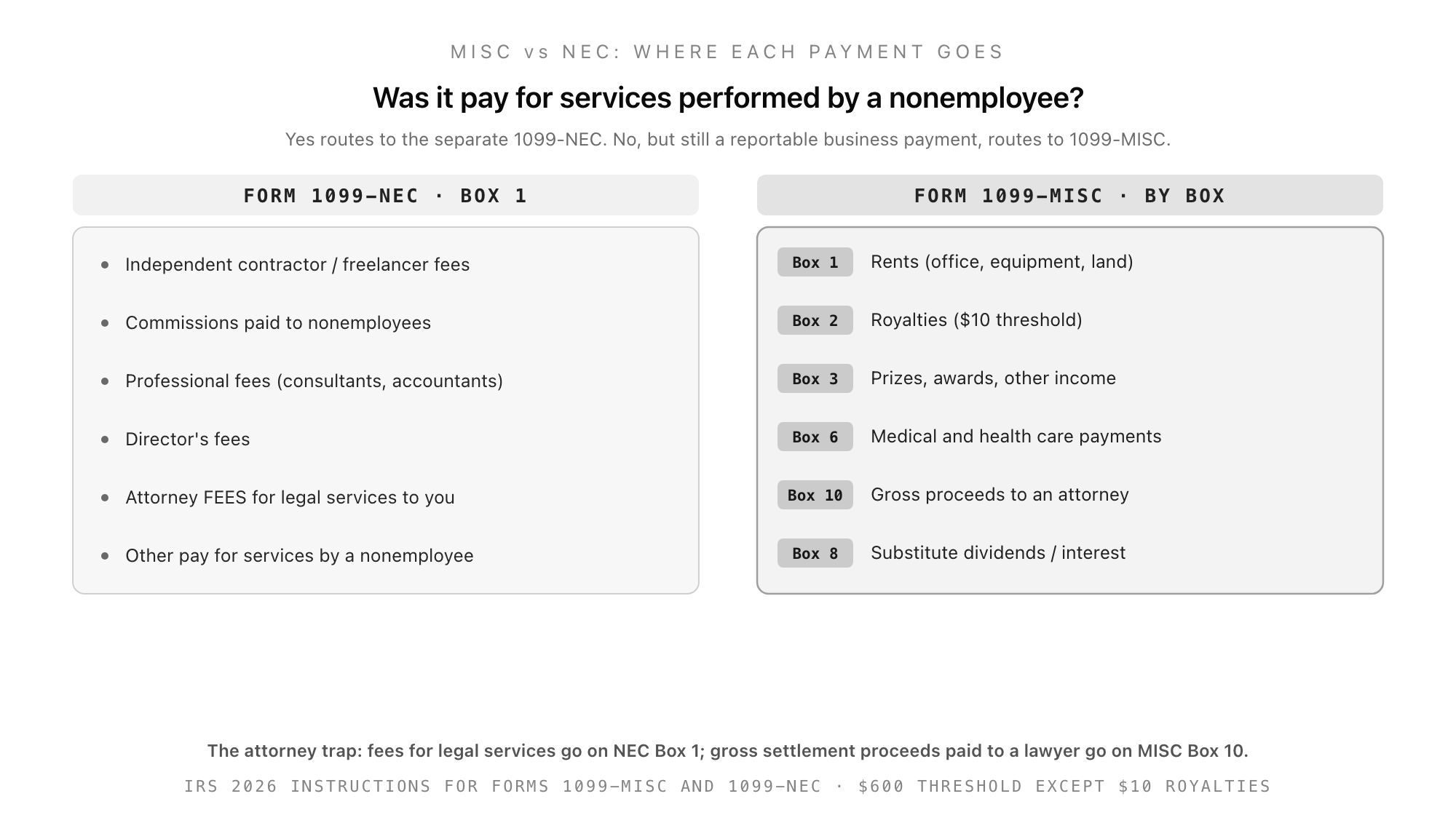

- MISC vs NEC turns on one question: was it pay for services performed by a nonemployee? If yes, it is a 1099-NEC. If it is rent, royalties, other income, or a settlement, it is a 1099-MISC.

- The attorney trap: legal fees for services go on 1099-NEC Box 1; the gross proceeds of a settlement paid to a lawyer go on 1099-MISC Box 10.

- Box 6 and Box 10 have no corporation exemption. You still report medical payments and attorney proceeds even when the payee is incorporated, which is the exception to the usual skip-corporations rule.

- Box 7 is now a checkbox for direct sales of $5,000 or more of consumer products for resale. It no longer carries a dollar amount.

- Deadlines: furnish the recipient copy by January 31; file with the IRS by February 28 on paper or March 31 electronically. E-filing is mandatory once you file 10 or more information returns of any type in aggregate.

What the 1099-MISC Form Is and Who Files It

Form 1099-MISC, retitled "Miscellaneous Information" in 2020 (it was "Miscellaneous Income" for decades), is an information return. It reports specific categories of payment a business made during the year so the IRS can match those payments against the income the recipient reports. It covers the odds and ends of business payments that do not fit on a W-2 and are not pay for a nonemployee's services.

The payer files it. That is the business that made the payment in the course of its trade or business. Personal payments do not count: if you pay a neighbour to mow your lawn, there is no 1099-MISC, because it was not a business payment. The recipient does nothing with the form except keep it and copy the figures onto their own return. The 1099-MISC has two audiences: the recipient, who needs it to file, and the IRS, which matches it against what the recipient reports.

To file it correctly you need the recipient's taxpayer identification number, which you collect on a Form W-9 before you pay. If the recipient will not certify a TIN, you may have to take 24% backup withholding out of the payment and report it in Box 4. Soliciting the W-9 up front is the single best way to avoid that problem, because chasing a TIN in January after the work is done rarely goes well.

What Changed in 2020: the NEC Split

For decades, the most common reason a business filed a 1099-MISC was to report what it paid an independent contractor. That money sat in the old Box 7, Nonemployee compensation. In 2020 the IRS revived a separate form, the 1099-NEC, and moved nonemployee compensation onto it. The reason was a deadline mismatch: nonemployee compensation had an earlier filing deadline than the rest of the 1099-MISC boxes, and stuffing two deadlines onto one form caused years of penalty notices.

So the modern division is simple. Pay for a nonemployee's services goes on the 1099-NEC. Everything else that used to be miscellaneous income stays on the 1099-MISC, with the boxes renumbered. The old Box 7 is now just a checkbox for direct sales. If you have read our guide to the 1099-NEC and the contractor-vs-employee test, this is the other half of that story: the two forms are siblings, and most payers who file one also file the other.

The Boxes That Matter: A 1099-MISC Walkthrough

The 1099-MISC has eighteen numbered boxes, but most payers only ever touch a handful. Here are the ones that carry real reporting weight.

Box 1: Rents

Box 1 reports rent of $600 or more paid in the course of business: office space, warehouse space, equipment rental, machine rental, and land. If your business leases its premises and pays the landlord directly, that rent goes in Box 1. The main exception is rent paid to a real-estate agent or property manager, who passes it on to the owner. In that case you do not file; the agent handles the reporting to the owner.

Box 2: Royalties

Box 2 reports royalties of $10 or more. This is the lowest threshold on the form, far below the usual $600, because royalty streams are easy to under-report. It covers oil, gas, and mineral royalties; and intangible royalties on copyrights, patents, trade names, and similar property. The figure is gross, before any expenses or severance taxes are netted out. A small-press publisher paying an author, or an app developer paying a licensor, is the typical Box 2 filer.

Box 3: Other Income

Box 3 is the catch-all, which is why 1099-misc box 3 and 1099-misc other income are such common searches. It captures reportable payments of $600 or more that do not belong in any other box: prizes and awards that are not for services, punitive damages, certain payments from lawsuits, jury duty pay turned over to an employer, and other miscellaneous income. If a payment is clearly reportable and clearly business-related but does not match a more specific box, Box 3 is usually where it lands. When in doubt, read the box descriptions in order; Box 3 is the fallback, not the first choice.

Box 6: Medical and Health Care Payments

Box 6 reports payments of $600 or more to physicians, suppliers, or providers of medical and health care services, made in the course of business. A business that pays a clinic for employee physicals, or an insurer that pays a provider, reports here. Box 6 carries an important quirk: it applies even when the payee is a corporation. The usual rule that you skip corporations on 1099s does not apply to medical payments, so a payment to an incorporated medical practice is still reportable.

Box 10: Gross Proceeds Paid to an Attorney

Box 10 is the most-missed box on the entire form, and the one that causes the most confusion. It reports gross proceeds of $600 or more paid to an attorney in connection with legal services, typically a settlement. The key word is gross proceeds, not fees. If your business settles a claim and writes a cheque to the claimant's lawyer for the full settlement amount, that full amount goes in Box 10. Like Box 6, Box 10 has no corporation exemption: you report it even though almost every law firm is incorporated.

The single most important MISC-vs-NEC distinction lives right here. Attorney fees for legal services rendered to your business (the lawyer billed you to handle a contract) go on the 1099-NEC, Box 1. Gross settlement proceeds paid to a lawyer on behalf of a third party go on the 1099-MISC, Box 10. Same payee, two different forms, depending on what the money was for.

Box 4 and Box 7: Withholding and the Direct-Sales Checkbox

Box 4 reports federal income tax withheld, which on a 1099-MISC almost always means 24% backup withholding taken because the recipient never gave you a certified TIN. Box 7 is now a checkbox, not a dollar field: you check it if you made direct sales of $5,000 or more of consumer products to the recipient for resale. The amount of those sales is reported elsewhere or not at all; Box 7 just flags that the relationship exists.

1099-MISC vs 1099-NEC: the Decision That Trips Everyone Up

The most common 1099-MISC mistake in 2026 is filing one when you should have filed a 1099-NEC, or the reverse. The two forms look almost identical and many accounting systems still default to "1099-MISC" out of habit from the pre-2020 era. The test is one question.

Was the payment for services performed by a nonemployee in your trade or business?

- Yes. It is nonemployee compensation, and it goes on the 1099-NEC. Contractor and freelancer fees, commissions to nonemployees, consultant and accountant fees, director's fees, and attorney fees for legal work all fall here.

- No, but it is still a reportable business payment. It goes on the 1099-MISC, in the box that matches the type: rent, royalties, prizes, medical payments, or attorney settlement proceeds.

If a worker should really have been on a W-2 in the first place, neither 1099 is correct. The contractor-vs-employee question sits upstream of both forms, and getting it wrong exposes the payer (not the worker) to misclassification penalties. Our guide to the 1099 contractor rules walks through the three-prong IRS test for that call.

Thresholds, Deadlines, and E-Filing

The general reporting threshold for the 1099-MISC is $600. The one exception is royalties (Box 2), which start at $10. Below those thresholds, no 1099-MISC is required, though you can still file one and many payers do for their own records.

The deadlines for 2026 reporting are:

- Furnish the recipient copy by January 31. The person you paid needs the form in time to file their own return.

- File with the IRS by February 28 on paper, accompanied by a Form 1096 transmittal if you are filing paper returns.

- File with the IRS by March 31 if you file electronically. The extra month is the reward for e-filing.

Note that the 1099-MISC deadlines are later than the 1099-NEC, which is due to both the recipient and the IRS by January 31 with no paper-versus-electronic split. That deadline gap is the entire reason the two forms were separated in 2020, and it is why filing the wrong one can trigger a late-filing penalty even when the money was reported.

Electronic filing is mandatory once you file 10 or more information returns of any type in aggregate. That aggregate count combines your 1099-MISC, 1099-NEC, W-2, 1099-R, and every other information return into a single total. Most businesses cross the 10-return line easily, so for practical purposes nearly everyone e-files through the IRS IRIS or FIRE system or a third-party provider.

Common 1099-MISC Mistakes to Avoid

A few errors account for most of the corrected returns and penalty notices:

- Filing MISC for contractor pay. The biggest one. Nonemployee compensation has belonged on the 1099-NEC since 2020. If you paid a freelancer for services, it is not a 1099-MISC.

- Putting attorney fees in Box 10. Box 10 is for gross settlement proceeds. Fees for legal services rendered to you are nonemployee compensation on the 1099-NEC.

- Skipping incorporated payees on medical and attorney payments. Box 6 and Box 10 override the usual skip-corporations rule. Report them even when the payee is a corporation.

- Missing the $10 royalty threshold. Box 2 starts at $10, not $600. A small royalty still triggers a filing requirement.

- Collecting the TIN too late. Solicit the W-9 before you pay. Without a certified TIN you face 24% backup withholding and a scramble in January.

Capture Each Payment Before Filing Season

The 1099-MISC itself is filed through the IRS or a provider, but the work that makes filing painless happens long before the deadline: collecting the recipient's W-9, recording which box each payment belongs in, and flagging the MISC-vs-NEC calls while the payment is fresh rather than reconstructing them in January.

Good Form gives you a clean, shareable intake for exactly that. Our 1099-MISC intake template captures the payer and recipient identification, the payment type, and the box-by-box amounts, and it flags the common case where a payment is really nonemployee compensation that belongs on a 1099-NEC. Send it to your accounts-payable contact or to the recipient, collect structured answers, and hand a clean record to whoever files the return. Start with Good Form for free and build your year-end information-return workflow before the deadline finds you.