The Schedule C tax form is how anyone who works for themselves tells the IRS what their business made and what it spent. Its formal name is "Profit or Loss From Business," it attaches to your personal Form 1040, and it is the single most-filed small-business tax form in the country. If you freelance, drive for a rideshare app, sell on Etsy, consult on the side, or run a one-person LLC, this is the form that turns a year of invoices and receipts into the one number the IRS taxes. This is the 2026 walkthrough: who files a Schedule C, the income and expense lines that make it up, the cost-of-goods and vehicle sections, the self-employment tax that catches people out, and the handful of lines that draw an audit.

The reason the form matters so much is that it does two jobs at once. It calculates your business profit, and that profit then gets taxed twice over: once as ordinary income tax, and again as self-employment tax. Understanding the structure is the difference between a form that feels arbitrary and one you can actually plan around. If you want to collect a client's numbers cleanly before you prepare one, clone the Good Form Schedule C intake template.

The short version:

- Schedule C reports self-employment income. Sole proprietors and single-member LLCs file one Schedule C per business, attached to the 1040.

- It has four parts. Part I income, Part II expenses, Part III cost of goods sold, Part IV vehicle. Most service businesses only touch Parts I and II.

- Line 31 is the answer. Income minus expenses equals net profit (or loss), and that number flows to Schedule 1 of your 1040.

- The profit is taxed twice. Once as income tax, and again at 15.3% self-employment tax via Schedule SE, because no employer paid the other half of your Social Security and Medicare.

- Part II is where the money is. Roughly twenty expense categories, Lines 8 to 27. Every dollar of legitimate, documented expense lowers both taxes.

- Three lines draw scrutiny. The vehicle deduction, meals (50% deductible), and the home office. All are claimable; all need real records.

- You may owe quarterly. Self-employment income usually means estimated tax payments on Form 1040-ES four times a year, not one bill in April.

Who Has to File a Schedule C?

You file a Schedule C if you carry on a trade or business as a sole proprietor or as the single owner of an LLC that has not elected corporate taxation. In plain terms, if you earn money working for yourself and you have not set the business up as an S corporation or partnership, your business income lands on Schedule C.

That covers a huge range of people: freelancers and contractors, gig-economy drivers and couriers, online sellers, tradespeople, consultants, creators earning ad or sponsorship income, and anyone with a profitable side hustle. The IRS does not care whether you think of it as a "real business." If the activity is regular, continuous, and done to make a profit, it is a business, and it goes on Schedule C. (A genuine hobby that occasionally makes money is treated differently and cannot deduct expenses the same way.)

A few rules worth knowing up front. You file one Schedule C per distinct business, so if you both drive for a delivery app and sell crafts, that is two forms. A married couple who jointly run an unincorporated business can each file a Schedule C for their share as a "qualified joint venture" rather than filing a partnership return. And income reported to you on a 1099-NEC or 1099-K belongs here, but so does cash and any income for which no 1099 ever arrived. The threshold for owing self-employment tax is just $400 of net profit.

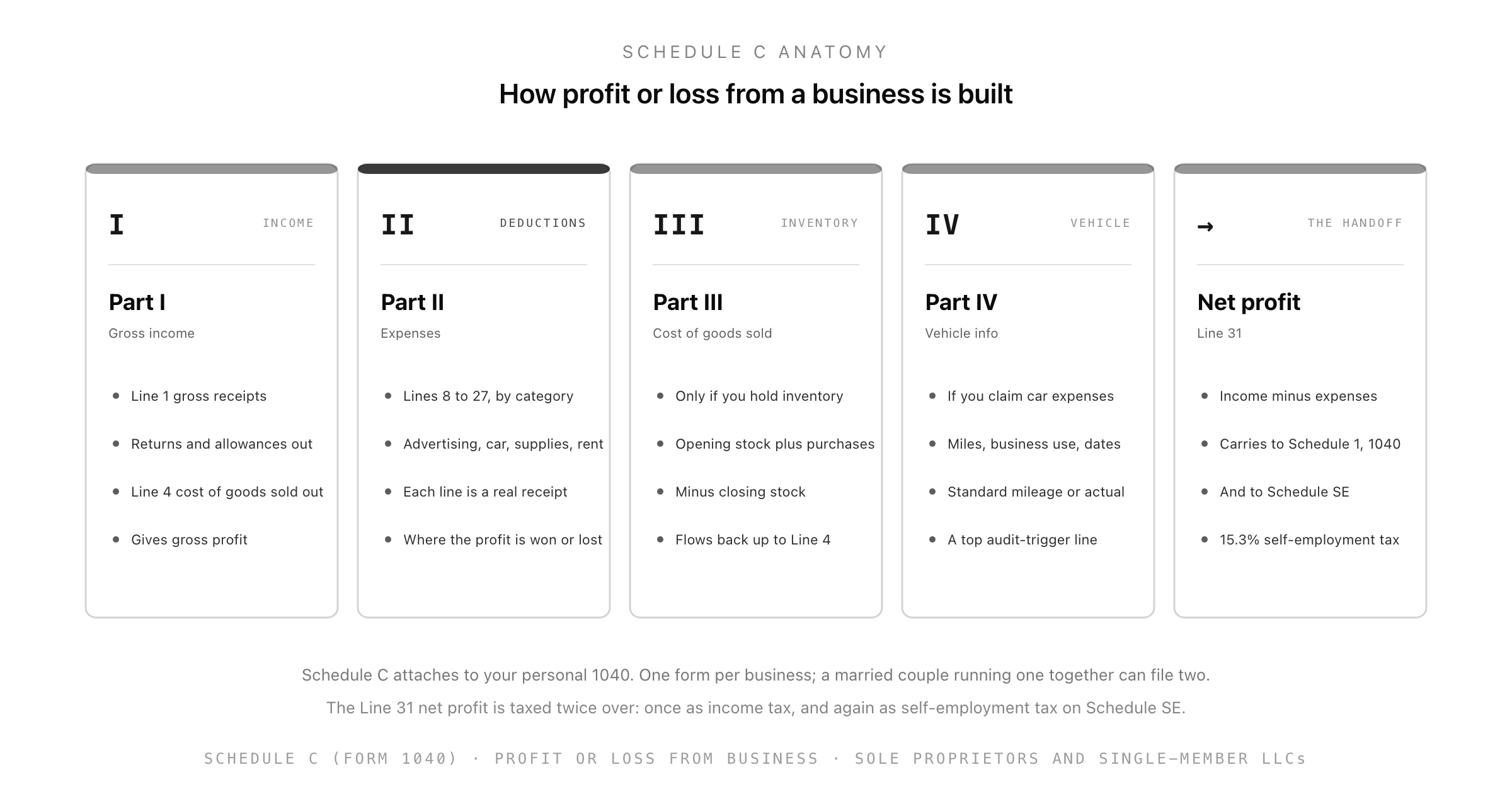

The Structure of Schedule C

The form looks dense, but it has a clean logic. It is built in four parts that flow into a single net-profit number.

Part I, Income. You start with Line 1, gross receipts, which is everything the business took in. You subtract returns and allowances, then subtract the cost of goods sold from Part III if you have inventory, and you arrive at gross profit. Add any other business income and you have gross income.

Part II, Expenses. This is the heart of the form, around twenty named expense categories from Line 8 to Line 27. Each line is a bucket for a type of ordinary, necessary business cost. The total of these is what comes off your gross income.

Part III, Cost of Goods Sold. Only relevant if you hold inventory, typically a product business rather than a service one. You take opening inventory, add purchases and direct costs, subtract closing inventory, and the result flows back up to Line 4 in Part I.

Part IV, Vehicle Information. If you claim car or truck expenses in Part II, you fill this in with your mileage and business-use details. It exists so the IRS can sanity-check vehicle deductions, which is exactly why it is a sensitive area.

The bottom line. Line 28 totals your expenses, and Line 31 subtracts them from gross income to give net profit or loss. That single figure is what the whole form exists to produce.

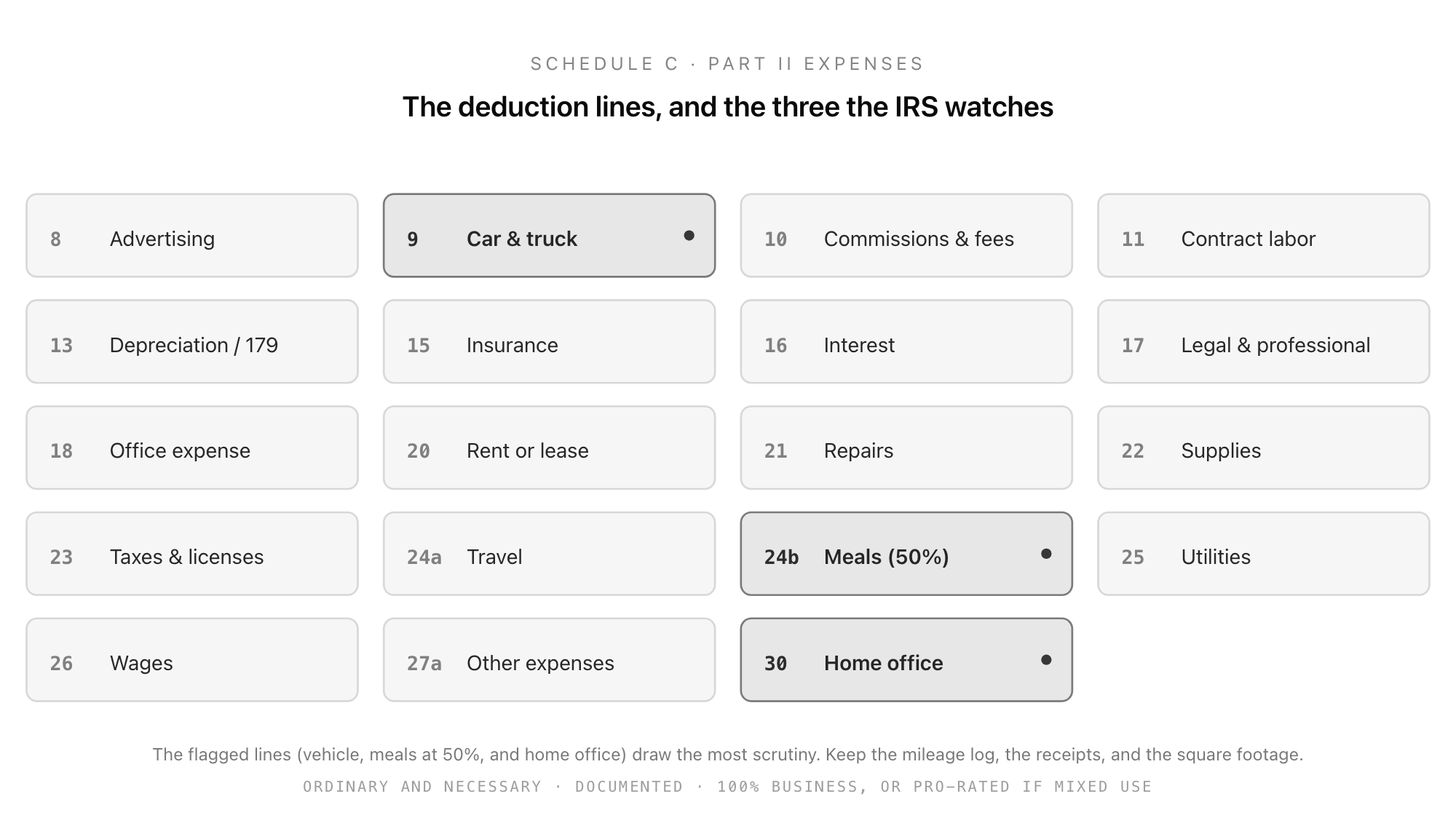

Part II: The Expense Categories

Most of your tax outcome is decided in Part II, so it is worth knowing the categories. The governing rule for every line is that an expense must be ordinary and necessary for your business: ordinary meaning common in your line of work, and necessary meaning helpful and appropriate. It must also be documented and, if an item is used partly for personal reasons, only the business portion is deductible.

The categories cover advertising, car and truck, commissions and fees, contract labor, depreciation and Section 179, insurance, interest, legal and professional services, office expense, rent or lease, repairs, supplies, taxes and licenses, travel, meals, utilities, wages, and a catch-all "other expenses" line where you list anything that does not fit a named bucket. A few deserve a note:

- Contract labor (Line 11) is what you paid to other independent contractors. If you paid any one of them $600 or more, you generally owe them a 1099-NEC, and the W-9 you collected from them is where their details come from.

- Meals (Line 24b) are generally only 50% deductible, so a $100 business lunch is a $50 deduction. Entertainment is no longer deductible at all.

- Wages (Line 26) are for W-2 employees, not for paying yourself. A sole proprietor does not take a wage; you simply keep the net profit, and you cannot deduct "your own salary."

Self-Employment Tax: The Part That Surprises People

Here is the line that catches first-time filers. When you are an employee, your employer quietly pays half of your Social Security and Medicare taxes, and the other half comes out of your paycheck. When you work for yourself, there is no employer, so you owe both halves. That combined rate is 15.3% (12.4% Social Security up to an annual wage cap, plus 2.9% Medicare with no cap) and it is called self-employment tax.

It is calculated on Schedule SE, using the net profit from your Schedule C Line 31, and it is completely separate from and on top of your ordinary income tax. This is why a freelancer earning $60,000 of profit can be startled by their bill: they owe income tax on that profit at their normal rate, and then roughly another 15% in self-employment tax before income tax is even counted. There is one piece of relief built in, you get to deduct half of the self-employment tax as an adjustment to income, but the headline rate is real and it is the single biggest reason self-employment feels more heavily taxed than a salary.

Because no one is withholding tax from your payments through the year, the IRS expects you to pay as you go through quarterly estimated payments on Form 1040-ES. Miss them and you can owe an underpayment penalty even if you settle up in April. If your year ran long and you need more time to file the return itself, remember that Form 4868 buys filing time but not paying time, so your estimated tax is still due in April.

The Three Lines the IRS Watches

Schedule C deductions are legitimate and you should claim every one you are entitled to. But three areas have a reputation for abuse, so they draw more scrutiny, and the way to claim them safely is simply to keep the records that prove them.

The home office. A genuine home-office deduction is valuable and perfectly legal, but it requires a space used regularly and exclusively for business. The kitchen table where you also eat dinner does not qualify. You can use the simplified method ($5 per square foot up to 300 square feet) or the regular method that pro-rates your actual home costs on Form 8829. Keep the square-footage math.

The vehicle. Car and truck expenses are claimed either with the standard mileage rate or with actual costs, and Part IV asks for your business and total miles. The thing that protects this deduction is a contemporaneous mileage log, a record kept as you go rather than reconstructed from memory in April.

Meals. Deductible at 50%, for genuine business purposes, with a record of who you met and why. A reasonable amount with documentation is fine; round numbers with no receipts are what invites questions.

In every case the deduction is allowed. What turns a routine deduction into an audit problem is claiming it without the documentation to back it up.

Collect the Numbers Once, File Cleanly

Whether you prepare your own Schedule C or you handle them for clients as a bookkeeper, the painful part is never the form. It is assembling a scattered year of income and expenses into the categories the form actually uses. The people who breeze through tax season are the ones who tracked income and tagged expenses by Schedule C line all year, so April is data entry rather than archaeology.

That is exactly the kind of structured collection a form is built for. With Good Form you can stand up a year-end Schedule C intake template that walks a sole proprietor or a client through their gross receipts, their cost of goods sold, the Part II expense categories, and the vehicle and home-office questions, so everything you need to complete the form arrives in one organized place. It fits neatly beside the rest of the self-employment paperwork, from the W-9 you collect from contractors to the extension you file when a return is not ready in time.

Schedule C looks intimidating because it is dense, not because it is hard. It is income minus expenses, arranged into named buckets, producing one number that gets taxed twice. Learn the structure once and it becomes the most predictable form you file. Create a free Good Form account and build the intake, so next year the business side of your taxes is already half done before you start.