Form 2553 is the IRS Election by a Small Business Corporation, the single form a company files to be taxed as an S corporation. It does not create a business and it does not change what a business does. It changes one thing: how the entity's profit is taxed, by passing income, losses, and deductions through to the owners and, for an active owner, splitting that profit into a salaried portion that carries payroll tax and a distribution that does not. For a profitable single-owner business already running on an EIN from Form SS-4, the S-corp election filed on form 2553 is often the next deliberate tax decision, and the one with the largest dollar swing.

This guide is the 2026 walkthrough of form 2553 for a US small business: what the election actually does, the four eligibility tests an entity has to pass, the 2-months-15-days deadline that catches most filers, the late-election relief under Rev. Proc. 2013-30 that saves the ones who miss it, how the form differs from Form 8832, and the self-employment-tax math that explains why anyone bothers. The audience is founders who just formed an LLC or corporation, sole proprietors whose profit has grown past the point where flat self-employment tax stings, and the finance or operations lead handed the job of "go make us an S corp." If you want a clean intake that captures the legal name, EIN, effective date, shareholder consents, and reasonable-salary plan a 2553 depends on, clone the Good Form 2553 intake template.

The short version:

- Form 2553 is the Election by a Small Business Corporation. Filing it makes an eligible corporation or LLC taxed as an S corporation under Subchapter S of the tax code.

- The S election is a tax classification, not a legal entity. You still form an LLC or corporation with your state first; the 2553 only changes how the IRS taxes that existing entity.

- The point is the self-employment-tax split. An S-corp owner-employee takes a reasonable salary (which carries FICA) plus distributions (which do not), instead of paying self-employment tax on the entire profit.

- Four eligibility tests: a domestic eligible entity, only allowable shareholders (individuals, certain trusts, and estates, no partnerships or corporations or non-resident aliens), no more than 100 shareholders, and one class of stock.

- The deadline is no more than 2 months and 15 days after the start of the tax year the election is to take effect, or any time in the prior tax year. For a new entity, the clock starts at the earliest of getting shareholders, acquiring assets, or beginning business.

- Miss the deadline and Rev. Proc. 2013-30 usually still saves you: file within 3 years and 75 days of the intended date, write "FILED PURSUANT TO REV. PROC. 2013-30" at the top, and attach a reasonable-cause statement.

- An LLC electing S-corp status generally files only Form 2553, not Form 8832. The 2553 is treated as a deemed entity-classification election, so the separate 8832 is unnecessary.

- Form 8832 is for choosing C-corporation taxation (or reverting classification). Form 2553 is for choosing S-corporation taxation. They are different elections to different destinations.

- The reasonable-salary requirement is not optional. An S corp that zeroes out salary to dodge all payroll tax is the single most-audited S-corp position. Pay a defensible wage first, distribute the rest second.

What Form 2553 Is and Why It Exists

Form 2553, formally the Election by a Small Business Corporation, is the form an eligible business files to elect S-corporation tax treatment under Subchapter S of the Internal Revenue Code. The word "election" is the key one. The business is choosing, affirmatively and in writing, to be taxed under a different set of rules than its default. Nothing about the business's legal form, ownership, or operations changes. The IRS simply starts treating the entity as an S corporation for federal income-tax purposes from the effective date on the form forward.

The default tax treatments are what the 2553 overrides. A single-member LLC defaults to a disregarded entity, taxed as a sole proprietorship on the owner's personal return. A multi-member LLC defaults to a partnership. A corporation formed with the state defaults to a C corporation, taxed at the entity level and again on dividends. The S election sits on top of any of these eligible entities and replaces the default with pass-through taxation: the entity itself generally pays no federal income tax, and profit, loss, deductions, and credits flow through to the shareholders, who report them on their own returns.

The reason the election exists, and the reason a profitable owner files it, is the treatment of an active owner's earnings. Under the default sole-proprietor or partnership rules, an active owner pays self-employment tax (Social Security and Medicare, 15.3% up to the wage base and 2.9% above it) on essentially all of the business profit. Under S-corp rules, the owner becomes an employee, takes a reasonable salary that carries payroll tax, and receives the remaining profit as a distribution that does not. That single structural difference is what the rest of this guide circles around.

The Self-Employment-Tax Math Behind the Election

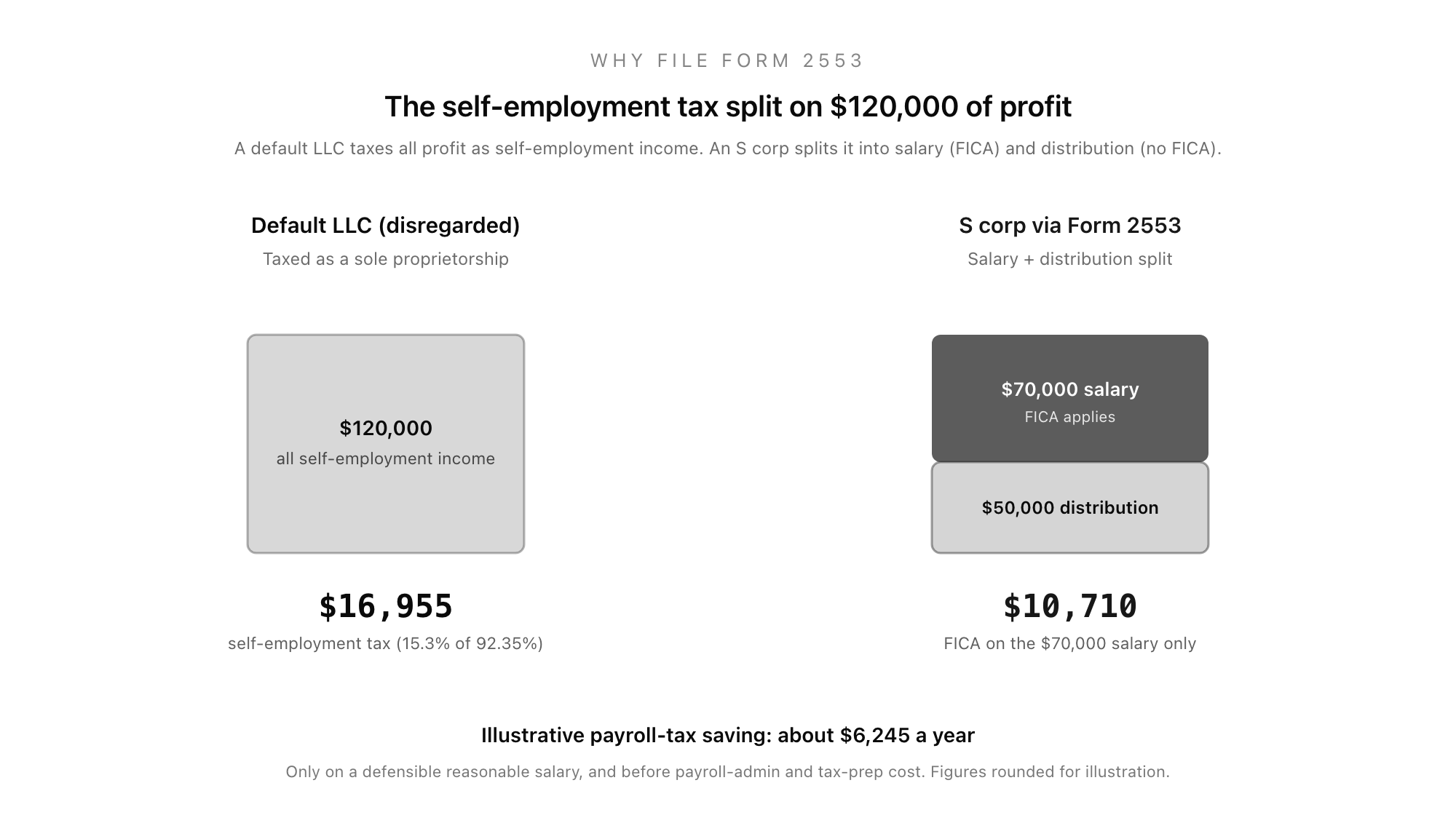

The clearest way to understand why anyone files form 2553 is to look at the same profit taxed two ways.

Take a single-owner business with $120,000 of net profit for the year. As a default LLC taxed as a sole proprietorship, the owner pays self-employment tax on 92.35% of that profit, which is $110,820, at 15.3%. That is roughly $16,955 in self-employment tax, on top of ordinary income tax.

Elect S-corp status, and the same owner becomes an employee of their own company. Suppose they pay themselves a reasonable salary of $70,000 for the work they actually do, and take the remaining $50,000 as a distribution. The $70,000 salary carries FICA (the employee and employer halves together, 15.3%), which is about $10,710. The $50,000 distribution carries no FICA at all. The payroll-tax bill drops from about $16,955 to about $10,710, a saving in the neighborhood of $6,245 for the year.

Two caveats keep this honest, and both matter. First, the figures are illustrative and rounded; the exact numbers depend on the wage base, the additional Medicare tax over $200,000, and the deductible half of self-employment tax. Second, and more importantly, the salary has to be reasonable. The saving comes entirely from the portion of profit you can defensibly call a distribution rather than wages, and the IRS scrutinizes S corps that pay an artificially low salary to shrink the FICA base. Set the salary to what you would have to pay someone else to do your job, document how you arrived at it, and the structure holds. Zero it out, and you have built the most common audit trigger in the S-corp world. There is also a real cost on the other side: running payroll, filing the quarterly Form 941, and preparing an 1120-S return all carry administrative and tax-prep expense that eats into the saving at lower profit levels. The election tends to make sense once profit is comfortably into five figures above a reasonable salary, not on the first dollar.

The Four Eligibility Tests

Not every business can elect S-corp status. The entity has to pass four tests, and an S election filed by an entity that fails any of them is invalid.

It must be a domestic eligible entity. That means a domestic corporation, or a domestic entity (most commonly an LLC) eligible to elect corporate treatment. Foreign entities cannot be S corporations.

It must have only allowable shareholders. Allowable shareholders are individuals, certain trusts, and estates. Specifically not allowed: partnerships, corporations, and non-resident alien shareholders. This is the test that quietly disqualifies a lot of structures, because the moment another company or a non-resident individual holds even a single share, the entity is ineligible.

It must have no more than 100 shareholders. Family members can be treated as a single shareholder for this count, which helps closely held businesses, but the ceiling is 100.

It must have only one class of stock. All shares must confer identical rights to distribution and liquidation proceeds. Differences in voting rights are allowed, but a true second economic class of stock (preferred shares with a different distribution priority, for example) breaks eligibility. For an LLC electing S-corp status, this is why the operating agreement matters: special allocations and disproportionate distributions that are perfectly normal in a partnership-taxed LLC will violate the one-class-of-stock rule once the S election is in place.

A handful of corporation types are also flatly ineligible regardless of the four tests, including certain financial institutions, insurance companies, and domestic international sales corporations. For the typical small business, the binding constraints are the shareholder-type test and the one-class-of-stock test.

The Filing Deadline

The deadline is where most form 2553 problems start. The election must be filed no more than 2 months and 15 days after the beginning of the tax year the election is to take effect, or at any time during the tax year that precedes it. Two months and 15 days is often rounded to "75 days" in conversation, but the statute is written as two months and 15 days, so count it on the calendar rather than as a flat 75.

For an existing calendar-year business that wants the election effective from January 1, that puts the deadline at March 15. Miss it, and absent relief, the election does not take effect until the following tax year.

For a brand-new entity, the clock does not start on January 1. It starts on the first day of the entity's first tax year, which is the earliest of three events: the date the entity first has shareholders, the date it first acquires assets, or the date it first begins doing business. New owners routinely misjudge this, assuming the deadline runs from the state formation date or from the date they got around to thinking about taxes. It runs from whichever of those three triggers happened first, and the 2-months-15-days window starts there.

The election is filed by mailing or faxing the completed 2553 to the IRS service center for the entity's state (the current addresses and fax numbers are in the form instructions). The IRS then sends back a CP261 notice confirming the S election was accepted, usually within about 60 days. Keep that acceptance letter; it is the proof the election is in place, and the document a future accountant or buyer will ask for.

Late-Election Relief Under Rev. Proc. 2013-30

Missing the deadline is common and, in most cases, fixable. Revenue Procedure 2013-30 provides a simplified path to late S-corporation election relief that does not require a private letter ruling (which is slow and expensive). It consolidated the older patchwork of relief procedures into one route, and it is the reason a missed March 15 is usually an inconvenience rather than a lost year.

To qualify, the entity generally has to meet a short list of conditions: it intended to be classified as an S corporation as of the intended effective date; it failed to qualify as an S corp solely because the 2553 was not filed on time; it has reasonable cause for the failure and acted diligently to correct it once discovered; and either it has filed returns consistent with S-corp status for the years in question, or those returns are not yet due. The relief has to be requested within 3 years and 75 days of the intended effective date.

Mechanically, you file the same Form 2553, but you write "FILED PURSUANT TO REV. PROC. 2013-30" across the top, and you attach a statement explaining the reasonable cause for the delay (and confirming the consistency of any returns already filed). The shareholders' consent statements have to cover the entire period from the intended effective date forward. When a late election is being made by an entity that also needs to be treated as a corporation in the first place (an LLC, most often), Part IV of the form captures the late corporate-classification representations that fold the entity-classification election into the same filing.

The practical lesson is to file on time, because relief is never guaranteed and a clean CP261 is worth more than a reasonable-cause argument. But if the deadline has already slipped, Rev. Proc. 2013-30 is the route, and it works far more often than panicked founders expect.

Form 2553 vs Form 8832: Which One You Actually File

The relationship between form 2553 and Form 8832 confuses almost everyone, because both are "elections" filed by LLCs that want to be taxed differently, and the internet is full of advice to file both. For most small businesses electing S-corp status, that advice is wrong.

Form 8832 is the Entity Classification Election, the "check-the-box" form. It lets an eligible entity choose how it is classified for federal tax purposes: an LLC can use it to elect to be taxed as a C corporation, or to change its classification, or to revert to its default. Its destination is corporate (specifically C-corp) or default classification.

Form 2553 is the S-corporation election. Its destination is S-corp taxation.

Here is the part that saves a filing: when an LLC files Form 2553 to elect S-corp status, the IRS treats that 2553 as also making the deemed entity-classification election. The LLC is deemed to have elected to be classified as a corporation as of the S-election effective date, so it does not need to file a separate Form 8832. One form, the 2553, accomplishes both the "be taxed as a corporation" step and the "and specifically as an S corporation" step. You only need Form 8832 on its own when your destination is C-corporation taxation, or when you are changing or reverting an entity's classification for some reason other than an S election.

So the rule of thumb: electing S-corp status, file only Form 2553. Electing C-corp status or otherwise reclassifying, file Form 8832. The cases where you genuinely file both are rare and specific, and if you think you are in one, it is worth a short conversation with a tax adviser before you mail anything.

The Form 2553 Walkthrough, Part by Part

The form is one page with four parts, and most small businesses complete only the first.

Part I, Election Information, is the core of the form and the part everyone fills in. It captures the entity's name, address, and EIN; the date and state of incorporation; the effective date of the election (line E); and the selected tax year (line F), which for most businesses is the calendar year. It then requires a consent statement from every shareholder: each one's name, address, SSN or EIN, the number of shares and date acquired, and their signature consenting to the election. Unanimous shareholder consent is mandatory; a single missing signature invalidates the election. An officer signs at the bottom.

Part II, Selection of Fiscal Tax Year, is completed only by businesses that want a tax year other than the calendar year. It covers the natural-business-year test (the 25%-gross-receipts test), the section 444 election for a permitted fiscal year, and the back-up section 444 election. Most small S corps use a December year end and skip Part II entirely.

Part III, Qualified Subchapter S Trust (QSST) Election, applies only when a trust is going to be a shareholder. It captures the income beneficiary's consent and information and is used to qualify the trust as a permitted S-corp shareholder. The vast majority of small, owner-operated S corps have no trust shareholders and skip Part III.

Part IV, Late Corporate Classification Election Representations, is used when an entity (typically an LLC) is making a late election and needs the deemed corporate-classification election to be treated as timely too. It is the section that pairs with the Rev. Proc. 2013-30 relief discussed above.

The shape of the form, then, is a wide first part that everyone completes and three narrower parts that most filers leave blank. If you are a single-owner LLC electing S-corp status on a calendar year, your 2553 is realistically Part I plus a signature.

How Good Form Fits Around the 2553

Form 2553 is an IRS election you file directly with the IRS, by mail or fax. A form builder does not file it for you, and you should be skeptical of any service that blurs the line between "we helped you organize the information" and "we filed a federal tax election on your behalf." Where Good Form fits is upstream: gathering and confirming the facts the 2553 depends on, and the reasonable-salary plan it implies, before you sit down to complete the form.

Good Form is a form builder used by small operations and finance teams to run the intake side of business and employment paperwork. It sits at the start of the same chain the federal forms run along: the SS-4 that issues the EIN, the W-9 an S corp hands clients, the W-2 it issues itself once the owner is on payroll, and the quarterly Form 941 that reports that payroll. For the 2553 specifically, the hard part is rarely the form itself; it is collecting clean shareholder consents, confirming the EIN and effective date, and documenting the reasonable-salary rationale that makes the whole election defensible. That is the intake Good Form is built for.

The Companion Template

The Good Form 2553 intake template (clone it here) is a pre-filing capture for everything the election needs. It collects the legal entity name and EIN exactly as they should appear; the entity type and state and date of incorporation; the intended effective date and a deadline check against the 2-months-15-days rule; a per-shareholder consent block (name, address, SSN or EIN, shares, date acquired) so the unanimous-consent requirement is met before you file; the tax-year selection; a flag for whether late-election relief under Rev. Proc. 2013-30 applies; and a reasonable-salary planning section that records the comparable-wage rationale you will want on file if the salary is ever questioned.

It does not file the 2553, and it does not make you an S corporation. Only the IRS does that, in response to the form you send. What the template does is turn the election from a research project into a verification step: gather the consents, confirm eligibility against the four tests, check the effective date against the deadline, document the salary plan, and then complete and file the form. Form 2553 is short, the election it makes is consequential, and the businesses that get it right are the ones that had the EIN, the consents, and the salary rationale lined up before they started filling it in.