Form 8832 is the IRS Entity Classification Election, the single form an eligible business files to choose how it is taxed: as a corporation, as a partnership, or as a disregarded entity. It is the original "check-the-box" form, the one the 1996 regulations created so that a business could pick its federal tax classification by ticking a box rather than litigating its corporate resemblance. Form 8832 does not create a company, change what a company does, or change its legal form with the state. It changes one thing: the tax box the entity sits in. For a business already operating on an EIN from Form SS-4, the entity classification election is the lever that decides whether profit is taxed once on the owners' returns or behind a corporate wall.

This guide is the 2026 walkthrough of form 8832 for a US business: what the election actually does, the default classifications it overrides, the six choices on line 6, the effective-date window that runs from 75 days back to 12 months forward, the 60-month limitation that locks the choice once made, the late-election relief under Rev. Proc. 2009-41 that rescues a missed effective date, and how the form differs from (and pairs with) Form 2553. The audience is founders deciding how a new LLC should be taxed, owners considering a move to C-corporation treatment, and the finance lead handed the job of "go change how the IRS sees us." If you want a clean intake that captures the entity identity, current and target classification, owner consents, and effective date a clean 8832 depends on, clone the Good Form 8832 intake template.

The short version:

- Form 8832 is the Entity Classification Election, the "check-the-box" form. An eligible entity uses it to choose to be taxed as a corporation, a partnership, or a disregarded entity.

- It is a tax classification, not a legal entity. You still form an LLC or other entity with your state first; the 8832 only changes how the IRS taxes that existing entity.

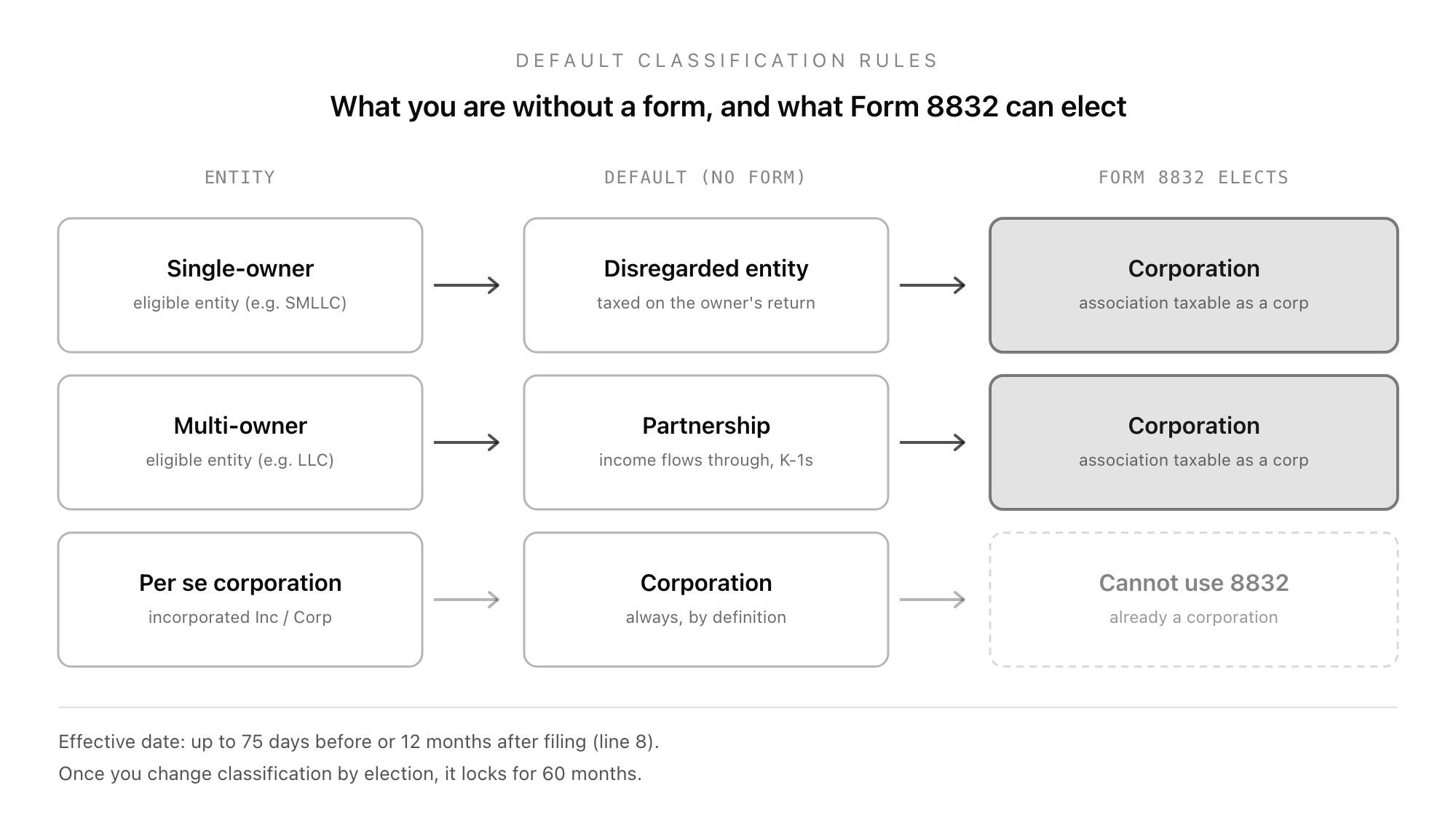

- Default classifications apply automatically if you never file. A domestic single-owner eligible entity defaults to disregarded; a domestic multi-owner entity defaults to a partnership. You file 8832 only to override a default.

- A "per se" corporation (a business incorporated as Inc or Corp under state law) cannot use Form 8832. It is already a corporation by definition. The form is for eligible entities, most often LLCs.

- Line 6 has six choices: domestic or foreign, each electing association-taxable-as-a-corporation, partnership, or disregarded. The common one is a domestic entity electing corporate treatment.

- The effective date (line 8) can be up to 75 days before the filing date and up to 12 months after it. Leave it blank and the election is effective on the filing date.

- The 60-month limitation locks the choice. Once an entity changes its classification by election, it generally cannot change again for 60 months (five years). A newly formed entity's first election is exempt from the lock.

- Miss the effective date and Rev. Proc. 2009-41 usually still saves you: file within 3 years and 75 days of the intended date, write "FILED PURSUANT TO REV. PROC. 2009-41" at the top, and attach a reasonable-cause statement.

- Form 8832 and Form 2553 are different elections. 8832 elects C-corporation (or default) classification. 2553 elects S-corporation status, and it carries a deemed classification election, so an LLC going S-corp files only the 2553, not both.

What Form 8832 Is and Why It Exists

Form 8832, formally the Entity Classification Election, is the form an eligible business files to elect how it is classified for federal tax purposes under Treasury Regulation section 301.7701-3. The shorthand "check the box" comes from the 1996 regulations that replaced an older, litigation-heavy test (the IRS used to weigh a business against a four-factor list of corporate characteristics) with a simple administrative choice. Since 1997, an eligible entity has been able to pick its classification by checking a box on this form.

The word "eligible" carries the weight. An eligible entity is a business entity that is not automatically a corporation under the rules. The most common eligible entity by far is the LLC, but the category also includes certain partnerships and foreign entities. What is not eligible is a "per se" corporation: a business that incorporated under a state's corporation statute (an Inc or a Corp) is a corporation for tax purposes by definition and has nothing to elect. Form 8832 is the form for the entities that have a genuine choice, which in practice means LLCs and similar unincorporated entities.

The reason the election exists is that the default tax treatment is not always the one a business wants. The defaults are sensible starting points, not destinations. An LLC that grows, raises money, or wants to retain earnings inside a corporate shell may need a classification its default never gave it. Form 8832 is the mechanism for that change, and the rest of this guide is about the rules that govern when and how the change takes effect.

The Default Classifications and the Check-the-Box Idea

Before you can decide whether to file form 8832, you have to know what the IRS already thinks you are. Every eligible entity has a default classification it falls into automatically, with no form filed at all.

A domestic eligible entity with a single owner defaults to a disregarded entity. The IRS ignores it as separate from its owner, so a single-member LLC owned by an individual is taxed as a sole proprietorship, and one owned by a corporation is treated as a division of that corporation. A domestic eligible entity with two or more owners defaults to a partnership, with income flowing through to the members on Schedule K-1. A per se corporation is, and stays, a corporation.

Form 8832 lets an eligible entity override its default. The six choices on line 6 are the full menu: a domestic entity can elect to be an association taxable as a corporation, a partnership, or (if it has a single owner) a disregarded entity; and the same three choices exist for foreign eligible entities. For a typical US small business, the live choice is almost always one option: a domestic LLC electing to be an association taxable as a corporation. That single election is what people usually mean when they say a company "filed an 8832 to become a C corp." Electing partnership or disregarded status on the form is rarer, because those are usually the defaults already; you reach for them mainly when you are changing an entity back after a prior election, or aligning classification after an ownership change.

Form 8832 vs Form 2553: Which One You Actually File

This is the question that sends most people to this article, because both forms are "elections" filed by LLCs that want different tax treatment, and plenty of advice online says to file both. For most businesses, that advice is wrong, and the distinction is clean once you see the destinations.

Form 8832's destination is C-corporation taxation (an association taxable as a corporation) or a change back to a default classification. Form 2553 destination is S-corporation taxation. They point at different boxes.

Here is the part that saves a filing. When an LLC files Form 2553 to elect S-corp status, the IRS treats that 2553 as also making the deemed entity-classification election. The LLC is deemed to have elected corporate classification as of the S-election effective date, so it does not file a separate Form 8832. One form, the 2553, does both jobs: be a corporation, and specifically an S corporation.

So the rule of thumb is short. Want S-corp taxation, file only Form 2553. Want C-corp taxation, file Form 8832. The only time you genuinely touch both is an uncommon sequence (electing C-corp on 8832 and later electing S-corp on 2553, for example), and if you think you are in that case it is worth a short conversation with a tax adviser before mailing anything. The self-employment-tax math behind the S election explains why most profitable small businesses want the S box rather than the C box, and therefore the 2553 rather than the 8832.

The Filing Deadline and the Effective-Date Window

Form 8832 does not have a hard annual deadline the way Form 2553 does. Instead it has an effective-date window, and the window is generous. On line 8, you state the date you want the election to take effect, and that date can be up to 75 days before the date you file and up to 12 months after it. If you leave line 8 blank, the election takes effect on the date the form is filed.

That 75-days-back, 12-months-forward window is the practical deadline. It means you can file in March and make an election effective on January 1 of the same year (within the 75-day look-back), or file now for an election that takes effect next year (within the 12-month look-forward). What you cannot do is reach back further than 75 days without falling into late-election territory and needing the relief procedure below.

The form is filed by mailing or faxing the completed 8832 to the IRS service center for the entity's location (the current addresses are in the form instructions; most filers use either Kansas City or Ogden). The IRS then sends an acknowledgment letter confirming whether the election was accepted, usually within about 60 days. A separate copy of the 8832 also has to be attached to the entity's federal tax return for the year the election takes effect. Keep the acknowledgment letter; it is the proof the classification is in place, and the document a future accountant, lender, or buyer will ask to see.

The 60-Month Limitation Rule

The single most important thing to understand before you file form 8832 is that the choice locks. Once an eligible entity elects to change its classification, it generally cannot change its classification again by election for 60 months (five years) after the effective date of the election. The clock is there precisely to stop businesses from flipping between classifications year to year to chase a short-term tax result.

There are two exceptions worth knowing. First, the 60-month lock does not apply to an entity's very first election when that election is effective on the date the entity was formed. A brand-new LLC that elects corporate treatment from day one is making an initial classification, not a change, so it is not locked out of a future change by the 60-month rule. Second, the IRS can permit an earlier change if more than 50% of the ownership interests in the entity are held by people who did not own any interest on the effective date of the prior election (a genuine ownership turnover, not a paper shuffle).

The practical takeaway is that an 8832 election is a five-year decision, not a this-year decision. Model the classification you want to live with for the medium term, not the one that minimizes tax in the next twelve months, because reversing it on a whim is exactly what the limitation forbids.

Late-Election Relief Under Rev. Proc. 2009-41

Missing the effective-date window is common, and in most cases it is fixable without the slow, expensive private-letter-ruling route. Revenue Procedure 2009-41 provides a simplified path to late entity-classification election relief. It is the 8832 counterpart to the Rev. Proc. 2013-30 relief that rescues a late S-corp election, and it works far more often than panicked founders expect.

To qualify, the entity generally has to meet a short list of conditions: it intended to be classified as it is now electing, as of the intended effective date; it has not yet filed (or had others file) returns inconsistent with that intended classification, or the relief is requested before those returns are due; it has reasonable cause for the failure to file on time; and the relief is requested within 3 years and 75 days of the requested effective date. (Different timing applies in a handful of special situations, but 3 years and 75 days is the headline window for the typical case.)

Mechanically, you file the same Form 8832, write "FILED PURSUANT TO REV. PROC. 2009-41" across the top, and attach a statement explaining the reasonable cause for the delay and confirming the consistency of any returns already filed. As with the on-time form, the practical lesson is to file inside the window, because relief is never guaranteed and a clean acknowledgment letter is worth more than a reasonable-cause argument. But if the effective date has slipped, Rev. Proc. 2009-41 is the route.

The Form 8832 Walkthrough, Line by Line

The form is short, and Part I (Election Information) is the whole of it for most filers.

Line 1, Type of election. You check whether this is an initial classification by a newly formed entity (1a) or a change in the current classification (1b). The 1a versus 1b distinction matters because the initial-classification box is the one that escapes the 60-month lock.

Lines 2a and 2b, the 60-month question. These ask whether the entity has changed its classification within the last 60 months. Answering them honestly is how you confirm you are not tripping the limitation rule discussed above.

Line 3, more than one owner. You state whether the entity has more than one owner. The answer steers the available classifications: a single-owner entity can be a corporation or disregarded; a multi-owner entity can be a corporation or a partnership.

Lines 4 and 5, owner and parent information. If the entity has a single owner, line 4 captures that owner's name and identifying number. If it is owned by a parent corporation, line 5 captures the parent's name and EIN.

Line 6, type of entity. This is the check-the-box line itself, the six options (domestic or foreign, by corporation, partnership, or disregarded). You tick exactly one.

Line 7, foreign country. Completed only by a foreign eligible entity, naming its country of organization.

Line 8, effective date. The date you want the election to take effect, inside the 75-days-back to 12-months-forward window.

Consent and signatures. A consent statement has to be signed by each member of the electing entity (or by an officer, manager, or member authorized to make the election). The bottom of the form holds the late-election relief representations used when filing under Rev. Proc. 2009-41.

The shape of the form, then, is a single page of identity and classification facts plus signatures. The hard part is never the typing; it is being sure the classification you are checking is the one you want to live with for five years, that everyone who has to consent has consented, and that the effective date is inside the window.

When Electing C-Corp Status Actually Makes Sense

Because the common live use of form 8832 is electing C-corporation treatment, it is worth being clear about when that is the right call, since for many profitable small businesses it is not. Default pass-through treatment (or an S election on the 2553) avoids the C corporation's defining drawback, which is the second layer of tax: a C corp pays the 21% federal corporate rate on its profit, and shareholders pay again on dividends.

The cases where C-corp classification still wins are specific. Founders raising venture capital usually need a C corporation (most institutional investors will not hold LLC interests, and the standard Delaware C-corp is what term sheets assume). Businesses that intend to retain and reinvest earnings rather than distribute them can prefer the flat 21% rate to pass-through rates on income the owners never take home. And the Qualified Small Business Stock exclusion under section 1202, which can exempt a large slice of gain on a future sale, is available only for stock in a C corporation. If none of those describe you, the 8832-to-C-corp election is usually the wrong lever, and the Form 2553 S-election or the default pass-through treatment is the better fit.

How Good Form Fits Around the 8832

Form 8832 is an IRS election you file directly with the IRS, by mail or fax. A form builder does not file it for you, and you should be skeptical of any service that blurs "we helped you organize the information" into "we filed a federal tax election on your behalf." Where Good Form fits is upstream: gathering and confirming the facts the 8832 depends on before you complete it.

Good Form is a form builder used by small operations and finance teams to run the intake side of business and employment paperwork. It sits at the start of the same chain the federal forms run along: the SS-4 that issues the EIN, the W-9 the entity hands to clients, and the returns that follow once a classification is set. For the 8832 specifically, the work that goes wrong is rarely the form; it is confirming the current default classification, deciding the target classification you can defensibly keep for five years, collecting every owner's consent, and pinning an effective date inside the window. That verification is the intake Good Form is built for.

The Companion Template

The Good Form 8832 intake template (clone it here) is a pre-filing capture for everything the election needs. It collects the legal entity name and EIN exactly as they appear on the EIN record; the current entity type and its default classification; whether this is an initial classification or a change (the line 1 question that drives the 60-month lock); the target classification you are electing on line 6; the number of owners and their consent blocks; the intended effective date with a check against the 75-days-back to 12-months-forward window; a 60-month-limitation check; and a late-relief flag for Rev. Proc. 2009-41 with space for the reasonable-cause statement.

It does not file the 8832, and it does not change your classification. Only the IRS does that, in response to the form you send. What the template does is turn the election from a research project into a verification step: confirm the default you are leaving, choose the box you can live with for five years, collect the consents, set the effective date inside the window, and then complete and file the form. Form 8832 is one page, the choice it records is a five-year one, and the businesses that get it right are the ones that had the EIN, the consents, and the effective date lined up before they checked the box.