Form W-7 is the application a person uses to get an ITIN, the Individual Taxpayer Identification Number the IRS issues to people who need to file or be reported on a US tax return but who are not eligible for a Social Security number. An ITIN is what lets a non-resident with US-source income file a return, what lets a foreign person claim a tax-treaty benefit on a W-8BEN, what lets a spouse or dependent who lacks an SSN be listed on a US tax filing, and what lets the third-party reporting on a 1099 or 1042-S land against an actual taxpayer identifier rather than an empty field. None of that happens until the W-7 is on file and the IRS has issued a number.

This is the 2026 walkthrough of form w-7 for the person applying and the firm helping them: what an ITIN is and is not (it is a tax filing number; it is not work authorisation, not a Social Security card, not an immigration document), the seven reason boxes (a through h) that say why you are applying, the line-by-line identity capture, the documentation rules that decide whether one passport or two alternate documents are needed, the four routes by which a W-7 actually reaches the IRS, and the renewal process for an ITIN that has expired from non-use. If you want a clean intake that captures the reason, identity, foreign address, and documentation plan a complete W-7 depends on, clone the Good Form W-7 ITIN intake template.

The short version:

- An ITIN is an Individual Taxpayer Identification Number. The IRS issues it to people who must be on a US tax return but cannot get a Social Security number. It is for tax purposes only.

- An ITIN looks like an SSN, but it always starts with a 9 (format 9XX-XX-XXXX). The two are visually similar and structurally distinct: SSNs come from the Social Security Administration; ITINs come from the IRS via Form W-7.

- Box a through box h on the W-7 is the reason for the application. The most common ones: (a) non-resident alien filing a US return, (b) resident alien filing a US return, (d) dependent of a US person, (e) spouse, (h) other (including treaty benefits claimed on Form 8233 or W-8BEN).

- The W-7 is normally filed with a US tax return. The return goes in the same envelope as the W-7; both arrive at the IRS together; the ITIN is assigned and the return is then processed under it.

- Documentation is the part most applications fail on. A valid, unexpired passport alone is sufficient for identity AND foreign status. Without a passport, you need two documents from the IRS's list of 13 (birth certificate, national ID, driving licence, visa, school records for dependents, and others), one for identity and one for foreign status.

- Originals or agency-certified copies are required. Standard notary-public certifications are not accepted; the certifying body must be the issuing authority itself (a passport office for a passport, a registrar for a birth certificate, etc.).

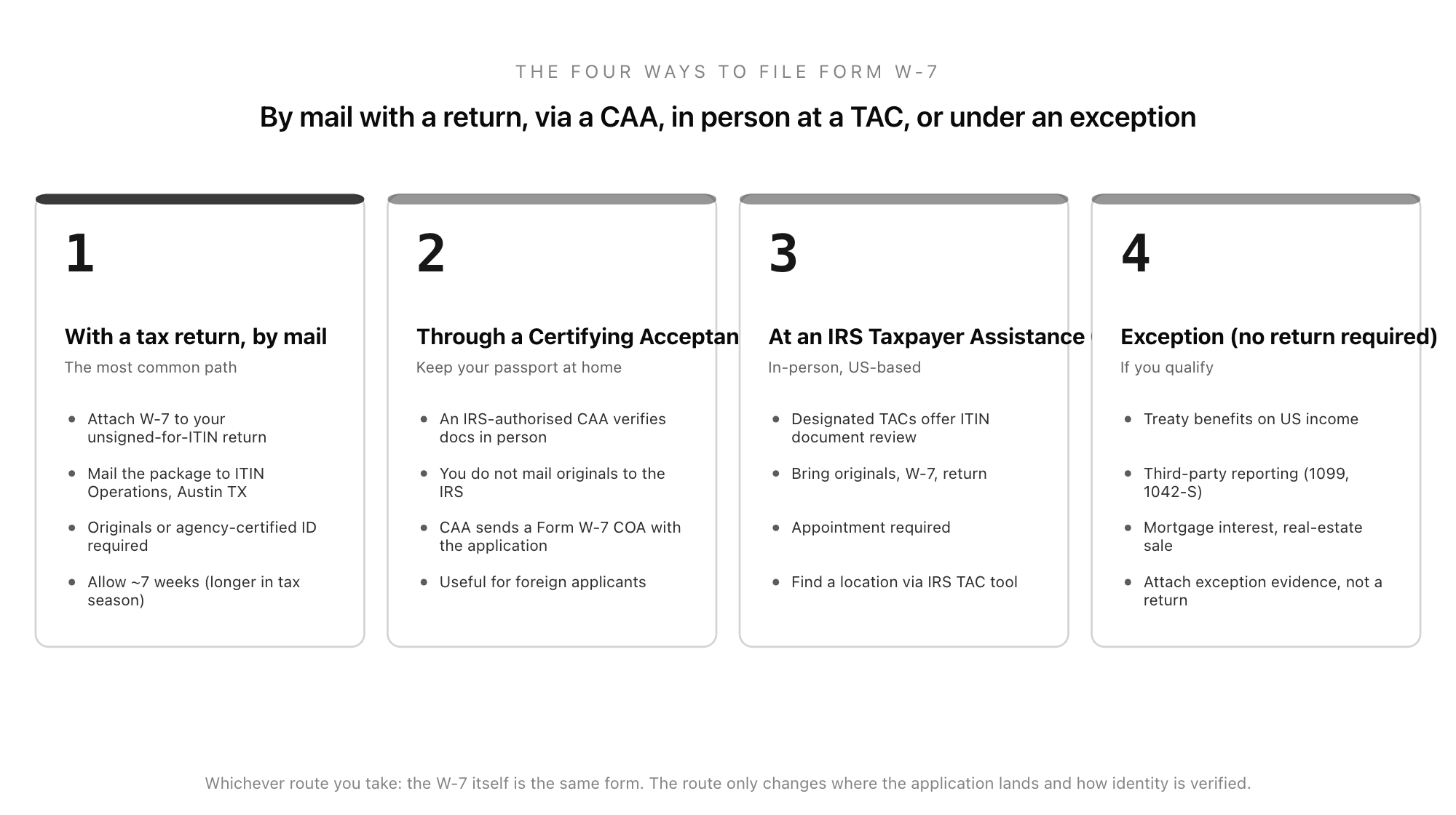

- Four routes exist for filing: by mail with a return (to ITIN Operations, Austin), through a Certifying Acceptance Agent (CAA) who verifies documents on your behalf so you keep your passport, in person at a designated IRS Taxpayer Assistance Center (TAC), or under an exception if you have a non-return reason such as treaty benefits or third-party reporting.

- ITINs expire if not used on a US tax return at any point during three consecutive years. A return for tax year 2022, 2023, or 2024 keeps an ITIN current through 2025; with no return in any of those three years, the ITIN expires on the last day of 2025.

- Renewing an expired ITIN uses the same Form W-7, marked "Renew an existing ITIN," with the same documentation rules and the same four filing routes. The number itself stays the same; only its activated status is restored.

- A US-source payer that issues 1099s, hires US workers, or files a corporate return operates under an EIN obtained via Form SS-4; the W-7/ITIN is the person-side counterpart for someone who needs a tax ID but is not eligible for an SSN.

What an ITIN Actually Is

An ITIN is a nine-digit Individual Taxpayer Identification Number issued by the Internal Revenue Service. The IRS created it in 1996 to solve a narrow but real problem: the US tax system needs every taxpayer to have a unique identifier, but a significant population of people who interact with that system are not eligible for a Social Security number. Non-resident aliens with US investment or rental income, foreign spouses and dependents claimed on a joint return, students and scholars covered by a tax treaty, and foreign sellers of US real estate all owe or are owed taxes and need an identifier to file under. The ITIN is that identifier.

The single most important thing to understand about an ITIN is what it is not. It is not a Social Security number, even though the format is identical. It does not authorise the holder to work in the United States. It does not affect immigration status, and it is not used by US Citizenship and Immigration Services. It does not entitle anyone to Social Security benefits, the Earned Income Tax Credit, or other SSN-gated programmes. It exists for one purpose: to identify a person on a US tax filing. Applying for an ITIN does nothing else and signals nothing else.

The format is the source of the most common confusion. ITINs are written 9XX-XX-XXXX. They always start with a 9. The middle two digits fall in specific ranges historically assigned to the IRS. The visual match to an SSN means many payroll, banking, and reporting systems accept an ITIN in an SSN field, and the number simply works. Just know that you are looking at a tax ID issued by the IRS, not an identity issued by the SSA.

The Reasons: Boxes a Through h

The first thing the W-7 asks is why. Boxes a through h list the eight reasons a person applies for an ITIN, and exactly one box must be ticked. The reason determines what documentation the IRS expects to see with the application and whether a tax return must be attached.

Box (a) is the non-resident alien required to obtain an ITIN to claim treaty benefits or because they have a US tax filing requirement. Box (b) is the non-resident alien who is filing a US tax return. Box (c) is the US resident alien (under the substantial-presence test or another residency rule) who is filing a US tax return. Box (d) is the dependent of a US citizen or resident alien. Box (e) is the spouse of a US citizen or resident alien. Boxes (f) and (g) cover non-resident students, professors, or researchers and their dependents. Box (h) is the catch-all "other," used most often for treaty-benefit claims via Form 8233 or W-8BEN where the treaty article and the applicable income type are written into the reason line.

The reason box is where the application's audit trail begins. The IRS examiner reading the form will use it to decide what supporting documents must accompany the W-7. A box-d dependent, for example, must include the dependent on the attached tax return; a box-h treaty-benefits claim must attach the treaty-claim document and the applicable evidence. Picking the right box is not cosmetic; it controls what the rest of the package needs to contain.

The Line-by-Line

Lines 1a and 1b are the applicant's legal name as written on the tax return, and the applicant's name at birth if it differs. Names must match the supporting identity documents. Marriage name changes, transliterations, and ordering of multiple given names are common reasons applications come back, so it is worth writing the name exactly as it appears on the strongest piece of supporting evidence (typically a passport) and using the same form on the return.

Lines 2 and 3 are the mailing address and the foreign residence address. These are not the same field; the IRS expects them to differ. Line 2 is where the IRS will send the assignment notice; line 3 is where the applicant actually lives in their home country. A line 3 that simply repeats line 2 is a flag.

Lines 4 and 5 are birth and identity: date of birth (in MM-DD-YYYY format), country of birth, country of citizenship, and the foreign tax identifying number (FTIN) issued by the country of residence. Many treaty claims and many bank-account-driven W-7 filings now require the FTIN on the form.

Line 6 captures US visa data when applicable: visa type, visa number, date of entry into the United States, and the USCIS number if the applicant has one. A US driving licence used as a supporting identity document also goes here.

The signature line at the bottom is signed by the applicant under penalty of perjury, by a parent or court-appointed guardian for a minor, or by a delegate of authority where one is in place. The phone number on the form is where the IRS will call if it has a question, which it often will.

The Documentation Rules

Documentation is the single most failure-prone part of a W-7. The rule is simple in principle and unforgiving in practice: the IRS must see evidence of identity and evidence of foreign status, and the evidence must be either originals or copies certified by the issuing agency.

The cleanest version of the documentation is a single passport. A current, unexpired passport (with at least one page of biometric or photo identity data) is the only single document that proves both identity and foreign status. If the application uses a passport, no other documentation is required for those two requirements.

When no passport is available, the IRS will accept two documents from a list of thirteen acceptable alternates. At least one document must prove identity (commonly: national identification card, driver's licence, US state driver's licence) and at least one must prove foreign status (commonly: foreign voter's registration card, foreign military identification card, civil birth certificate, foreign driver's licence). A US state driver's licence counts only for identity; a foreign birth certificate counts for both. For dependents on a parent's return, school records or medical records may be added to the package to support the relationship.

The certification rule is where many applications die. A standard notary public is not the certifying body the IRS will accept. Certification must come from the issuing agency itself: a passport office for a passport, a national-ID-issuing authority for the national card, a civil registrar for a birth certificate. The reason is fraud: notarisation is widespread and inconsistent; agency certification ties the copy directly to the original record. If you cannot reach the issuing agency, the practical alternative is the Certifying Acceptance Agent route, where a trained intermediary verifies your originals in person.

The Four Routes

A W-7 reaches the IRS by one of four paths, and the right path depends on whether you have a US return to attach, whether you are inside the United States, and whether you can part with your passport for several weeks.

Route one is by mail, with a US tax return attached. This is the most common path. The applicant completes the W-7, attaches the return that requires the ITIN (with the ITIN field left blank, or with "Applied For" written in), encloses the original passport (or alternate documents), and mails the entire package to ITIN Operations in Austin, Texas. The IRS issues the ITIN, processes the return under the new number, and returns the original documents by mail. Typical timeline: about seven weeks outside the tax-filing crush, longer in February through May.

Route two is through a Certifying Acceptance Agent (CAA). A CAA is an individual or firm the IRS has authorised to verify identity documents on the applicant's behalf. The applicant visits the CAA with originals; the CAA examines them, signs Form W-7 (COA), and submits the application without sending the originals to the IRS. The applicant keeps the passport throughout. This route is especially useful for applicants outside the United States, and for anyone unwilling to mail an original passport to a tax authority.

Route three is in person at a Taxpayer Assistance Center. Specifically designated IRS TACs offer ITIN document review by appointment. The applicant brings the W-7, the return, and originals; the TAC clerk reviews and returns the documents on the spot, then forwards the package to ITIN Operations. The location list and appointment system are on irs.gov.

Route four is the exception route, used when no return is attached. Most W-7s are filed with a return; a minority are not. The exception cases include treaty-benefit claims via a withholding-agent letter, third-party reporting where a 1099 or 1042-S will issue, the mortgage-interest reporting case, and the real-estate-sale reporting case. In each, the applicant attaches the exception evidence to the W-7 in place of a return and explains why the return is not required.

Renewing an Expiring ITIN

ITINs are not permanent. The IRS expires an ITIN that has not been used on a US tax return at any point during three consecutive years. The expiration is automatic. An ITIN used on a return for tax year 2022, 2023, or 2024 is current through the end of 2025; one not used in any of those three years expires on the last day of 2025.

Renewal uses the same Form W-7, with the "Renew an existing ITIN" box ticked at the top. The same documentation rules apply: passport or two alternates, originals or agency-certified copies, mailed or via a CAA or in person at a TAC. The applicant's existing ITIN does not change; the renewal restores its active status. A return filed against an expired ITIN is processed but most refund and credit claims are blocked until the renewal lands.

The most common ITIN-renewal trigger is a family with US-side filings using a foreign spouse or dependent on the return: every three years, the ITIN must be exercised or renewed, and the calendar moves quietly. A short calendar reminder against the year a return is filed is the practical fix.

Why a Payer Cares (Even If You Are Not the Applicant)

Most readers of this guide are not applying for their own ITIN. They are the US-side payer or HR or finance lead figuring out what to do about a foreign contractor or spouse on someone else's return. For that audience the W-7 connects to two adjacent forms.

The first is the W-8BEN. A foreign individual claiming a tax-treaty rate on US-source income often needs a US TIN to support the claim, and that TIN is an ITIN obtained on Form W-7. The W-8BEN does not produce the ITIN; the W-7 does. The two travel together: collect the W-8BEN for the foreign-status documentation and, where a treaty rate is being claimed and an ITIN is required, walk the payee toward the W-7 application path.

The second is information reporting. If you will issue a 1099 or 1042-S for payments made to a person, that report needs a TIN. Where the payee is foreign and not eligible for an SSN, the W-7 is what produces a number to file the report against. Without one, the report is filed with a missing TIN, and backup-withholding and matching-notice problems follow.

The cleanest payer-side workflow keeps the two paths separate. US payees flow through the W-9 and 1099 process; foreign payees flow through the W-8BEN and, where an ITIN is needed, the W-7. A short, structured intake makes the routing obvious and captures the documentation plan before money moves. The Good Form W-7 ITIN intake template covers the reason box, identity data, address pair, foreign tax ID, and documentation route in one pass so the application package is complete before it leaves your desk.

The Short Version

Form W-7 is the IRS application for an Individual Taxpayer Identification Number, the tax-only identifier used by people who must be on a US tax return but are not eligible for a Social Security number. An ITIN is 9XX-XX-XXXX, looks like an SSN, and is for tax filing alone: not work authorisation, not an immigration document, not a route to Social Security benefits. The W-7 asks for one of eight reasons (boxes a through h) plus identity (name, address pair, birth, foreign tax ID, US visa data where applicable), supported by either a single passport or two of thirteen alternate documents, with originals or agency-certified copies, never standard notarisations. The form normally travels with a US tax return to ITIN Operations in Austin, but it can also be filed through a Certifying Acceptance Agent (which lets the applicant keep their passport), in person at a designated IRS Taxpayer Assistance Center, or under an exception when no return is required. ITINs expire after three years of non-use on a return; renewal uses the same form, marked "Renew." For a US-side payer, the W-7 is the partner form to the W-8BEN and the upstream condition for filing 1099 or 1042-S reports against foreign individual payees. If you want the intake built for you, clone the W-7 ITIN intake template in Good Form and stop chasing the documentation plan after the fact.