The Form 1099-K is the statement a payment processor sends to a payee, and files with the IRS, to report the gross amount of payments it settled for that payee during the year through payment cards or a third-party network. If you took card payments through a processor, or got paid through PayPal, Venmo, Stripe, Etsy, eBay, or any similar platform, the 1099-K is how those platforms tell the IRS how much money flowed to you. It is not a form you fill in, and it is not a tax bill. It is a gross-receipts report filed by the payment company, and the single biggest mistake people make is reading the Box 1a figure as taxable income.

This is the 2026 walkthrough of the form 1099-K for the person who receives one and the business that has to make sense of it: what the form does, who actually issues it, the box-by-box breakdown, the reporting threshold that whipsawed from $20,000 down toward $600 and then snapped back to $20,000 under the One Big Beautiful Bill, the overlap with the 1099-NEC that can get the same dollar reported twice, and what to do when a 1099-K shows up for money that was never income at all. If you run payments through a platform and want a clean way to capture each payee's details before reconciling at year-end, clone the Good Form 1099-K intake template.

The short version:

- Form 1099-K, Payment Card and Third Party Network Transactions, is filed by a payment settlement entity (a payment card company or a third-party settlement organization like PayPal, Venmo, Stripe, or eBay), not by the payee and not by the customer.

- Box 1a is gross. It is the total of all payments the platform settled, before fees, refunds, chargebacks, or adjustments. It is almost always larger than your actual income, and it is a starting point, not the taxable number.

- The threshold whipsawed. The American Rescue Plan dropped the trigger to $600 with no transaction minimum. The IRS delayed it for years, then the One Big Beautiful Bill (signed July 4, 2025) repealed the $600 rule and restored the old $20,000 and more than 200 transactions threshold, retroactive to 2022.

- Below the threshold is not tax-free. A platform may still issue a 1099-K voluntarily or under a stricter state rule, and all income is taxable whether or not a 1099-K is issued.

- 1099-K vs 1099-NEC can double-count. If a client pays you by card or app and also files a 1099-NEC for the same money, the income can appear on both forms. You report it once and reconcile so the IRS matching does not flag a shortfall.

- Personal payments get caught by mistake. Splitting rent, repaying a friend, or selling a used couch at a loss can land on a 1099-K. There is a defined way to back it out on Schedule 1 so you are not taxed on a gift or a loss.

- The monthly boxes (5a to 5l) break the gross down by month, and Box 4 carries any backup withholding (24% when a TIN is missing or flagged).

- Paper filers transmit the 1099-K with a Form 1096 summary, the same transmittal that covers the rest of the 1099 family.

What the Form 1099-K Is and Who Issues It

Form 1099-K reports the gross dollar amount of reportable payment transactions that a payment settlement entity processed for a payee in a calendar year. The title on the form is "Payment Card and Third Party Network Transactions," and those two phrases describe exactly the two kinds of money it covers.

Payment card transactions are payments settled through a payment card: credit cards, debit cards, and stored-value cards. The entity that files here is the payment card company or the merchant acquirer that settles the card charges into your bank account.

Third-party network transactions are payments settled through a third-party payment network, which is where the apps live. A third-party settlement organization (TPSO) is a platform that sits between a lot of buyers and a lot of sellers and settles the money: PayPal, Venmo (for goods and services), Stripe, Square, Etsy, eBay, Airbnb, Uber, and the rest. When you search 1099-k paypal or 1099-k ebay, this is the box you are in, the TPSO box.

The crucial point is who does not file it. The recipient never prepares a 1099-K. The customer who paid you never prepares one. It is always the payment company. The recipient's only job is to take the numbers, understand them, and reconcile them against their own books.

Box by Box: Reading the 1099-K

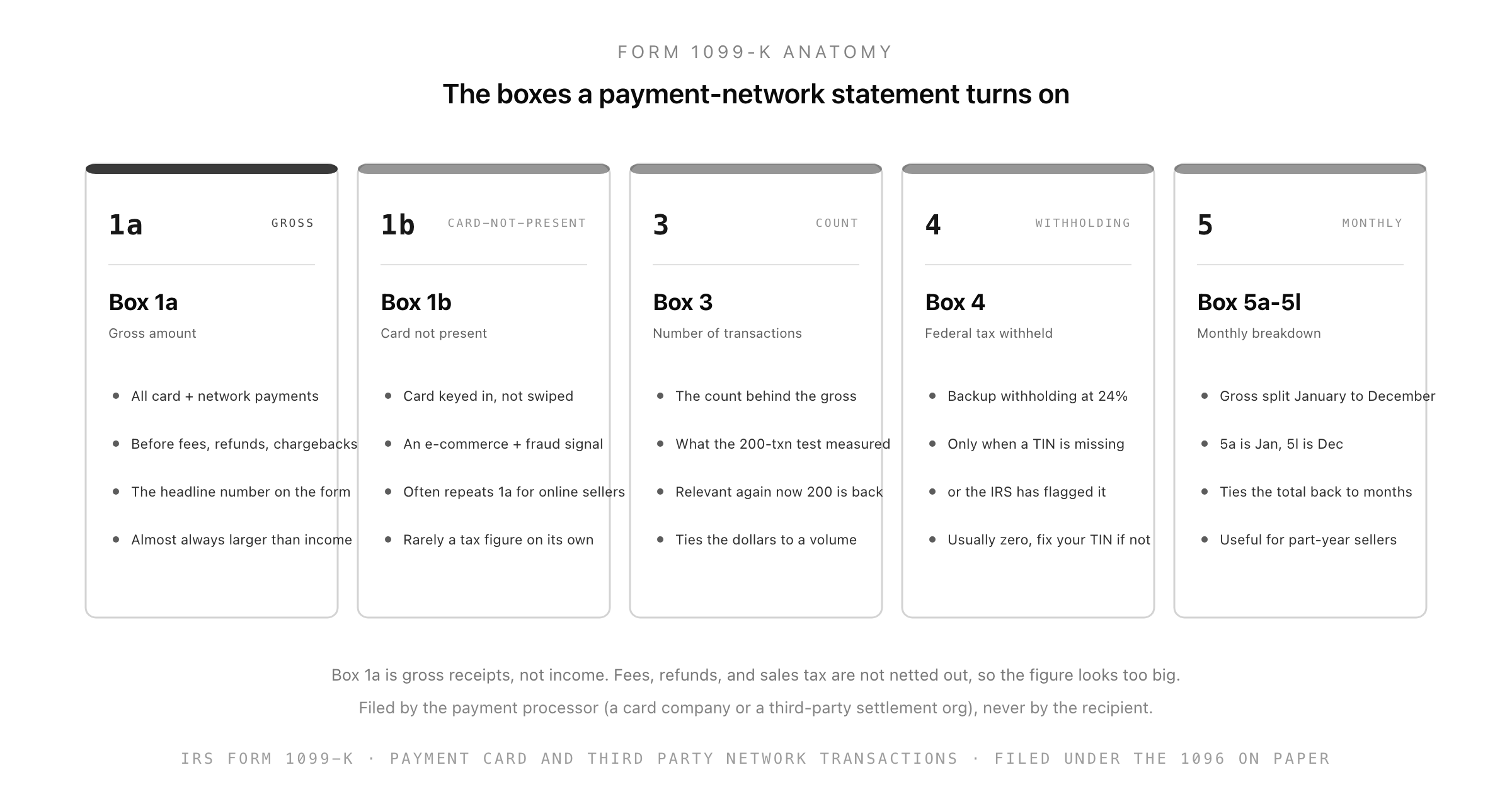

The 1099-K has fewer moving parts than the 1099-MISC or the 1099-R, but the boxes are easy to misread because the headline number is gross.

Box 1a, Gross amount of payment card / third party network transactions, is the total dollar amount the platform settled for you in the year, before anything is netted out. Fees the platform charged you, refunds you issued, chargebacks, sales tax it collected on your behalf, shipping it billed: none of that is subtracted. This is why a seller who actually cleared $30,000 can see a Box 1a of $42,000. The gross is correct from the platform's point of view, and it is your job to bridge from gross to net on your return.

Box 1b, Card not present transactions, is the portion of Box 1a where the card number was keyed in rather than physically swiped or tapped. It is an e-commerce and fraud signal more than a tax figure, and most online sellers will see most or all of Box 1a repeated here.

Box 2, Merchant category code (MCC), is the four-digit code that classifies the type of business. It comes from the card networks and you rarely need to do anything with it.

Box 3, Number of payment transactions, is the count of payments behind the Box 1a gross. This is the number the old "more than 200 transactions" test was measured against, which makes it suddenly relevant again now that the 200-transaction threshold is back (more on that below).

Box 4, Federal income tax withheld, is backup withholding, normally zero. A platform withholds at 24% only when it does not have a valid taxpayer identification number for you, or the IRS has flagged the one it has. If you ever see a number here, fix your TIN on file with the platform, because that money was held back from your payouts.

Boxes 5a through 5l, the monthly breakdown, split the annual gross across the twelve months, January in 5a through December in 5l. They let you and the IRS tie the total back to specific months, which is useful for a business that started or stopped mid-year or that needs to reconcile against monthly statements.

Boxes 6, 7, and 8 carry the state, the state identification number, and any state income tax withheld, for platforms reporting to a state as well as the IRS.

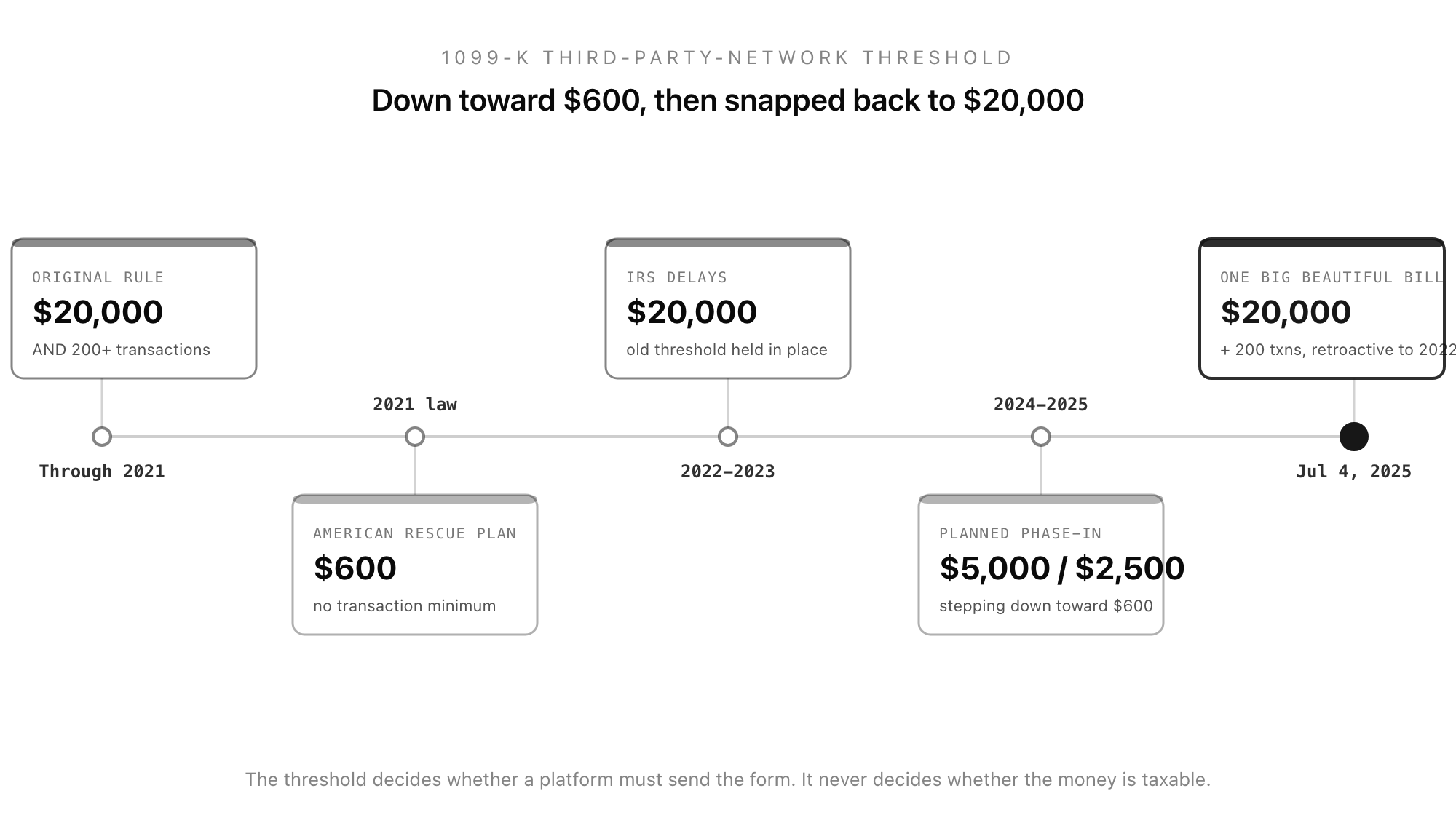

The Threshold Whiplash: $20,000, Then $600, Then Back to $20,000

No part of the 1099-K has caused more confusion than the 1099-k threshold, because it changed by law, then got delayed by the IRS for several years running, then changed back. Here is the actual sequence, because the headlines from 2022 through 2024 are now out of date.

The original rule. For years, a TPSO only had to file a 1099-K once a payee crossed both $20,000 in gross payments and more than 200 transactions in the year. Both tests had to be met, so a low-volume seller with high-value items, or a high-volume seller of cheap items, often stayed under it. (Payment card transactions, the Box 1a card side, never had this de minimis floor; a single dollar of card settlement is reportable.)

The American Rescue Plan change. In 2021, Congress lowered the third-party-network trigger to $600 with no transaction minimum, the same $600 floor used by the 1099-NEC. On paper this took effect for the 2022 tax year and would have pulled tens of millions of casual sellers and side-giggers into 1099-K reporting for the first time.

The IRS delays. Facing the prospect of a flood of forms going to people who had no taxable income to report, the IRS postponed the $600 rule repeatedly. It treated 2022 and 2023 as transition years that kept the old $20,000 / 200 threshold, then announced a phase-in: a $5,000 threshold for 2024 and a planned $2,500 for 2025 on the way down to $600.

The One Big Beautiful Bill reversal. Then the law changed again. The One Big Beautiful Bill Act, signed on July 4, 2025, repealed the $600 threshold entirely and restored the original $20,000 and more than 200 transactions test, retroactive to 2022. The IRS has confirmed in updated FAQs that the dollar limit reverts to $20,000. In practice this means the phase-in numbers you may have read about ($5,000, then $2,500) were overtaken by the new law, and the threshold for third-party-network reporting is back where it started: both $20,000 and more than 200 transactions must be met before a TPSO is required to file.

Two things still matter even with the higher threshold restored:

- A platform can issue a 1099-K below the threshold. Some do it voluntarily, and some states set their own lower thresholds (Maryland, Massachusetts, Vermont, Virginia, and others have used a $600 state trigger). So you may still receive one even when the federal rule would not require it.

- The threshold governs the form, not the tax. This is the part people miss. The $20,000 line decides whether a platform has to send you a piece of paper. It does not decide whether the money is taxable. All income is taxable whether or not a 1099-K is issued. Falling under the threshold is a paperwork break, not a tax break.

1099-K vs 1099-NEC: The Double-Report Trap

The most expensive 1099-K mistake is letting the same income get counted twice. Here is how it happens.

Say a client pays you $8,000 for freelance work, and they pay it by credit card or through a platform. Two reporting paths can fire on that one payment:

- The payment processor may report it on a 1099-K (if you cross the threshold), because it settled the card or app payment.

- The client may also file a 1099-NEC, because from their side they paid a nonemployee $600 or more for services.

Now the IRS has two information returns describing what was really one $8,000 payment. If you report the $8,000 once on your Schedule C (which is correct), the IRS matching system can see $8,000 of NEC plus $8,000 of K and wonder why you only reported $8,000.

The rule that is supposed to prevent this: a payer is not meant to file a 1099-NEC for a payment that was made by payment card or through a third-party network, precisely because the processor's 1099-K already covers it. The IRS instructions tell businesses to exclude card and app payments from the amounts they put on a 1099-NEC. But plenty of payers do not follow that rule, especially small ones running the numbers out of their accounting software.

How to handle it: report the income once, based on your own books, not by adding up every form you received. Keep a reconciliation that shows the overlap: this $8,000 appears on both the 1099-NEC from the client and the 1099-K from the processor, and it is the same money. If the IRS sends a matching notice (a CP2000), your reconciliation is the answer. The difference between 1099-k vs 1099-nec is not which one is right; it is that they can describe the same dollars, and you account for those dollars one time.

Personal Payments Reported by Mistake

Because apps like Venmo and PayPal handle both business and personal money, a 1099-K can capture payments that were never income: your share of a group dinner, a roommate's half of the rent, a friend repaying a loan, or the sale of a personal item at a loss.

Two protections matter here:

- Goods and services vs friends and family. On most apps, a payment marked "friends and family" is not a reportable third-party-network transaction, while a "goods and services" payment is. If personal money keeps landing in the reportable bucket, the fix is usually how the payments are being tagged.

- The Schedule 1 back-out. If a 1099-K reports an amount that is not taxable income, the IRS has a defined way to remove it so you are not taxed on it. You report the 1099-K amount on Schedule 1, line 8z ("Other income") and then subtract the same amount on Schedule 1, line 24z as an adjustment, with a description like "Form 1099-K received in error" or "personal item sold at a loss." The two entries net to zero, the IRS sees that you accounted for the form, and nothing is taxed.

The one thing you should not do is ignore a 1099-K because you know the money was not income. The IRS received a copy; if you leave it off your return entirely, the matching system has nothing to reconcile against, and that is what triggers a notice.

How a Payer Files It, and the 1096 Transmittal

If you are on the filing side (a platform, a marketplace, or a processor settling payments for others), the 1099-K follows the same filing mechanics as the rest of the family. You furnish the recipient copy by January 31, and you file with the IRS by February 28 on paper or March 31 electronically. Electronic filing is mandatory once you file 10 or more information returns of any type in aggregate across the year, a low bar that catches almost every real platform.

Paper filers attach a Form 1096, the Annual Summary and Transmittal of U.S. Information Returns, which totals the 1099-Ks being submitted in that batch. Electronic filers go through the IRS IRIS or FIRE system and do not use a 1096. The recipient TIN you report has to be correct, which is why collecting a clean Form W-9 from each payee before you ever settle a payment saves a backup-withholding headache later.

Capture the Details Cleanly Before Year-End

Whether you are a platform preparing 1099-Ks or a business trying to reconcile the ones you receive, the work is the same underneath: you need each payee's legal name, TIN, address, and a clean record of gross settled, fees, and refunds so the Box 1a gross can be bridged to real income. Doing that in a spreadsheet at the end of January is how TINs go missing and backup withholding kicks in.

Good Form gives you a structured way to collect it up front. The 1099-K intake template captures the payer and payee details, the gross and net figures, the transaction count behind Box 3, and the goods-and-services-vs-personal flag that decides whether a payment is even reportable, so the data is clean before your filing vendor or your accountant needs it. It does not file the 1099-K for you; it makes sure that when filing time comes, nothing is missing. Start building your 1099-K intake form and get the gross-to-net reconciliation right from the first payment.