The W-8BEN form is the IRS Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting, the single form a non-US individual gives to a US payer to say "I am a foreign person, here is my country, and here is the treaty rate I am entitled to." It is the foreign-person counterpart to the W-9: where a US contractor hands you a W-9, an overseas contractor hands you a W-8BEN. Getting it on file is what lets a US business pay an international freelancer, license-holder, or investor correctly, without over-withholding 30% by default and without issuing a 1099 to someone who never owed US tax in the first place.

This is the 2026 walkthrough of the w-8ben form for the US payer who has to collect it and the foreign payee who has to complete it: what the certificate of foreign status actually does, the line-by-line of all three parts, how a tax-treaty claim reduces or removes withholding, the crucial rule that services performed abroad are foreign-source income (so there is usually nothing to withhold and no 1099 at all), how the form differs from the W-9 and from the entity version W-8BEN-E, and how long it stays valid. If you want a clean way to collect foreign status, treaty country, and tax IDs from an overseas contractor before the first payment, clone the Good Form W-8BEN intake template.

The short version:

- Form W-8BEN is the Certificate of Foreign Status for an individual. A non-US person gives it to a US payer to establish that they are foreign and, optionally, to claim a tax-treaty rate.

- It is the foreign-person counterpart to the W-9. US payees file a W-9; foreign individuals file a W-8BEN; foreign entities file W-8BEN-E.

- The payee completes the entire form. The US requester (the payer or withholding agent) keeps it on file and does not send it to the IRS.

- The default withholding rate on US-source FDAP income (interest, dividends, royalties, and similar) is 30%. A valid treaty claim in Part II can reduce that, sometimes to zero.

- The single most useful rule for hiring overseas: pay for services that a foreign person performs entirely outside the US is foreign-source income. It is generally not subject to US withholding and is not reported on a 1099. The W-8BEN documents the foreign status that supports that treatment.

- Part I is identity: name of the beneficial owner, country of citizenship, permanent residence address (no US address, no PO box), mailing address if different, US TIN if held, foreign TIN, and date of birth.

- Part II is the treaty claim: line 9 names the treaty country of residence; line 10 covers special rates and conditions for specific income types.

- Part III is the certification, signed under penalty of perjury. No signature means an invalid form, which means default 30% withholding.

- A W-8BEN is generally valid from the date it is signed through the last day of the third following calendar year, unless a change in circumstances makes the information wrong.

- A foreign individual who needs a US taxpayer ID for a treaty claim applies for an ITIN on Form W-7; a US-source payer that issues 1099s operates under an EIN from Form SS-4.

What the W-8BEN Form Is and Why It Exists

Form W-8BEN, the Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals), is the form a non-US individual uses to certify two things to a US payer: that they are a foreign person, and that they are the beneficial owner of the income being paid. It exists because the United States taxes US-source income paid to foreigners differently from income paid to US persons, and the payer (the "withholding agent") needs documentation to apply the right treatment.

Without a W-8BEN, a US payer faces a default it does not want. Under the US rules for payments to foreign persons, US-source income of certain kinds is subject to a flat 30% withholding tax, and a payer with no valid documentation must presume the worst and withhold. A completed W-8BEN does the opposite: it establishes the payee's foreign status, optionally claims a treaty rate that lowers or removes the 30%, and in the common case of services performed abroad, supports treating the pay as foreign-source income that is outside US withholding entirely.

The "BEN" stands for beneficial owner: the person who actually owns the income for tax purposes, not an intermediary, agent, or nominee holding it for someone else. That distinction is why the form asks the questions it does, and why an entity (a company rather than a human) cannot use this version at all and must use W-8BEN-E instead.

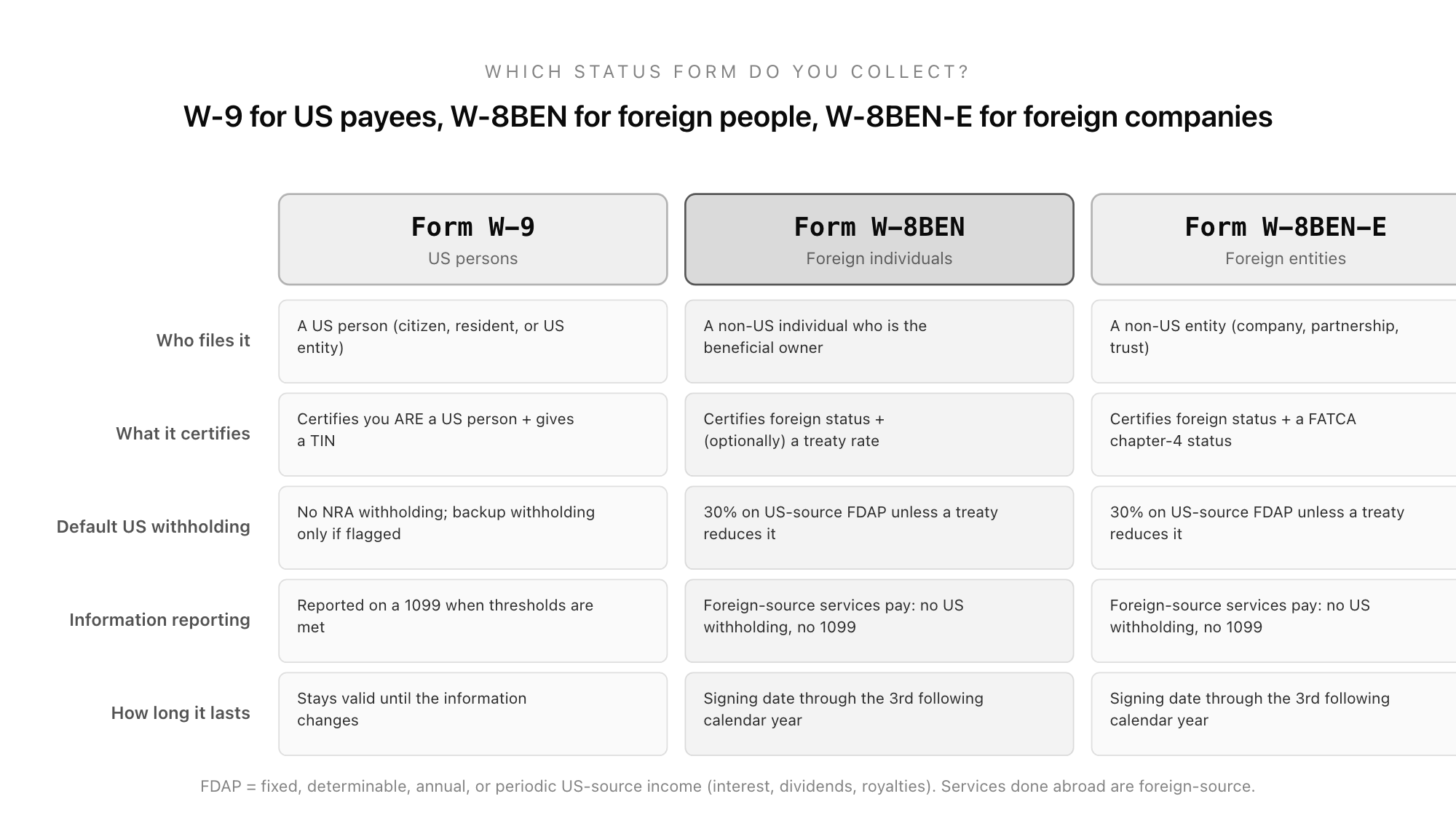

W-8BEN vs W-9 vs W-8BEN-E: Which One You Collect

The fastest way to understand the W-8BEN is to place it next to its siblings. The form you collect depends entirely on who the payee is.

A US person (a citizen, a US resident, or a US-formed entity) gives you a W-9. It certifies that they are a US person, supplies their TIN, and puts them on the path to a 1099 when the payment thresholds are met.

A foreign individual gives you a W-8BEN. It certifies that they are not a US person and lets them claim a treaty rate. A human being who is not a US person uses this form.

A foreign entity (a non-US company, partnership, or trust) gives you W-8BEN-E, a longer relative of the W-8BEN that adds a FATCA "chapter 4" status classification. If the overseas party you are paying is a registered company rather than a person, you need the W-8BEN-E, not the W-8BEN. The principle is the same; the entity form simply asks more questions.

Collecting the wrong form is the most common error in this area. A US payer who accepts a W-9 from someone who is plainly foreign, or a W-8BEN from a limited company, has documentation that does not match the payee and cannot rely on it.

The Line-by-Line: Part I (Identification)

Part I of the W-8BEN identifies the beneficial owner. It is the part everyone completes; the treaty part is optional, but Part I is not.

Line 1, name of the beneficial owner. The individual's full legal name, matching their passport or national ID. This is a person, never a business; a business name here is the signal that the wrong form is being used.

Line 2, country of citizenship. A single country. Note that this asks for citizenship, not residence. If the two differ, the residence address goes on line 3 and the treaty claim (line 9) keys off the country of tax residence, but line 2 is citizenship.

Line 3, permanent residence address. The country where the person claims to be resident for tax purposes. This cannot be a US address, a PO box, or a care-of (in-care-of) address; any of those undermines the foreign-status claim. A mismatch here is one of the things a withholding agent is told to watch for.

Line 4, mailing address. Only if it differs from line 3.

Line 5, US taxpayer identification number (SSN or ITIN). Completed only if the person actually has one. Most foreign payees do not, and that is fine. A foreign individual who needs a US TIN to support a treaty claim applies for an ITIN on Form W-7.

Line 6, foreign tax identifying number (FTIN). The tax ID issued by the person's country of residence. For many account relationships this is now effectively required, with line 6b as the checkbox for "FTIN not legally required" when the person's country does not issue one.

Line 7, reference numbers. Any account or reference number the withholding agent wants tied to the form. Often blank.

Line 8, date of birth. In MM-DD-YYYY format. Required for many financial-account uses of the form.

Part II: Claiming a Tax Treaty Rate

Part II is where the W-8BEN earns its keep for the payee, and it is optional: a person with no treaty to claim leaves it blank and is simply documented as foreign.

The United States has income-tax treaties with dozens of countries, and those treaties frequently reduce or eliminate the 30% default rate on specific kinds of US-source income, royalties and certain other categories being the common ones. Line 9 is where the payee names the country of which they are a resident and with which the US has a treaty. By signing, they certify they are a resident of that country within the meaning of the treaty.

Line 10 handles special rates and conditions: the specific article of the treaty, the rate claimed, and the type of income, used when the income needs a more particular claim than the standard categories on the form cover (certain royalties, scholarship or fellowship income, and similar). Most straightforward treaty claims do not need line 10; it is there for the cases that do.

Two things matter here. First, a treaty claim usually requires a US TIN or, for certain income, the foreign TIN, which is why lines 5 and 6 and the W-7 ITIN route connect to this part. Second, the treaty rate only applies to the income the treaty actually covers. The treaty does not turn taxable US-source income into nothing; it applies the agreed lower rate.

The Rule That Matters Most: Services Performed Abroad

For the typical US business reading this, the reason to care about the W-8BEN is hiring an overseas contractor, and the most important rule is one the form itself does not spell out: the source of services income is where the work is performed.

When a foreign person performs services entirely outside the United States, the income is foreign-source. Foreign-source income paid to a foreign person is generally not subject to US withholding, and it is not reported on a 1099. So a US company paying a developer in Lisbon or a designer in Manila who do all their work from their own country usually has nothing to withhold and nothing to file with the IRS for that payment.

So why collect a W-8BEN at all in that case? Because the form is the documentation that supports the treatment. It establishes that the payee is a foreign person, which is the fact that makes the foreign-source analysis apply. If the IRS ever asks why you did not withhold and did not issue a 1099, the answer is "the payee certified foreign status on a W-8BEN and performed the services abroad." Without the form, you are presuming foreign status with no evidence, and the default presumption runs against you.

The flip side is the trap. If a foreign contractor performs services while physically in the United States, that portion of the pay can become US-source and potentially subject to withholding even with a W-8BEN on file. The form documents status; it does not change where the work happened.

Part III: Certification and Signature

Part III is short and decisive. The beneficial owner signs under penalty of perjury, certifying that they are the beneficial owner, that they are not a US person, that the income is not effectively connected with a US trade or business (or is but is covered by a treaty), and that the treaty claims they made are correct.

The signature line is where most invalid forms die. An unsigned W-8BEN, or one signed by someone other than the beneficial owner without proper authority, is not a valid certificate, and a withholding agent cannot rely on it. No valid form means the default 30% applies. Print name and date go alongside the signature.

How Long a W-8BEN Lasts

A W-8BEN is not a one-time, forever document. As a general rule, it is valid from the date it is signed through the last day of the third succeeding calendar year. A form signed at any point in 2026, for example, generally remains valid through 31 December 2029, after which the payer needs a fresh one.

There are exceptions that shorten it: a change in circumstances that makes any information on the form incorrect (the person becomes a US resident, moves to a different country of residence, or changes anything material) invalidates the form immediately, and the payee is required to provide a new one within 30 days. There are also limited situations in which a form remains valid longer, but the three-calendar-year rule is the one to plan around. The practical takeaway for a payer: diarise W-8BEN expiries and re-collect before year-end of the third year, the same way you would refresh any compliance document.

What This Means for a US Payer Hiring Abroad

Put the pieces together and the workflow for paying a foreign contractor is clean:

- Before the first payment, collect a W-8BEN (or W-8BEN-E if the payee is a company). Do this before you pay, not after; chasing documentation from someone you have already paid is the hard way.

- Check Part I matches the person. A foreign address on line 3, citizenship on line 2, and an individual's name on line 1. Watch for the US-address and PO-box red flags.

- Decide the source of the income. Services performed abroad are foreign-source: generally no withholding, no 1099. US-source income (or work done while in the US) needs the withholding analysis, and a Part II treaty claim may reduce the rate.

- Store the form and diarise its expiry. Keep it with your payee records; do not file it with the IRS. Refresh it before the end of the third following calendar year.

- Keep US and foreign payees on separate tracks. US contractors flow through the W-9 and 1099 process; foreign contractors flow through the W-8BEN and (usually) no 1099. Mixing the two is where mistakes happen.

A short, structured intake gets you the foreign status, country of residence, treaty country, and tax IDs in one pass, before money moves. The Good Form W-8BEN intake template captures exactly those fields so the certificate on file is complete and current, and so you can tell at a glance which of your contractors are documented and which are not.

The Short Version

The W-8BEN is the Certificate of Foreign Status for a non-US individual: the form a foreign person gives a US payer to establish foreign status and, optionally, to claim a tax-treaty rate. It is the foreign-person mirror of the W-9; foreign companies use W-8BEN-E instead. Part I identifies the beneficial owner (name, citizenship, foreign address, tax IDs, date of birth), Part II claims a treaty country and rate, and Part III is the under-penalty-of-perjury signature without which the form is invalid. The default US withholding rate on US-source FDAP income is 30%, which a treaty claim can reduce or remove. The rule that matters most for hiring abroad is that services a foreign person performs entirely outside the US are foreign-source income: generally no withholding and no 1099, with the W-8BEN as the documentation that supports it. The form lasts from signing through the third following calendar year unless circumstances change. Collect it before the first payment, check that it matches the payee, store it (do not file it), and refresh it before it expires. If you want the intake built for you, clone the W-8BEN intake template in Good Form and start documenting your foreign contractors today.