Form 1040 is the tax return almost every American files. Its formal name is the "U.S. Individual Income Tax Return," and it is the single sheet (front and back) where every other tax document you receive in a year finally adds up. Your W-2, your 1099s, your Schedule C profit, your mortgage interest, your withholding: all of it lands on the 1040, which reconciles what you owe against what you already paid and produces one number, a refund or a balance due. This is the 2026 walkthrough of what Form 1040 is, the page-1 and page-2 lines, the schedules that attach to it, the difference between the 1040 and the 1040-SR, the standard deduction, and the deadline.

The form looks intimidating because it touches every part of your financial year, but its logic is a straight line: gather income, subtract a deduction, calculate the tax, subtract what you have paid, and settle up. Once you see that spine, the rest is just knowing which line each number belongs on. If you prepare returns for clients and want to gather their figures cleanly before you start, clone the Good Form 1040 tax organizer template.

The short version:

- Form 1040 is the individual income tax return. Nearly every taxpayer files one each year to report income and settle their federal tax.

- It runs in one direction. Total income, minus adjustments, equals adjusted gross income (AGI); minus your deduction, equals taxable income; tax, minus credits and payments, equals your refund or balance due.

- AGI on Line 11 is the pivot. Many credits, deductions, and phase-outs are measured against it.

- Schedules attach as needed. Numbered Schedules 1, 2, and 3 carry extra income, extra taxes, and extra credits; lettered Schedules A to F carry itemized deductions, capital gains, business profit, and more.

- Most filers take the standard deduction. For 2025 returns it is $15,000 single and $30,000 married filing jointly, raised by inflation, so itemizing on Schedule A only pays when your deductible costs beat that.

- 1040-SR is the same form, larger type. It is for taxpayers 65 and older with an identical line structure and a printed standard-deduction chart.

- The deadline is April 15, 2026 for the 2025 tax year. Need more time to file? Form 4868 buys six months, but not more time to pay.

What Is a 1040 Form?

A 1040 form is how an individual tells the federal government what they earned in a calendar year and calculates the income tax due on it. If you have a job, run a business, draw a pension, collect investment income, or earn money in almost any other way above the filing threshold, you file a 1040. It is the master return: other tax forms either feed numbers into it or attach to it as supporting schedules.

It helps to separate two kinds of forms. Information returns, like the W-2 your employer sends or the 1099-NEC a client sends, report a single slice of income to both you and the IRS. The 1040 is the return itself, the place where all those slices combine, your deduction comes off, the tax is figured, and the year is reconciled. Information returns are the ingredients; the 1040 is the meal.

The current 1040 is short by design. In 2018 the IRS redesigned it into a compact two-page form and moved the less-common entries onto three numbered schedules. A simple return (wages, standard deduction, a refund) can fit entirely on the two pages with no schedules at all. The complexity only appears when your situation calls for it.

The Structure of Form 1040

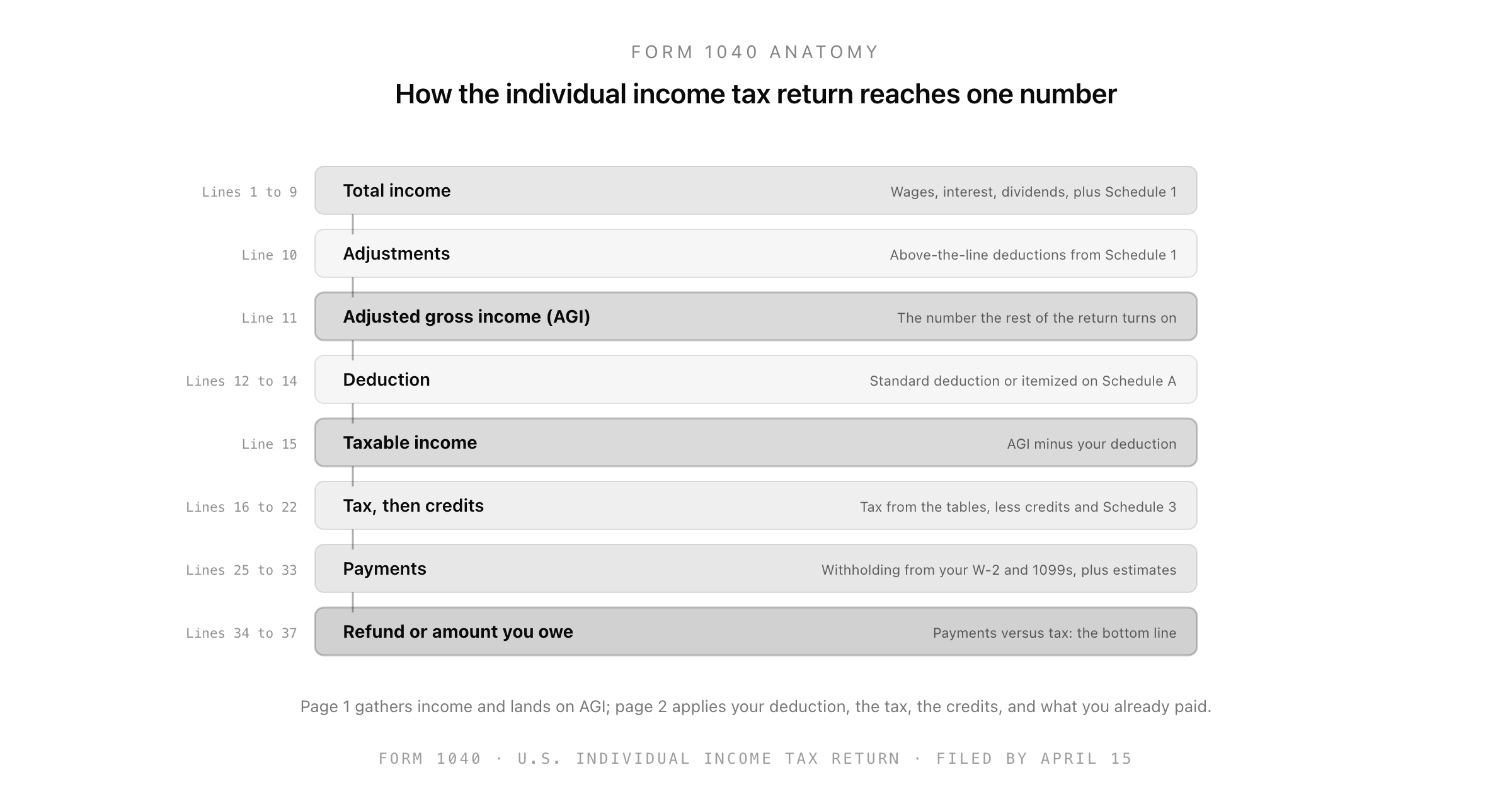

Despite everything it does, the 1040 is built on a single arithmetic spine. Read it top to bottom and each section hands a number to the next.

The top block: who and how. Before any numbers, page 1 captures your name, Social Security number, filing status (single, married filing jointly, married filing separately, head of household, or qualifying surviving spouse), and dependents. Filing status is not cosmetic: it sets your standard deduction and your tax brackets, so it is the first real decision on the form.

Income (Lines 1 to 9). You list wages from your W-2, then interest, dividends, IRA and pension distributions, Social Security, and capital gains. Anything that does not have its own line, from business profit to unemployment, arrives here as a single total carried in from Schedule 1. Add it all and you have total income.

Adjustments to AGI (Lines 10 to 11). A short list of "above-the-line" deductions (such as educator expenses, self-employment tax, HSA contributions, and student-loan interest) comes off via Schedule 1. Subtract them and Line 11 gives your adjusted gross income, the single most-referenced number on the return.

Deduction and taxable income (Lines 12 to 15). You subtract either the standard deduction or your itemized total from Schedule A. The result on Line 15 is your taxable income, the figure the tax is actually calculated on.

Tax, credits, and payments (Lines 16 to 33). You look up the tax, subtract credits (child tax credit, education credits, and the rest, some via Schedule 3), add any other taxes from Schedule 2, then record what you already paid: withholding from your W-2 and 1099s, plus any estimated payments.

The bottom line (Lines 34 to 37). If your payments beat your tax, the difference is your refund. If they fall short, it is the amount you owe. That settlement is the entire reason the form exists.

How to Fill Out a 1040: The Order That Works

If you are completing a 1040 by hand or just want to understand what software is doing, work in this order rather than strictly top to bottom:

- Set your filing status and dependents first. Everything downstream depends on it.

- Enter every income document. Pull each W-2 and 1099 and put its figures on the matching line. Do not skip a 1099 just because it was small; the IRS already has a copy.

- Handle adjustments on Schedule 1 if any apply, then lock in your AGI.

- Choose standard or itemized. Take the standard deduction unless your Schedule A total clearly beats it.

- Figure the tax and apply credits. Use the tax tables or the IRS calculation, then work through the credits you qualify for.

- Total your payments. Add up withholding (it is printed in box 2 of each W-2 and the withholding box of your 1099s) plus any estimated tax you sent in.

- Reconcile and sign. Compare tax to payments, write in the refund or balance due, and sign. An unsigned return is not a filed return.

The practical lesson for anyone gathering this information, especially a preparer collecting it from a client, is that the work is mostly assembly. If the source documents are complete and organized before you start, the form fills itself in.

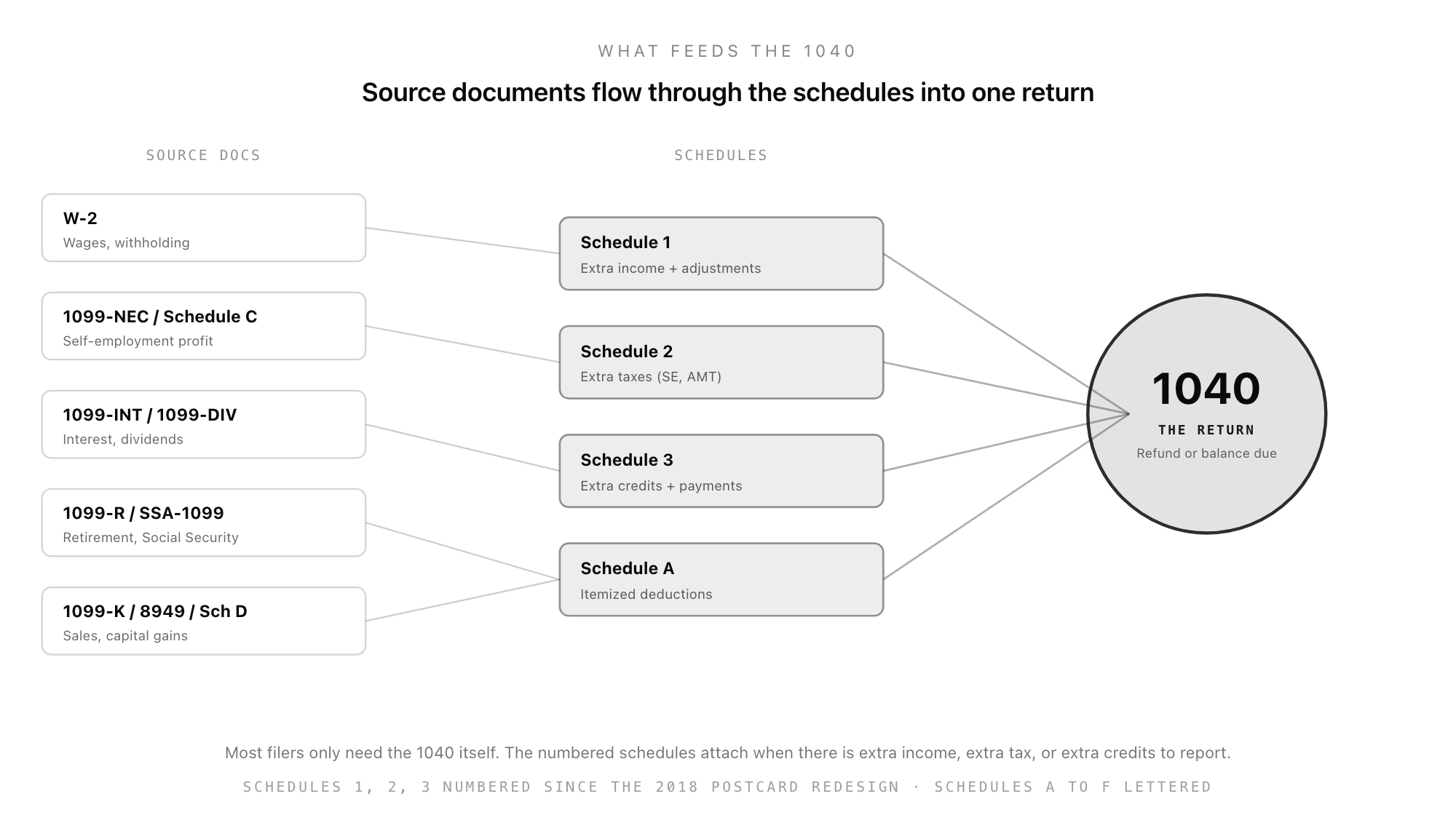

The Schedules That Attach to the 1040

The reason the 1040 stays short is that it offloads detail onto schedules. There are two families: numbered schedules (1, 2, 3) added in the 2018 redesign, and the older lettered schedules (A through F).

Schedule 1, Additional Income and Adjustments. Catches income without its own 1040 line (business profit from Schedule C, rental income, unemployment, gambling winnings) and the above-the-line adjustments. Its two totals flow to Lines 8 and 10.

Schedule 2, Additional Taxes. Carries taxes beyond ordinary income tax: self-employment tax, the alternative minimum tax, and a handful of others.

Schedule 3, Additional Credits and Payments. Carries nonrefundable credits (foreign tax credit, education credits, residential energy) and certain other payments.

The lettered schedules. Schedule A itemizes deductions (mortgage interest, state and local taxes, charitable gifts). Schedule B reports larger interest and dividend totals. Schedule C reports sole-proprietor business profit. Schedule D with Form 8949 reports capital gains. Schedule E covers rental and pass-through income, and Schedule F covers farm income.

You only attach the schedules your situation calls for. A retiree with a pension and the standard deduction may file none of them; a freelancer with investments may file several.

1040 vs 1040-SR: Which One?

The 1040-SR is the 1040 for older taxpayers. It is available to anyone born before January 2, 1961 (that is, age 65 or older for the 2025 tax year), and it is identical in substance to the standard 1040: same line numbers, same schedules, same calculations.

The differences are purely about readability. The 1040-SR uses a larger font and prints the standard deduction chart directly on the form, including the extra standard deduction that taxpayers 65 and older are entitled to. There is no tax advantage to choosing one over the other; the 1040-SR simply makes the same return easier to read and reminds older filers of the larger deduction they qualify for. If you e-file, the software picks the right version for you and the distinction barely matters.

The Standard Deduction and the 2026 Deadline

For most people the biggest single subtraction on the return is the standard deduction, a flat amount you take instead of itemizing. For the 2025 tax year (the return filed in early 2026) it is $15,000 for single filers and $30,000 for married couples filing jointly, with an additional amount for taxpayers who are 65 or older or blind. These figures rise with inflation each year, so always confirm the current number in the 1040 instructions.

Itemizing on Schedule A only makes sense when your deductible costs (chiefly mortgage interest, state and local taxes capped at the legal limit, and charitable giving) add up to more than the standard deduction. For the large majority of filers, they do not, which is why most people simply take the standard amount.

The filing deadline for the 2025 return is April 15, 2026. If you cannot file in time, Form 4868 gives you an automatic six-month extension to October 15, but it is an extension to file, not to pay: any tax you owe is still due in April, and interest and penalties run from then. If you expect to owe, estimate and pay by the deadline even if the paperwork follows later.

Get the Numbers Right Before You File

The hardest part of a 1040 is rarely the arithmetic. It is collecting every figure (each W-2, every 1099, the business totals, the withholding) accurately and in one place before you start. A missing 1099 or a transposed withholding number is what turns a quick return into an IRS notice months later.

That is the part a good intake solves. With Good Form you can build a clean tax-organizer questionnaire that gathers a client's filing status, dependents, income documents, and deductions in one structured submission, so the numbers arrive ready to enter rather than scattered across emails and photos. Clone the 1040 tax organizer template to start, or set up the supporting forms that feed the return, from W-4 withholding to Schedule C intake. Get the inputs clean, and the 1040 is just assembly.